Source: Tencent Technology

1. Huang Renxun emphasized that generative AI is growing at an exponential rate and that businesses need to adapt and utilize this technology quickly, rather than standing by and falling behind the pace of technological development.

2. Huang Renxun believes that open and closed source AI models will coexist and that companies need to leverage their respective strengths to promote the development and application of AI technology.

3. Huang Renxun proposed that the development of AI needs to consider energy efficiency and sustainability, reducing energy consumption by optimizing the use of computing resources and promoting the inference and generation capabilities of AI models to achieve more eco-friendly intelligent solutions.

4. With the constant accumulation of data and the continuous advancement of intelligent technology, customer service will become a key area for companies to achieve intelligent transformation.

5. According to foreign media reports, at the 2024 Databricks Data + AI Summit held recently,

6. Founder and CEO Huang Renxun had a fascinating conversation with Ali Ghodsi, co-founder and CEO of Databricks. The dialogue between the two parties demonstrated the importance and development trends of artificial intelligence and data processing technology in modern enterprises, emphasizing the key role of technological innovation, data processing capabilities and energy efficiency in promoting enterprise transformation and industry development.

7. Huang Renxun looked to the future of data processing and generative AI in the conversation. He pointed out that the business data of each company is like an untapped gold mine, with tremendous value but extracting deep insight and intelligence from it has always been a daunting task.

8. Huang Renxun also talked about open source models like Llama and DBRX are driving corporate transformation into AI companies, activating a global AI movement and promoting technological development and corporate innovation. Through the collaboration between NVIDIA and Databricks, the two companies will work together to leverage their respective strengths in accelerating computing and generative AI, bringing unprecedented benefits to users.

9. The following is the transcript of the conversation:

10. Moderator: I am very excited to introduce our next guest, a man who needs no introduction, the one and only global rock star CEO - NVIDIA CEO Huang Renxun. Please come to the stage. Thank you very much for coming! I want to start with NVIDIA's remarkable performance, with a market capitalization of up to 3 trillion US dollars. Did you ever think five years ago that the world would evolve so rapidly and present such a remarkable picture today?

11. Huang Renxun: Absolutely! I expected that from the beginning.

12. Moderator: That's really amazing. Can you offer some advice to the CEOs in the audience on how to achieve their goals?

13. Huang Renxun: Whatever you decide to do, my advice is not to get involved in the development of graphics processors (GPUs).

14. Moderator: I will tell the team that we are not going to get involved in that field. We spent a lot of time today discussing the profound significance of data intelligence. Enterprises have vast amounts of proprietary data that are critical for building customized artificial intelligence models. The deep mining and application of this data are crucial to us. Have you also noticed this industry trend? Do you think we should increase our investment in this area? Have you collected any feedback and insights from the industry on this issue?

15. Huang Renxun: Every company is like a gold mine with abundant business data. If your company offers a series of services or products and customers are satisfied with them while giving valuable feedback, you have accumulated a large amount of data. These data may involve customer information, market trends, or supply chain management. Over the years, we have been collecting these data and have a huge amount of data, but until now, we have just started to extract valuable insights from them, and even higher-level intelligence.

16. Currently, we are passionate about this. We use these data in chip design, defect databases, creation of new products and services, and supply chain management. This is our first time using engineering processes based on data processing and detailed analysis, building learning models, then deploying these models, and connecting them to the Flywheel platform for data collection.

17. Our company is moving towards the world's largest companies in this way. This is, of course, due to the extensive use of artificial intelligence technology in our company, which has helped us achieve many remarkable achievements. I believe that every company is experiencing such changes, so I think we are in an extraordinary era. The starting point of this era is data, and the accumulation and effective use of data.

18. The harmonious coexistence of open source and closed source

19. Moderator: This is truly amazing and very much appreciated. At present, the debate about closed-source and open-source models is gradually heating up. Can open-source models catch up? Can they coexist? Will they eventually be dominated by a single closed-source giant? What is your view of the entire open-source ecosystem? What role does it play in the development of large language models? And how will it develop in the future?

