Summary

This week (8.1-8.7), crude oil showed a trend of first suppressing and then rising. The average price of WTI this week was $74.24/barrel, a decrease of $2.54/barrel or -3.31% from the previous week. During the week, the main factors that put pressure on oil prices were: weak US economic data, global stock market decline, and increased market risk aversion. The factors that support oil prices include: EIA data shows a decrease in US crude oil inventories.

Chapter 1 Review of the Trends in the International Crude Oil Market

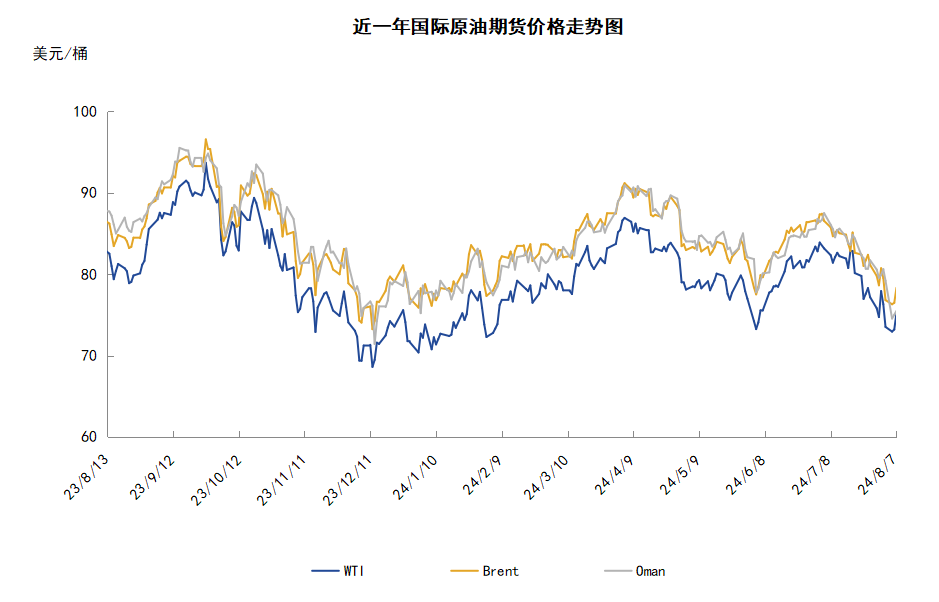

Review of This Week's Crude Oil Futures Market

This week (8.1-8.7), crude oil showed a trend of first suppressing and then rising, with a week-over-week decline in average price.

During the week, bearish pressure on oil prices intensified due to weak economic data. Recent US non-farm employment data shows that the unemployment rate and PMI data were lower than expected. Investors' concerns about the weak prospects for the US economy further escalated. The Institute for Supply Management (ISM) data shows that the US July purchasing managers' index (PMI) for manufacturing fell 1.7 percentage points to 46.8%, the lowest since November 2023. The US Labor Department data shows that the number of non-farm employment positions increased by 0.114 million in July, lower than the market's expected 0.175 million. The unemployment rate in July increased by 0.2 percentage points to 4.3%, a new high in nearly three years. In addition, global stock markets generally fell due to poor economic data, and market risk aversion increased. As a result, downward pressure on crude oil futures as a risk asset intensified.

On the other hand, the reduction in US crude oil inventories in the later part of the week supported oil prices. According to the US Energy Information Administration, as of August 2, 2024, the total US crude oil inventory, including strategic reserves, decreased by 2.992 million barrels from a week ago to 0.805154 billion barrels. US commercial crude oil inventories decreased by 3.728 million barrels from a week ago to 0.429321 billion barrels.

