Nomad Foods Limited (NYSE:NOMD) came out with its second-quarter results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Revenues were €753m, approximately in line with whatthe analysts expected, although statutory earnings per share (EPS) crushed expectations, coming in at €0.43, an impressive 22% ahead of estimates. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

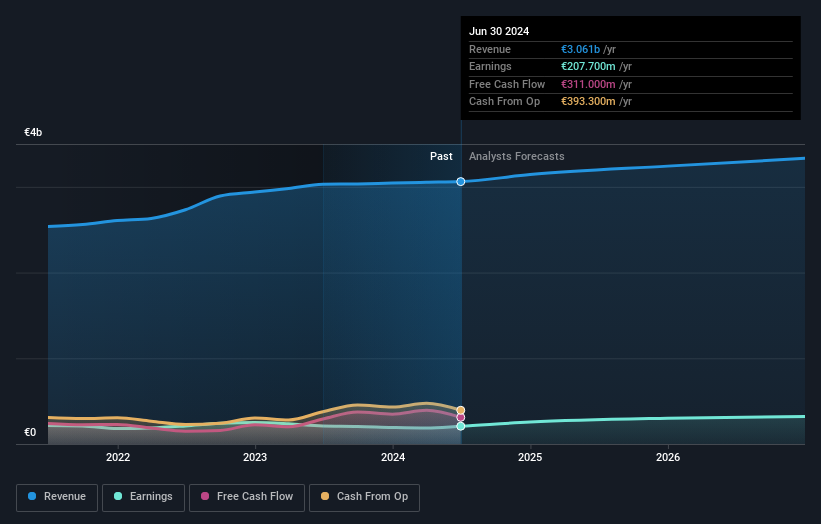

After the latest results, the seven analysts covering Nomad Foods are now predicting revenues of €3.14b in 2024. If met, this would reflect an okay 2.7% improvement in revenue compared to the last 12 months. Per-share earnings are expected to climb 15% to €1.47. Before this earnings report, the analysts had been forecasting revenues of €3.14b and earnings per share (EPS) of €1.63 in 2024. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

The consensus price target held steady at US$24.54, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Nomad Foods at US$27.95 per share, while the most bearish prices it at US$20.97. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2024 brings more of the same, according to the analysts, with revenue forecast to display 5.4% growth on an annualised basis. That is in line with its 6.5% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 3.1% per year. So it's pretty clear that Nomad Foods is forecast to grow substantially faster than its industry.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2024 brings more of the same, according to the analysts, with revenue forecast to display 5.4% growth on an annualised basis. That is in line with its 6.5% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 3.1% per year. So it's pretty clear that Nomad Foods is forecast to grow substantially faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at US$24.54, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Nomad Foods. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Nomad Foods going out to 2026, and you can see them free on our platform here..

Even so, be aware that Nomad Foods is showing 2 warning signs in our investment analysis , and 1 of those makes us a bit uncomfortable...

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.