Author: Guo Xiaojing. In 2023, the stock prices of these companies rose by 239%, 194%, 102%, 81%, 59%, 57% and 48%, respectively, and they were named the "Magnificent Seven" in the market. Meanwhile, during the same period, the Standard & Poor's 500 index only rose by a total of 24%. However, on July 24, 2024, it seems that this impressive rise came to a halt as the US market fell more than 2% and the Nasdaq fell more than 3.6%, both with the single largest daily drop since the end of 2022. It happened to coincide with the releases of the quarterly reports from Google's parent company Alphabet and Tesla. In the following days, Microsoft, Meta and Apple also released their financial reports, causing the stock market to fluctuate dramatically. Although there may be various reasons for the fluctuations, such as expectations of interest rate cuts, the release of employment data, the so-called impossible triangle, US bond yields, and US technology stocks, which have been maintaining the so-called three highs that seem to violate financial common sense. However, one of the main themes that affects market sentiment is the huge investment in AI by top US technology companies. It is a huge controversy whether it is a "future investment" or a "bill" for shareholders to pay. The biggest driving force behind this wave of growth is the huge expectation for generative AI. Irene Tunkel, chief strategy officer of US stocks at BCA Research, a global economic analysis company, commented that in addition to Nvidia, the main reason for the excellent performance of the "Magnificent Seven" in 2023 is the expansion of P/E multiples, which shows that investors have high expectations for the future profit growth of these companies. The most special one, Nvidia, which does indeed have explosive performance support, has a market capitalization that has fallen more than 22% since June, evaporating 5.2 trillion RMB, and has fallen 20% for 17 consecutive trading days. In addition to negative information about Blackwell chip production, the capital market also began to worry that if technology giants cannot prove that AI can bring sufficient incremental business, they will not be able to sustain their investments in the AI field. Nvidia's performance will not continue to exceed expectations. Expectations are always the biggest driving force behind stock price increases, far more important than past performance. The capital market seems to have split into two equally powerful camps. On the left, there is a strong vision of AI changing the world and a constant inflow of capital investment; on the right, there is a deep suspicion of the input-output ratio of AI and the huge bubble it is generating: (1) Will the huge investment by giants in generative AI make short-term financial reports look bad? (2) Can such massive investment really bring growth? When will it be realized? (3) If generative AI is a distant future, is the bubble being blown bigger and bigger? (4) Why are the giants so convinced and betting heavily on generative AI? After a deep analysis of the AI bills of technology giants, we realize that the future may be more complicated than we imagined.

$NVIDIA (NVDA.US)$,$Meta Platforms (META.US)$,$Tesla (TSLA.US)$,$Amazon (AMZN.US)$,$Alphabet-A (GOOGL.US)$,$Microsoft (MSFT.US)$And.$Apple (AAPL.US)$The weather is good today The weather is good today.

Please use your Futubull account to access the feature.$S&P 500 Index (.SPX.US)$The US market fell more than 2%.$Nasdaq Composite Index (.IXIC.US)$Nasdaq fell more than 3.6%, both with the single largest daily drop since the end of 2022. This happened to coincide with the releases of the quarterly reports from Google's parent company Alphabet and Tesla.

In the following days, Microsoft, Meta and Apple also released their financial reports, causing the stock market to fluctuate dramatically. Although there may be various reasons for the fluctuations, such as expectations of interest rate cuts, the release of employment data, the so-called impossible triangle, US bond yields, and US technology stocks, which have been maintaining the so-called three highs that seem to violate financial common sense.$USD (USDindex.FX)$But it is undeniable that one of the main themes that affects market sentiment is the huge investment in AI by top US technology companies.

There is also a huge controversy whether it is a "future investment" or a "bill" for shareholders to pay.

The biggest driving force behind this wave of growth is the huge expectation for generative AI. Irene Tunkel, chief strategy officer of US stocks at BCA Research, a global economic analysis company, commented that in addition to Nvidia, the main reason for the excellent performance of the "Magnificent Seven" in 2023 is the expansion of P/E multiples, which shows that investors have high expectations for the future profit growth of these companies.