Review of This Week's Crude Oil Spot Market

This week, the average price of international crude oil spot prices fell compared to the previous week. In the Middle East crude oil market, Saudi Arabia raised its official crude oil selling price for September to the Asian market for the first time in three months but lowered its official crude oil selling price for September to other regions. Saudi Aramco raised its official selling price of crude oil for September by $0.10-$0.20/barrel to the Asian market, among which the official selling price of Arab Light crude oil rose by $0.20/barrel to a premium of $2.00/barrel over Oman/Dubai, reaching a two-month high, but the increase was not as expected by the market. At the same time, Saudi Aramco lowered the official selling prices of all its crude oil for September to the US market by $0.75/barrel, among which the official selling price of Arab Light crude oil fell to a premium of $4.10/barrel over ASCI. In addition, Saudi Aramco lowered the official selling prices of all its crude oil for September to Northwest Europe and the Mediterranean by $2.75/barrel, among which the official selling prices of Arab Light crude oil were ICE Brent crude oil futures prices plus $1.25/barrel and ICE Brent crude oil futures prices plus $ 1.15/barrel. In addition, after Saudi Arabia raised the official selling price of September crude oil to the Asian market at the beginning of this week, the Abu Dhabi National Oil Company (ADNOC) also raised its official selling price of September crude oil. ADNOC raised the official selling price of Murban crude oil for September to $83.80/barrel, and set the official selling price of Upper Zakum crude oil for September at $0.05/barrel higher than the Murban crude oil official price. The official selling prices of Qatari and Iraqi crude oil will be announced soon, and it is expected that the loading schedules for Middle East crude oil from September to October will be announced at the beginning of next week. In the Asia-Pacific crude oil market, Vietnam PV OIL released a tender to sell two ships each of 0.3 million barrels of Chim Sao crude oil, which will be loaded from September 29 to October 3 and October 22 to 26, respectively. The tender will end on August 12.

Chapter 2 Analysis of Factors Affecting Crude Oil Futures Market

Supply and Demand Factors

In terms of supply, due to the rebound of Russia's domestic refining operating rate to a six-month high, the country's marine transportation of crude oil has now dropped to the lowest level since January and is likely to continue at least until the end of August. Some organizations predict that Russia's maritime crude oil flow in July and August will remain around 2.7 million barrels per day, but will increase slightly to 2.9 million barrels per day in September, when Russian refineries are expected to start their traditional autumn maintenance. As a result of Ukraine's drone attacks repeatedly disrupting domestic refineries, the export volume in April and May decreased from 3.6 million barrels per day to 3.7 million barrels per day, which is quite considerable.

In terms of demand, the path of global oil demand recovery is still unclear, and the imbalance of economic recovery may continue to affect demand prospects. The market needs to closely monitor global economic indicators and energy consumption trends to better predict changes in demand. As economic growth weakens and fuel demand declines, China's oil imports and refinery operating rates are trending lower than in 2023. Some organizations believe that although China's economic data is still disappointing, a greater decline in global oil inventories is beginning to be seen, indicating that supply growth is lagging behind demand growth.

Changes in US Inventory This Week

The US refinery utilization rate has slightly increased, with commercial crude oil inventories decreasing for the sixth consecutive week, but gasoline and distillate inventories have increased. According to data from the US Energy Information Administration until the week of August 2, 2024, crude oil inventories were 3.66% lower than the same period last year, 6% lower than the same period in the past five years. Gasoline inventories were 4.01% higher than the same period last year and 2% lower than the same period in the past five years; and the distillate inventories were 10.70% higher than the same period last year and 6% lower than the same period in the past five years. In addition, last week's average daily crude oil imports to the US fell to 6.224 million barrels, a decrease of 0.729 million barrels from the previous week, and the average daily imports of refined oil products were 210.4 barrels, a decrease of 0.127 million barrels from the previous week.

Fund holding situation

Speculators holding net long positions in NYMEX Light Sweet Crude Oil futures decreased by 11.1%. According to the latest statistics from the US Commodity Futures Trading Commission, as of the week of July 30, all positions in WTI crude oil futures had fallen for two consecutive weeks, and the decline was significantly expanded. Among them, the total open position fell by 1.2% compared with the previous week, the long position fell by 11.2% compared with the previous week, the short position fell by 11.9% compared with the previous week, and the net long position fell by 11.1% compared with the previous week. Since the decline in short positions exceeded the decline in long positions, the long-short ratio of WTI continued to rebound to 4.50, an increase of 0.03 or 0.77% compared with the previous week.

