芯原股份表示,2024年上半年半导体产业逐步复苏,

芯原股份表示,2024年上半年半导体产业逐步复苏,① VeriSilicon shares spent 0.569 billion yuan on R&D in the first half of the year, an increase of 30.25% over the previous year. ② VeriSilicon achieved gross profit of 0.414 billion yuan in the first half of the year, a year-on-year decrease of 26.62%. Revenue from intellectual property licensing fees related to AI computing power was 0.122 billion yuan, accounting for 47.22%.

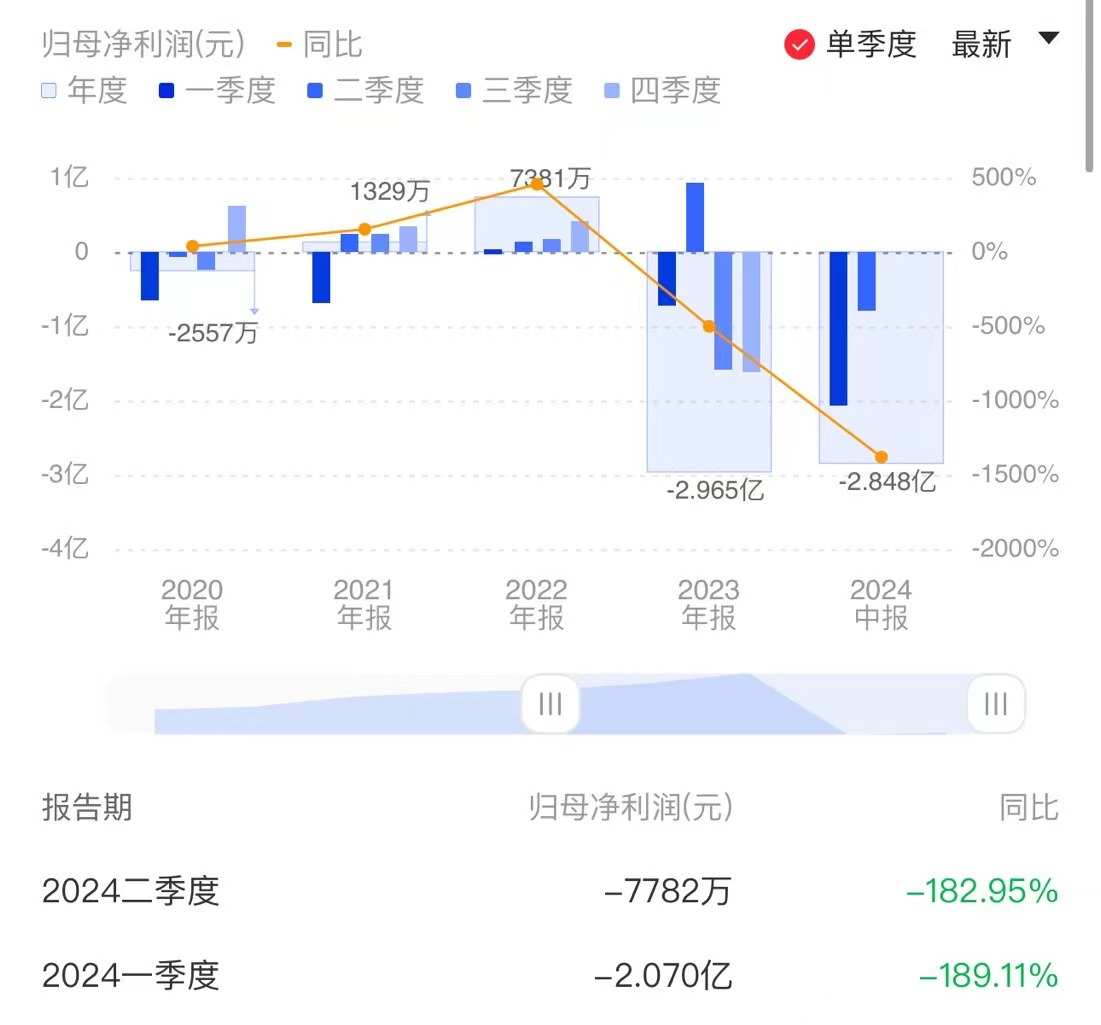

“Science and Technology Innovation Board Daily”, August 8 (Reporter Qiu Siyu) Today (August 8), VeriSilicon disclosed its 2024 semi-annual report, achieving revenue of 0.932 billion yuan, a year-on-year decrease of 21.27%; net profit to mother was -0.285 billion yuan, after deducting non-net profit of -0.304 billion yuan.