As the results of the financial reporting season are revealed, these overly high growth expectations begin to swing significantly.

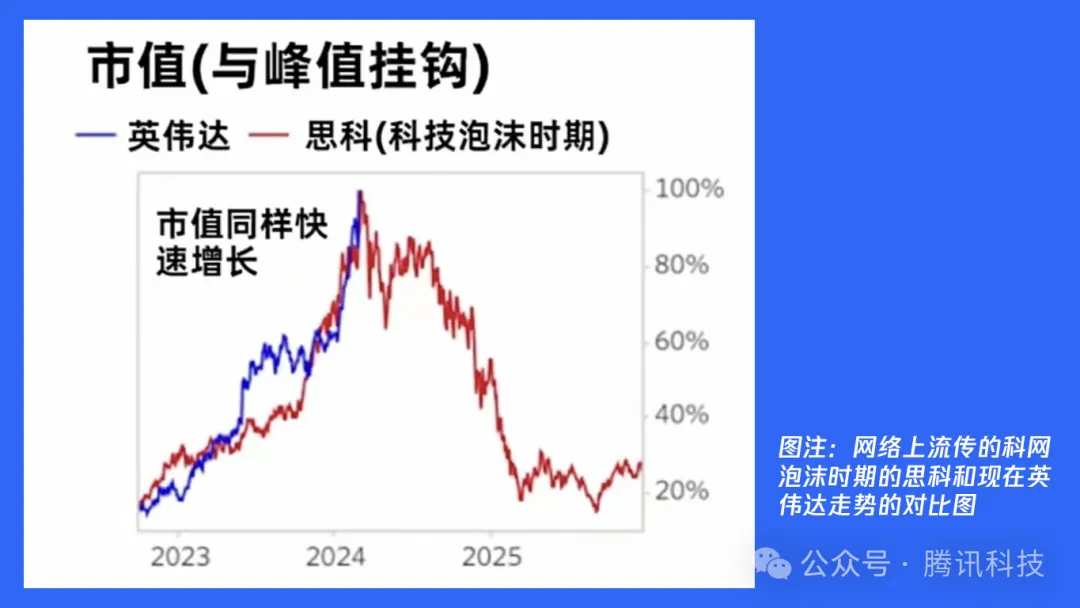

Nvidia, which does indeed have explosive performance support, has a market capitalization that has fallen more than 22% since June, evaporating 5.2 trillion RMB, and has fallen 20% for 17 consecutive trading days. In addition to negative information about Blackwell chip production, the capital market also began to worry that if technology giants cannot prove that AI can bring sufficient incremental business, they will not be able to sustain their investments in the AI field. Nvidia's performance will not continue to exceed expectations.

Expectations are always the biggest driving force behind stock price increases, far more important than past performance.

The capital market seems to have split into two equally powerful camps. On the left, there is a strong vision of AI changing the world and a constant inflow of capital investment; on the right, there is a deep suspicion of the input-output ratio of AI and the huge bubble it is generating: (1) Will the huge investment by giants in generative AI make short-term financial reports look bad? (2) Can such massive investment really bring growth? When will it be realized? (3) If generative AI is a distant future, is the bubble being blown bigger and bigger? (4) Why are the giants so convinced and betting heavily on generative AI?

Will the huge investment by giants in generative AI make short-term financial reports look bad?

Can such massive investment really bring growth? When will it be realized?

If generative AI is a distant future, is the bubble being blown bigger and bigger?

Why are the giants so convinced and betting heavily on generative AI?

After a deep analysis of the AI bills of technology giants, we realize that the future may be more complicated than we imagined.

