Superior Group of Companies, Inc. (NASDAQ:SGC) shareholders that were waiting for something to happen have been dealt a blow with a 36% share price drop in the last month. Still, a bad month hasn't completely ruined the past year with the stock gaining 45%, which is great even in a bull market.

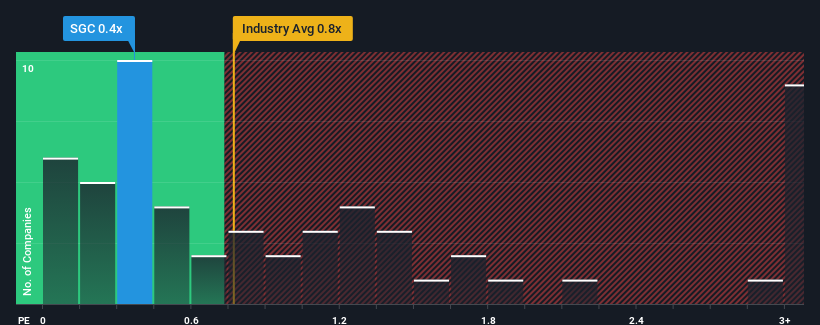

Although its price has dipped substantially, there still wouldn't be many who think Superior Group of Companies' price-to-sales (or "P/S") ratio of 0.4x is worth a mention when the median P/S in the United States' Luxury industry is similar at about 0.8x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

How Has Superior Group of Companies Performed Recently?

Recent times haven't been great for Superior Group of Companies as its revenue has been rising slower than most other companies. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Superior Group of Companies.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Superior Group of Companies' is when the company's growth is tracking the industry closely.

The only time you'd be comfortable seeing a P/S like Superior Group of Companies' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. That's essentially a continuation of what we've seen over the last three years, as its revenue growth has been virtually non-existent for that entire period. Accordingly, shareholders probably wouldn't have been satisfied with the complete absence of medium-term growth.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 4.5% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 6.2% per annum, which is not materially different.

In light of this, it's understandable that Superior Group of Companies' P/S sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

What We Can Learn From Superior Group of Companies' P/S?

Following Superior Group of Companies' share price tumble, its P/S is just clinging on to the industry median P/S. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've seen that Superior Group of Companies maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

Before you settle on your opinion, we've discovered 2 warning signs for Superior Group of Companies that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.