Summary

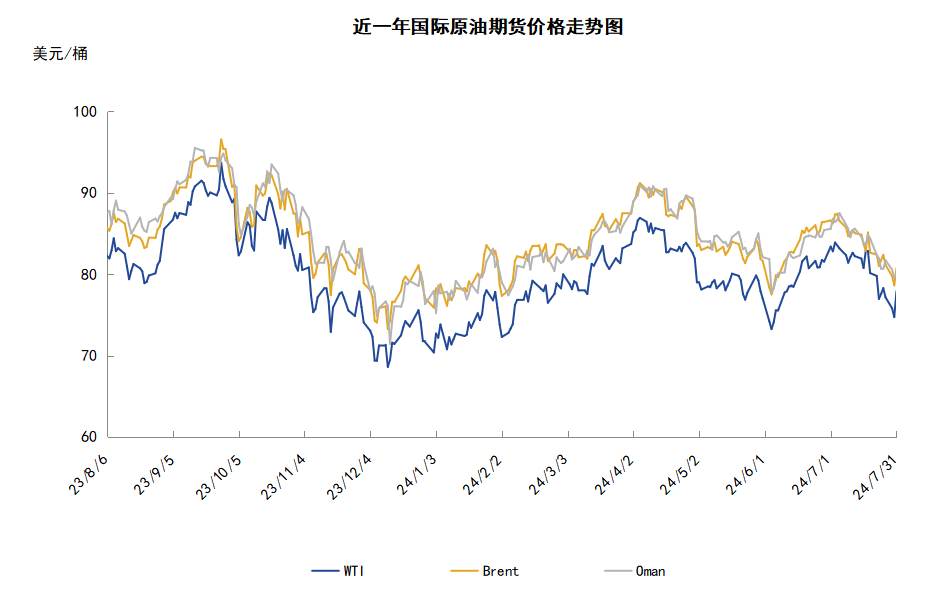

This week (7.25-7.31), crude oil showed a trend of first suppressing and then rising. The average price of WTI this week was $76.78 per barrel, a decrease of $2.68 per barrel or -3.37% compared to the previous week. During the week, the main factors that caused pressure on oil prices were the continued increase in Iraqi crude oil supply and the plan to reduce production by US refineries, which caused investors to worry about the outlook for the crude oil supply and demand fundamentals. The factors that supported the oil price were mainly the EIA data showing a reduction in US crude oil and gasoline inventories.

Chapter 1 Review of the Trends in the International Crude Oil Market

Review of This Week's Crude Oil Futures Market

This week (7.25-7.31), crude oil showed a trend of first suppressing and then rising, and the weekly average price fell compared to the previous week.

During the week, multiple bearish factors in the market news led to a drop in oil prices. On the supply side, Iraqi crude oil supply still exceeded the OPEC+ limit, and investors' worries about the oversupply of crude oil caused oil prices to fall. The Iraqi Ministry of Oil stated in a statement that Iraq's average daily oil exports in June increased by 0.051 million barrels. In addition, OPEC previously stated that Iraq's excess oil production in the first half of 2024 was about 1.184 million barrels per day. On the demand side, Valero Energy, the second largest US refiner, stated that its 14 refineries will run at 92% capacity in the third quarter, and its capacity utilization in the second quarter was 94%. As the summer driving season comes to an end, US refineries are preparing to reduce production, and investors expect US crude oil demand to gradually decrease. On the geopolitical front, two Israeli officials stated that Israel hopes to strike Hezbollah, which is backed by Iran, without a full-scale war. Israel seeks to avoid causing broader conflicts in the Middle East, easing investors' worries about the geopolitical situation in the Middle East.

However, in the latter part of the week, the reduction of US crude oil inventories provided support for oil prices. The data from the US Energy Information Administration showed that as of the week ending on July 26, 2024, the total US crude oil inventories, including strategic reserves, decreased by 2.75 million barrels to 0.808146 billion barrels compared to the previous week. US commercial crude oil inventories decreased by 3.44 million barrels to 0.433049 billion barrels, and total US gasoline inventories decreased by 3.67 million barrels to 0.223757 billion barrels compared to the previous week.