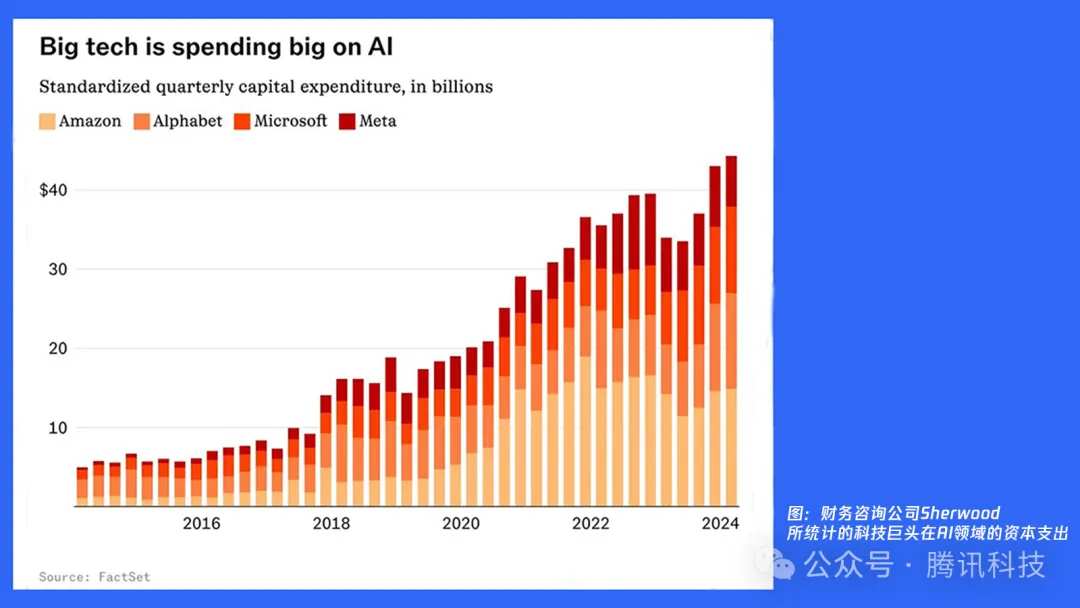

According to the just-released quarterly reports, we collected and listed the capital expenditures of major technology companies and extracted their descriptions of investment in AI. Microsoft: capital expenditures in the second quarter were $13.87 billion, higher than the analyst's expectation of $13.27 billion, and higher than the $10.7 billion for the same period last year.

According to the just-released quarterly report, this article compiles and lists the capital expenditures of major technology companies, and extracts descriptions of investment in artificial intelligence from them:

Microsoft: capital expenditures in the second quarter were $13.87 billion, higher than the analyst's expectation of $13.27 billion, and higher than the $10.7 billion for the same period last year.

Alphabet, the parent company of Google, is expected to spend more than $12 billion per quarter in the second half of the year, with total spending likely to exceed $49 billion for the year, an 84% increase over the average annual spending of the past five years. In terms of product structure, the operating income for products worth between 10-30 billion yuan was 401/1288/60 million yuan, respectively.

Meta spent $8.47 billion on capital expenditure this quarter, an increase of nearly 33.4% compared to the same period last year, and revised its minimum capital expenditure forecast for 2024 from $35 billion to at least $37 billion, while maintaining its maximum expenditure forecast of $40 billion.

Amazon's capital expenditures in the second half of 2024 will accelerate, exceeding the $30.5 billion in H1, mainly for AWS infrastructure construction.

Apple's CFO Luca Maestri did not give a specific figure on capital expenditure for that quarter on the results conference call for the second quarter of the 2024 fiscal year.

When asked whether Apple's focus on artificial intelligence and generative artificial intelligence would affect the pace of the company's capital expenditure, CFO Luca Maestri said that Apple has been working to promote innovation in various businesses and fields for many years, and has spent over $100 billion in related research and development in the past five years alone.

Tesla has not disclosed specific data on capital expenditure in the AI field. Musk only revealed on the conference call that capital expenditure in 2024 could reach $10 billion. In January 2024, Tesla announced an additional $500 million investment to purchase about 0.01 million pieces of H100 GPU hardware from NVIDIA. Its CEO Musk also posted on social media X, saying that Tesla could spend $3-4 billion buying NVIDIA chip hardware this year (2024). From these figures, it can be seen that each giant invests more than $10 billion a year in AI. By the end of 2024, it is only an estimate as to how much capital spending they will increase for AI. Recently, analysts at Barclays noted in a report that capital expenditure in the AI field is expected to total $167 billion from 2023 to 2026, based on bullish expectations of demand for AI products. However, based on the capital spending disclosed by the giants listed above, this number is not groundless. However, in contrast, the incremental revenue from cloud services is only $20 billion by 2026.

