Blink Charging Co. (NASDAQ:BLNK) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 64% loss during that time.

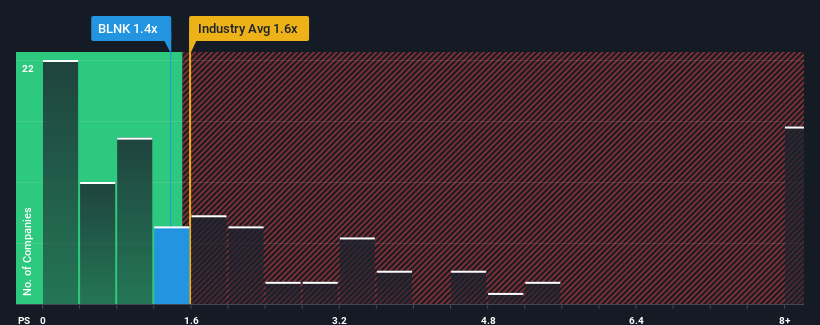

Although its price has dipped substantially, it's still not a stretch to say that Blink Charging's price-to-sales (or "P/S") ratio of 1.4x right now seems quite "middle-of-the-road" compared to the Electrical industry in the United States, where the median P/S ratio is around 1.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

How Has Blink Charging Performed Recently?

There hasn't been much to differentiate Blink Charging's and the industry's revenue growth lately. It seems that many are expecting the mediocre revenue performance to persist, which has held the P/S ratio back. If this is the case, then at least existing shareholders won't be losing sleep over the current share price.

Want the full picture on analyst estimates for the company? Then our free report on Blink Charging will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Blink Charging?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Blink Charging's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 66% gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 27% per annum during the coming three years according to the eight analysts following the company. With the industry predicted to deliver 46% growth per annum, the company is positioned for a weaker revenue result.

With this in mind, we find it intriguing that Blink Charging's P/S is closely matching its industry peers. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What Does Blink Charging's P/S Mean For Investors?

With its share price dropping off a cliff, the P/S for Blink Charging looks to be in line with the rest of the Electrical industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Given that Blink Charging's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Blink Charging (1 is potentially serious!) that you should be aware of before investing here.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.