Review of This Week's Crude Oil Spot Market

This week, the international spot crude oil price fell compared to the previous period. In the Middle East crude oil market, the Abu Dhabi National Oil Company (ADNOC) predicted in a report released on July 29 that the Murban crude oil export volume in July 2025 will reach 1.768 million barrels per day, higher than the June target of 1.747 million barrels per day, setting a new record high. In October 2024, Murban crude oil exports will be 1.665 million barrels per day, higher than the expected level of 1.643 million barrels per day in September. In addition, in terms of prices, the premium of Murban crude oil plummeted because most refineries have completed their procurement tasks. Buyers are focusing on medium/heavy crude oil for September loading, such as El Sharara and Upper Zakum crude oil. As prices are attractive, a Singapore-based trader pointed out that the price of Upper Zakum crude oil for September loading has fallen to a discount of $0.15-$0.20 per barrel to the Murban crude oil for September loading. The supply and demand fundamentals of Upper Zakum crude oil are not as loose as before, but the market is still weak. In the Asia-Pacific crude oil market, data from industry institutions showed that India's crude oil imports in July decreased from 4.6 million barrels per day in June to 4.52 million barrels per day, of which Russian crude oil accounted for 43.8%, slightly lower than 44.4% in June and lower than 44% a year ago. In May 2023, the proportion of Russian crude oil in India's crude oil imports reached a record high of 46%. According to ship tracking data, Iraq was the largest oil supplier to India before 2022. In 2023, Iraq's oil supply to India is about half of Russia's oil supply, and it dropped to the lowest level in more than four years in July. Insiders said that Australia's Northwest Shelf condensate October loading plan is expected to be announced on August 5. The production of Northwest Shelf condensate oil is decreasing, and the supply is decreasing. The supply in recent months is only two ships per month, compared to three ships per month before.

Chapter 2 Analysis of Factors Affecting Crude Oil Futures Market

Supply and Demand Factors

This week, on the supply side, a large amount of new supply from the US and other regions in the Americas poured into the market, causing global statistical oil inventories as of May to increase for four consecutive months, reaching the highest level since mid-2021. It is expected that global oil inventories will be roughly balanced in the fourth quarter, even if OPEC+ plans to restore some crude oil production. Goldman Sachs stated that the crude oil market is currently tight, but in most of 2025, the crude oil market is expected to be oversupplied.

On the demand side, Fitch believes that high-frequency economic data depicts a relatively healthy picture for the energy-intensive parts of the global economy, but the performance of these parts this year is generally poor, and petroleum consumption also showed a seasonal increase this quarter. In the past four weeks, US commercial crude oil inventories have continued to decline. If this trend continues, it will indicate that oil demand is recovering. However, whether this trend is sustainable will depend on further economic recovery and changes in energy consumption patterns.

Changes in US Inventory This Week

The operating rate of US refineries continued to decline, commercial crude oil inventories decreased for the fifth consecutive week, while gasoline inventories also decreased and fractionated oil inventories increased. According to data from the US Energy Information Administration as of the week ending July 26, 2024, crude oil inventories were 1.53% lower than the same period last year, 4% lower than the same period over the past five years, gasoline inventories were 2.13% higher than the same period last year, and 3% lower than the same period over the past five years. Fractionated oil inventories were 8.27% higher than the same period last year, and 7% lower than the same period over the past five years. In addition, last week the average daily crude oil imports into the United States were 6.953 million barrels, an increase of 0.082 million barrels from the previous week, and the average daily imports of refined oil were 223.1 barrels, which increased by 0.255 million barrels from the previous week.

Fund holding situation

Speculators reduced their net long positions in light crude oil futures on the New York Mercantile Exchange by 4%. According to the latest statistics from the US Commodity Futures Trading Commission as of the week of July 23, all positions in WTI crude oil futures have declined. Total open positions fell by 1.2% on a month-on-month basis, long positions fell by 5.5% on a month-on-month basis, short positions fell by 10.4% on a month-on-month basis, and net long positions fell by 4.0% on a month-on-month basis. As the decline in short positions far exceeds the decline in long positions, the long/short ratio of WTI rebounded to 4.47, an increase of 0.23 or 5.40% on a month-on-month basis.