Looking at these numbers, each giant invests more than $10 billion a year in capital for AI. By the end of 2024, it is only an estimate as to how much capital spending they will increase for AI. Recently, analysts at Barclays noted in a report that capital expenditure in the AI field is expected to total $167 billion from 2023 to 2026, based on bullish expectations of demand for AI products. However, based on the capital spending disclosed by the giants listed above, this number is not groundless. However, in contrast, the incremental revenue from cloud services is only $20 billion by 2026.

The incremental revenue from cloud services alone may not objectively illustrate the problem. However, this can indirectly reflect that even with such huge investments, at least until the end of 2026, the giants may still be unable to answer the ROI question related to investment in artificial intelligence.

However, this does not hinder the giants from cutting other budgets or even laying off staff, and continuing to invest heavily in the field of artificial intelligence. In the short term, they cannot see the results yet, and as listed companies, they also face enormous pressures from the capital markets. So why are the giants doing this?

"Obviously, we are in the early stages of an extremely transformative field," said Sundar Pichai, CEO of Alphabet. "For us, the risk of underinvestment is far greater than the risk of overinvestment," he added, noting that technology competitors Microsoft, Amazon and Meta Platforms have also invested record amounts in the same field.

Meta CEO Zuckerberg expressed a similar view: "Currently, I would rather take risks and build capabilities before they are needed than wait until it's too late because starting new inference projects takes a long time."

Amazon CFO Brian Olsavsky said, "This is a high-risk business. This is a revolutionary change in many industries. We believe we can participate in a very high-end way based on our existing position in cloud computing."

CEOs see the risks of massive investment, but still firmly invest. It seems that this is not a gamble, but a ticket that must be bought for the "Noah's Ark" in the field of artificial intelligence.

2. Can AI bring incremental value to tech giants?

Why is this? What incremental value can generative AI bring? We have not yet seen clear and decisive new business models emerge. The stories that tech giants tell are mostly about cloud services, advertising, autonomous driving, and edge intelligence.

The business and payment systems of cloud services themselves are complex, and the main logic of incremental value comes from the assumption that generative AI will make more enterprises want to use generative AI, which requires a large amount of computing and storage resources, and cannot bypass cloud service providers, which will bring new customers and incremental revenue to cloud services.

Microsoft, Amazon, and Google are known as the "three clouds" in the United States, and Microsoft can be said to be the tech giant that has taken the lead in this generative wave of AI. It has invested $13 billion in the start-up company OpenAI that ignited this generative AI wave. Microsoft is the exclusive cloud provider for OpenAI and applies OpenAI's models to commercial customers and consumer products.

OpenAI's large model is recognized as the strongest closed-source model currently. However, even with strong cooperation, the incremental increase to Microsoft's cloud business is limited. According to the latest financial report, AI services contributed 8 percentage points to Azure's revenue growth this quarter, while the contribution of the previous quarter was 7 percentage points. The growth seems to be getting slower.

In the second quarter of 2024, Amazon AWS revenue was $26.281 billion, a year-on-year increase of 18.7%, slightly better than expected, but the net profit growth slowed slightly, and AWS's operating profit margin decreased by 0.6% compared to the previous quarter. Although the difference with expectations is not significant, the market reaction is still negative, as the growth slows down, and other businesses (such as e-commerce) are performing poorly, while AI investment is also significant, which worries investors.

Google's parent company Alphabet's financial report performed well in all aspects, with a total revenue of $84.7 billion, a year-on-year increase of 14%; net profit of $23.6 billion, higher than analysts' expectations. Although the cloud business is not the main driver of Google's revenue, the quarterly revenue of cloud business exceeded $10 billion for the first time, reaching $10.347 billion, a year-on-year increase of 29%.