This week, as concerns about the outlook for oil demand continued to intensify, funds began to withdraw from the crude oil futures market. Although the poor performance of economic data in China and the US has increased investors' concerns about the future of oil demand, the tense situation in the Middle East has supported the oil market to a certain extent, making the shrinking of the long and short positions slightly greater than the shrinking of the long positions. From the performance of oil prices, WTI crude oil futures prices began to weaken, falling below $75 per barrel. Looking ahead, as the peak season for oil consumption in Europe and the United States begins to enter the final stage, market expectations for the oil market's fundamentals will further weaken, which will increase the bearish sentiment of oil prices. However, expectaions of the rate cut by the Federal Reserve and geopolitical risks still exist in the US, and may to a certain extent support the oil market.

Chapter Three Outlook for Crude Oil Futures Market Trend

Market Outlook for Next Week

Technically, the price of WTI crude oil futures rose and then fell during the week. The main factors driving up oil prices this week are: the continued tension in the Middle East; the force majeure encountered by Sharara oil field production; the crude oil inventory decline exceeded expectations. The main factors suppressing oil prices this week are: the rebound of the US dollar exchange rate; the global stock market suffered selloffs; concerns that the US economy may be approaching a recession; and the Fed has maintained its rates for the eighth time in a row. As of the 7th, WTI closed at $75.23 per barrel, a decrease of $2.68 per barrel or -3.44% compared to the previous period. As of the week of the 7th, the weekly average price of WTI was $74.24 per barrel, a decrease of $2.54 per barrel or -3.31% compared to the previous week. From a technical perspective, the trend of oil prices is bearish.

In terms of the economy this week in the US, the new business index of service providers improved to the highest level in a year. The report shows that while the economy continues to grow, the ability of companies to pass on rising costs is limited. The comprehensive index of input prices, including rising transportation costs and wage growth, climbed. Even so, the rate of increase in output prices slowed to a six-month low. From the output point of view, growth has become worrisome, and while the service industry continues to strengthen, the manufacturing industry has fallen into a recession again. The PMI preliminary data means that in the ideal situation at the beginning of the third quarter, the economy is growing steadily and inflation is easing.

This week, on the 1st, OPEC+ implied that oil supply will remain unchanged and maintained the provisional plan to resume production that had been suspended earlier from the next quarter. The Organization of the Petroleum Exporting Countries and its allies have agreed to gradually restore production that was suspended at the end of 2022 to boost oil prices. Daily production in the fourth quarter will increase by about 0.54 million barrels.

Saudi Aramco has increased the official selling price of Arab light crude oil to Asian customers by 20 cents per barrel in September, with a specific benchmark price of Oman-Dubai +2 US dollars. However, this is lower than the predicted 50 cent increase by traders and refiners. In Europe, the price of Arab light crude oil was reduced by 2.75 US dollars, the largest decrease since the peak of the new crown epidemic.

On the 1st, the OPEC Joint Ministerial Monitoring Committee (JMMC) meeting maintained its oil production policy unchanged, and it will gradually resume production that had been suspended earlier to boost oil prices from the end of 2022. Daily production in the fourth quarter will increase by about 0.54 million barrels. In addition, the chairman of the meeting insisted on requiring member countries to make commitments to the compensation plan.

On the 6th, the US Energy Department's Office of Petroleum Reserves announced a tender, supplying 1.5 million barrels of oil to the Bayou Choctaw Reserve in January 2025, and an additional tender will be held on August 12, 2024. An additional 2 million barrels of oil will be transported to the Bryan Mound Reserve for delivery in January 2025.