As the ceasefire in the Gaza region continues to strengthen, funds are beginning to withdraw from the crude oil futures market. Looking at the capital situation on the exchange, in addition to the easing of geopolitical tensions in the Middle East, the market's concerns about global crude oil demand are also starting to heat up. Due to poor travel data in Europe and America in the summer and the end of the peak season, institutional expectations for crude oil demand have also been tempered. However, the decline in long and short positions reflects a speculative sentiment that is in conflict with crude oil prices. Looking at the performance of crude oil prices, WTI crude oil futures prices have continued to decline and fell below $80 per barrel. Looking ahead, crude oil prices will correct the deviation between speculative sentiment and fundamentals. Under the premise of a weakened market expectation of crude oil fundamentals, WTI's short positions are expected to increase, or its decline will be weaker than that of long positions in the later period.

Chapter Three Outlook for Crude Oil Futures Market Trend

Market Outlook for Next Week

On the technical chart, WTI crude oil futures prices were suppressed after opening higher before rebounding during the week. The main factors that boosted oil prices during the week were: first, the assassination of Hamas political leader Haniya tightened the geopolitics of the Middle East; second, US crude oil and gasoline inventories fell; and third, US economic growth in the second quarter was stronger than expected. The main factors that weighed on oil prices during the week were: first, OPEC+ may maintain its production policy at the market monitoring meeting on August 1; second, concerns about weakening crude oil demand persist; third, China's weak economic performance may cause energy demand to slow; fourth, with the end of the peak season approaching, US oil demand will slow. As of the 31st, WTI closed at $77.91 per barrel, up 0.32 per barrel or 0.41% month-on-month. As of the week ending the 31st, WTI's weekly average price was $76.78 per barrel, down 2.68 per barrel or -3.37% month-on-month. From a technical perspective, oil prices are trending steadily.

Economically speaking, on the US side this week, the Federal Reserve is increasingly convinced that inflation will return to the target level of 2%, and the Federal Reserve will cut interest rates before the rate of price increases actually reaches this level. Recent data has indeed to some extent strengthened people's confidence that inflation is continuing to slow. The annualized inflation rate in June was 3.0%, lower than 3.3% in May. Most economists expect the first interest rate cut to take place in September, and Wall Street traders have increased their expectations that the Federal Reserve will lower the benchmark interest rate from a high of 5.25%-5.5% in 23 years. In addition, the market also expects further interest rate cuts in November and December.

Due to the rise in domestic diesel prices, Russia is considering banning diesel exports. Russia is the world's largest marine transportation exporter of diesel fuel, accounting for about 15% of the global marine transportation diesel market. Diesel is the most exported petroleum product in Russia, with an annual export volume of about 35 million tons, of which nearly three-quarters are transported by pipelines. If prices rise significantly, Russia may ban diesel exports, but no decision has been made yet.

The OPEC Secretariat said the company has received compensation plans from Iraq, Kazakhstan, and Russia for their overproduction from January to June, 2024. According to OPEC Secretariat data, during these six months, Iraq's accumulated excess daily output was about 1.184 million barrels, Kazakhstan's was 0.62 million barrels per day, and Russia's was 0.48 million barrels per day.

Iraq has repeatedly stated that it is committed to complying with the decisions of OPEC and its production cut alliance countries and will make up for overproduction. In February, Iraq pledged not to exceed a daily production of 4 million barrels, but its daily production in January-June was between 4.189 million and 4.217 million barrels. In March, Iraq stated that it would reduce the average daily crude oil exports to 3.3 million barrels to make up for overproduction, but its average daily exports in April and May were 3.41 million barrels and 3.36 million barrels, respectively.

Investment bank Goldman Sachs said that the next US president will have very limited tools to significantly increase the country's oil supply, and no matter who wins the November US presidential election, they will have to deal with low inventory in strategic oil reserves. In addition, if Trump wins, any deregulation of the US oil industry is expected to only affect the long-term crude oil production in the United States, rather than the immediate supply.

On the 29th, the US Department of Energy finalized a contract to purchase 4.65 million barrels of crude oil to supplement the Strategic Petroleum Reserve (SPR) and will be delivered in the last three months of this year.

The United Arab Emirates has been committed to increasing crude oil production. Abu Dhabi National Oil Company of the UAE has utilized AI technology to increase the capacity of one of its offshore oil fields by 25%, as the UAE hopes to increase its total crude oil production capacity to 5 million barrels per day by 2027. In May of this year, the UAE stated that its daily production capacity had reached 4.85 million barrels, higher than the daily production of 4.65 million barrels by the end of 2023.