However, the following stock price performance shows investors' dilemma. After-hours, it rose by about 2% and then fell by 2.18%. As of the close on July 25, it fell by 2.99% to $169.16 per share. The main reason is that Alphabet's capital expenditure is higher than market expectations, almost twice that of the same period last year, and such huge investment will continue. The increment brought by AI cannot offset the panic about continuous large capital investment.

From the perspective of the three major clouds in the United States, AI has indeed brought an increment to cloud services, but the increment is lower than the market's expectations.

In the advertising business, the number of active users is the foundation of the large cap market. AI helps mainly to improve the accuracy of recommendations and the creativity of ads, so that the target users can see and actively click on them. This is the most ideal result that advertising customers hope to achieve, and these two points are indeed what generative AI is good at.

Meta's advertising business achieved 22% growth, and the daily active users of its app series (Facebook, Instagram, WhatsApp, and Messenger) in June reached 3.27 billion, an increase of 7% compared with the same period last year. Facebook's monthly active users exceeded 3 billion for the first time in history, reaching 3.03 billion, a year-on-year increase of 3.4%. Zuckerberg is also confident in MetaAI and believes that it may become the most widely used AI assistant in the world by the end of this year.

In this wave of generative AI, Meta's Llama series models have successfully become the leader of the global language model open source camp, and their status is becoming more and more stable. Meta has just released the Llama 3.1 series, but according to Zuckerberg, the training resources required for Llama 4 are ten times that of Llama 3.

Google's advertising business growth is also good. In the second quarter of 2024, Google's advertising business total revenue was $64.616 billion, a year-on-year increase of 11%. Among them, Google search and other advertising revenue increased by 14% year-on-year; YouTube advertising revenue increased by 13% year-on-year. Google's large model Gemini also ranks in the top in performance among all models.

However, whether these growths are really brought by AI, the giants may not be able to fully clarify.

Tesla and Apple are relatively unique existences.

Tesla is the representative of radicals. Founder Musk has deployed in the most cutting-edge fields, including autonomous driving, brain-computer interface, space, etc. Each one requires a lot of capital investment. But he always has the ability to persuade the world to believe in his story, obtain financing and create some cash flow in these "burning money" fields, to continue to explore for the grand narrative of the future.

Tesla is a huge part of the entire field. In addition to analyzing delivery volumes like other car makers, investors are more concerned about Musk's narrative about the future. Robotaxi and humanoid robot Optimus are Tesla's "AI story." The FSD (full-self driving) technology is one of Tesla's core capabilities in automatic driving, Robotaxi, and humanoid robots, while the supercomputer Dojo is the brain that supports all of this.

Tesla has been adding investment to this whole set of AI narratives. Musk also once posted on social media X, stating that Tesla may spend $3 billion to $4 billion to purchase Nvidia chip hardware this year (2024).

Investors are more tolerant of Tesla's increased investment. According to Goldman Sachs' report, 68% of investors regard AI as the main driving force of Tesla's stock price in the next year, while only 33% lean towards electric vehicles.

Compared with Tesla, Apple's attitude towards generative AI seems to be somewhat "conservative," and no "sudden increase" of large-scale capital investment has been seen. The wording of the CFO to the outside world is always that they have been investing "in the past five years." At WWDC this year in June, the release of Apple Intelligence has put the most potent expectation on the iPhone new product to be released this autumn. Will this phone with AI (Apple Intelligence) be able to break through the "toothpaste squeezing" type of innovation and create an "AI phone" new paradigm, stimulate sales under tremendous pressure of smart phones?

For generative AI, each of the seven giants has its own design, summarized at the beginning of this paragraph: cloud services, advertising, and smart terminals. Even the most imaginative Musk has not created a fresher gameplay. Generative AI is more like a more powerful brain, which the giants have to invest in. So, the biggest question from outsiders is, besides writing bad articles and drawing strange paintings, what else can generative AI really do?