Gold Investment Outlook predicts that next week (August 8-14), pressure from global economic prospects and oil demand expectations will continue to suppress the oil market. Although tensions in the Middle East are still high, its effect on the oil market is limited as it has not affected oil-producing countries yet. What we need to pay attention to next is whether the relationship between Iran and Israel will deteriorate. Once Iran enters the game, it may boost the oil market, otherwise it will be difficult to stop the weak trend of the oil market. Overall, the international oil price next week is likely to fluctuate mainly.

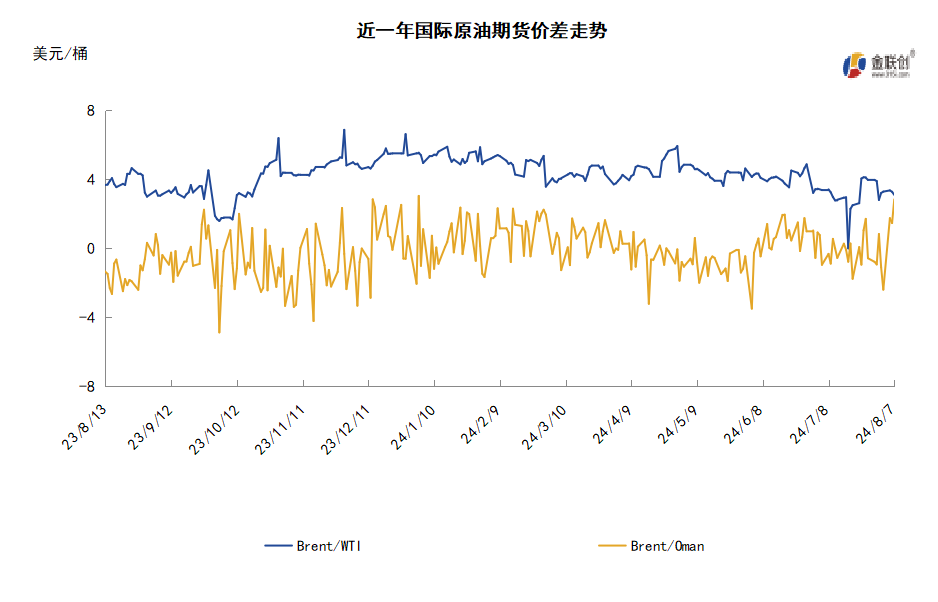

Chapter 4: Examples of crude oil futures market price differentials.

For market institutions or investors, they can focus on crude oil futures to participate in the crude oil market. Assuming that a certain futures institution wants to adopt a cross-term arbitrage scheme for market trading, the institution can formulate a trading strategy based on the current market situation. Due to the large fluctuations in current crude oil prices, risk can be effectively controlled through spread arbitrage. If the month difference structure shows that the WTI crude oil futures spread between near and far periods further expands, and the forward market sentiment declines, investors can hedge their positions by buying near-term contracts and selling far-term contracts in a hedging trade. If the current spread continues to expand, this cross-term arbitrage trade can still maintain a positive return.

Disclaimer

The data, opinions and forecasts in this report reflect the personal judgement of the author on the day of the initial release of the report. They are based on information that the author believes to be reliable and publicly available, but the accuracy and completeness of this information are not guaranteed. The author also does not guarantee that his/her views or statements in the report will not change. In different periods, the author may issue a report inconsistent with the data, opinions and predictions of this report without notifying anyone. The information or opinions expressed in the report do not constitute investment advice for anyone, and the cases listed in this report are for demonstration purposes only. The author is not responsible for any losses incurred by anyone using the content of this report.

This report reflects the personal views of the author and does not represent the research and judgment of JLC or ZCE. JLC or ZCE do not guarantee the accuracy and completeness of the report. The report is only transmitted to specific clients and the copyright belongs to JLC. Without the written permission of JLC, any institution or individual may not copy, reproduce, quote or reprint the report in any form.

The market involves risks, and investment needs to be cautious.