On the 31st, the Federal Reserve kept its benchmark interest rate unchanged in the range of 5.25%-5.50% for the eighth consecutive time. Powell said that the Fed's employment and inflation risks have entered a better balance. The Q2 inflation data has increased the Fed's confidence, and it no longer needs to focus 100% on inflation. If the labor market worsens or inflation falls rapidly, the Fed is prepared to respond, and an interest rate cut in September 'may be on the table.'

JLC expects that due to the poor performance of major economies' economic data next week (8.1-8.7), the market's concerns about weak crude oil demand will continue to rise. In addition, OPEC+ may maintain its crude oil production policy on August 1st market monitoring meeting, which will increase pressure on the crude oil market. The geopolitical situation in the Middle East is still tense, and once it affects oil-producing countries, it will greatly boost the oil market. Overall, international oil prices may experience short-term volatility next week.

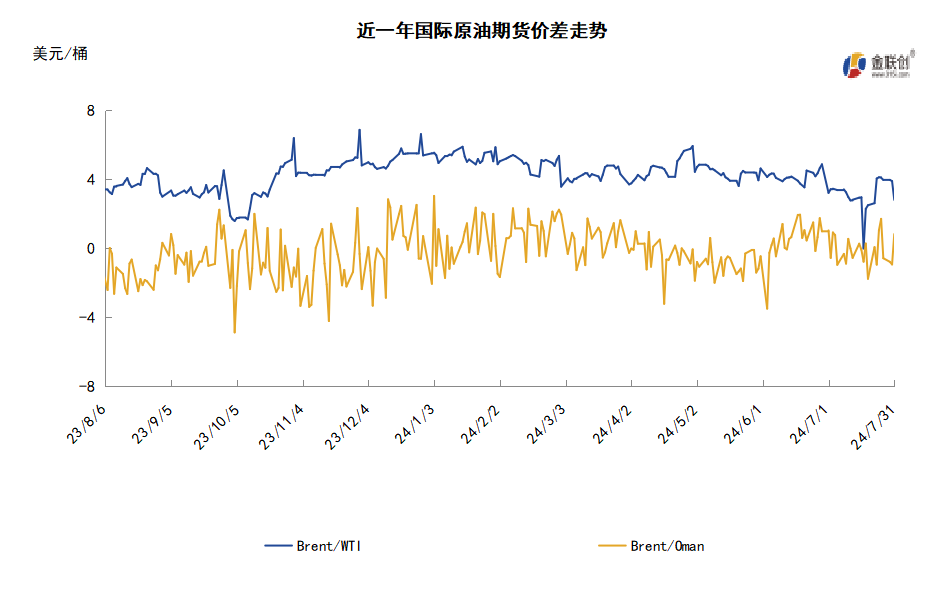

Chapter 4: Examples of crude oil futures market price differentials.

For market institutions or investors, they can pay attention to crude oil futures to participate in the crude oil market. Assuming that a certain futures institution wants to adopt a cross-period arbitrage scheme for market trading, the institution can develop a trading strategy based on the current market situation. If the month spread structure shows that the WTI crude oil futures near-future period premium expands and the far-future market sentiment has fallen, investors can hedge by buying near-term contracts and selling far-term contracts. If the overall trend of crude oil futures is downward and the price difference continues to expand, the profits from the far-term contracts will be higher than the losses from the near-term contracts, and this round of trading will still maintain a positive return.

Disclaimer

The data, opinions and forecasts in this report reflect the personal judgement of the author on the day of the initial release of the report. They are based on information that the author believes to be reliable and publicly available, but the accuracy and completeness of this information are not guaranteed. The author also does not guarantee that his/her views or statements in the report will not change. In different periods, the author may issue a report inconsistent with the data, opinions and predictions of this report without notifying anyone. The information or opinions expressed in the report do not constitute investment advice for anyone, and the cases listed in this report are for demonstration purposes only. The author is not responsible for any losses incurred by anyone using the content of this report.

This report reflects the personal views of the author and does not represent the research and judgment of JLC or ZCE. JLC or ZCE do not guarantee the accuracy and completeness of the report. The report is only transmitted to specific clients and the copyright belongs to JLC. Without the written permission of JLC, any institution or individual may not copy, reproduce, quote or reprint the report in any form.

The market involves risks, and investment needs to be cautious.