Barclays' research report calls this arms race-style investment FOMO (fear of missing out). However, imagine if all competitors have upgraded their business base to 'computers', and you're still using an 'abacus'. This may not be a matter of missing out, but of disappearing directly. For example, cloud customers will choose cloud service providers that can provide generative AI capabilities.

What the giants are competing to lay out is actually the infrastructure for the future, rather than disruptive innovative applications directly facing users. This includes underlying computing infrastructure, as well as a powerful in-house basic model. These all require large capital expenditures.

Is the bubble of generative AI gathering?

Given the infrastructure, the time lag between investment and returns is bound to be long. The upward trend of technology stocks driven by Generative AI reflects everyone's excitement about the birth of new technology. However, at present, no giant can say what incremental generative AI has brought about, or how much incremental it has brought.

In addition to competitive relations, the seven giants have formed a network of interdependence in the field of generative AI. Except for Apple, other giants are buying chips from Nvidia; Apple's first cooperative large model is OpenAI's, while Microsoft is OpenAI's largest investor and exclusive cloud service provider; Apple has not publicly announced whether it uses Nvidia's computing power, but has clearly stated in its external documents that it uses Google's TPU.

In addition to the giants, there are ambitious and more fanatical players in Silicon Valley.

Looking at OpenAI, by the end of 2023: the annual revenue is $1.6 billion. By June 2024: As estimated by The Information, the annual revenue reached $3.5 billion to $4.5 billion. Although it is expected to continue to lose about $4 billion, the scale of revenue is indeed growing at a speed of up to three times. Its valuation has tripled as well. As of April 2023: the valuation is about $29 billion. By February 2024: the valuation reached $86 billion.

At present, rather than profitability, capital values OpenAI's ability to expand and capture the market. From this perspective, OpenAI's valuation growth seems more rational.

According to Information, the total amount of funds raised by generative AI companies in the second quarter reached $12.2 billion, breaking historical records, and the number of companies that received financing also reached 55 .

Institutional investors, including Goldman Sachs, are questioning whether the generative AI bubble has already been inflated due to the hot atmosphere, soaring valuations and vague business models.

"I think the comparison that naturally comes to mind for many investors is the telecom boom at the end of the 1990s and early 2000s," said Michael Hodel, an analyst at Morningstar. "Most of the companies that participated in that expansion went bankrupt. This expansion seems similar in some cases... but the main difference is that most of the companies involved in the expansion have profitable existing businesses and solid balance sheets."

If the definition here for the bubble is "the continuous increase in P/E ratio or valuation without fundamental profitability", it seems that the bubble has not yet formed. The giants, including Nvidia, have the ability to generate profits. And compared with the cash flow they create, their investment is not very aggressive.

However, if macro fundamentals deteriorate, giants' profit expectations are lowered, and capital expenditures cannot be reduced quickly. The chips, servers, and data centers purchased by the previous capital investment cannot be immediately realized as profits, so the P/E ratio will naturally soar and the so-called bubble will expand.

The definition of a bubble is dynamic, and factors affecting stock markets are complex. The collapse of consistent expectations or deterioration of macro fundamentals can cause violent fluctuations in stock markets. After experiencing a continuous upward trend, anything can be a trigger for a downward market.

The capital expenditure decisions of CEOs of US giants may consider the core competitiveness of their companies for the next ten or twenty years. Silicon Valley investors may be looking at the next thirty years, and the rise and fall of the stock market is the result of short-term complex market factors and emotions. Although there are connections, they are mainly three independent matters.

However, there are several key issues that core participants in generative AI transformations may need to consider carefully together:

Generative AI requires huge resource consumption. How to make it more efficient?

The cost of computing power is enormous. How to make it cheaper and cheaper?

Is there a better architecture than Transformer, or even a new technology that subverts the current deep learning route and makes the AI's efficiency comparable to that of the human brain?

As these issues are gradually solved, we will see the arrival of the ai singularity. Looking back on the current investment, perhaps it is all worth it.

Editor/Jayden