In terms of single-quarter performance, VeriSilicon achieved revenue of 0.614 billion yuan in the second quarter, an increase of 92.96% over the first quarter. However, the company remained at a loss. Net profit due to mother was 0.078 billion yuan in the second quarter, and the loss was 62.40% narrower than in the first quarter.

VeriSilicon Co., Ltd. said that the semiconductor industry gradually recovered in the first half of 2024, and the downstream customer inventory situation has improved markedly. Thanks to the company's unique business model, that is, in principle, there is no risk of product inventory, no application boundaries, and counterindustrial cycle attributes, the company's business situation quickly reversed, and the business gradually improved. The second quarter performance improved significantly compared to the first quarter.

VeriSilicon Co., Ltd. said that the semiconductor industry gradually recovered in the first half of 2024, and the downstream customer inventory situation has improved markedly. Thanks to the company's unique business model, that is, in principle, there is no risk of product inventory, no application boundaries, and counterindustrial cycle attributes, the company's business situation quickly reversed, and the business gradually improved. The second quarter performance improved significantly compared to the first quarter.

Regarding the loss in performance in the first half of the year, VeriSilicon explained that it was mainly due to factors such as fluctuations in the company's revenue and the year-on-year increase in R&D labor costs.

Financial reports show that VeriSilicon's R&D expenses were high. R&D expenses in the first half of the year were 0.569 billion yuan, an increase of 30.25% over the previous year. R&D investment accounted for 61.03% of revenue, an increase of 23.71 percentage points over the same period last year. By the end of the reporting period, the company had 1,640 R&D personnel, accounting for 89.18% of the total number of employees.

In terms of orders, VeriSilicon revealed that the new orders were in good condition. Ongoing orders have remained high for three consecutive quarters. As of the end of the reporting period, the company's current orders were 2.271 billion yuan, and the conversion rate is expected to be about 81% within one year. Among them, the company also revealed that the total number of new orders for the mass production business in the past three quarters was 0.756 billion yuan, a sharp increase of more than 400% over the first three quarters of 2023, which had an obvious impact on the inventory removal cycle.

AI-related business performance is outstanding, and gross profit is under pressure

VeriSilicon Inc. is a semiconductor IP licensing company. It has six types of processor IP: GPU IP, NPU IP, VPU IP, DSP IP, ISP IP, Display Processor IP, and more than 1,400 digital-analog hybrid IPs and RF IPs for integrated circuit design.

By business, VeriSilicon's semiconductor IP licensing business (including revenue from intellectual property licensing fees and royalties) decreased 22.36% year-on-year in the first half of the year, while revenue from the one-stop chip customization business (including revenue from chip design business and mass production business) fell 20.56% year-on-year.

However, the revenue situation of multiple business lines improved markedly in the second quarter. Among them, in the second quarter, the company's mass production business achieved revenue of 0.234 billion yuan, an increase of 125.00%; the chip design business achieved revenue of 0.193 billion yuan, an increase of 122.04%; the intellectual property license royalties business achieved revenue of 0.16 billion yuan, an increase of 60.60% over the previous month; and royalty revenue was 0.024 billion yuan, a decrease of 11.79% over the previous month.

It is worth noting that VeriSilicon's AI-related business performance is quite outstanding. In response to the massive computing power requirements of AIGC applications, the company launched AI GPU IP, high-performance GPU IP, and GPGPU IP for high-performance computing.

Financial reports show that during the reporting period, VeriSilicon's revenue from intellectual property licensing fees related to AI computing power was 0.122 billion yuan, accounting for 47.22%. Neural network processor (NPU) IP has been used by 72 customers in their 128 artificial intelligence chips, and artificial intelligence (AI) chips incorporating VeriSilicon's NPU IP have been shipped worldwide for more than 0.1 billion.

Dai Weimin, chairman of VeriSilicon, also said at the first quarter results briefing held earlier that large computing power is the foundation that supports the rapid development and evolution of AI applications. As the computing power requirements of AIGC and smart mobility (autonomous driving, smart cockpit, etc.) continue to increase, the data processing capacity and computing power requirements of chips are getting higher and higher.

However, it should be noted that VeriSilicon achieved gross profit of 0.414 billion yuan in the first half of the year, a year-on-year decrease of 26.62%; the comprehensive gross profit margin was 44.41%, down 3.24 percentage points from the same period last year. In response, the company explained that it was mainly due to factors such as changes in revenue structure and declining gross margin of the one-stop chip customization business.

VeriSilicon's shares are relatively scattered, and there are no controlling shareholders or actual controllers. As of the end of the reporting period, VeriSilicon Limited, the company's largest shareholder, had a shareholding ratio of 15.14%. The company also admits that there are certain internal control risks, and it is not ruled out that there is a risk that the company's decision-making efficiency will be poor due to no controlling shareholders or actual controllers.