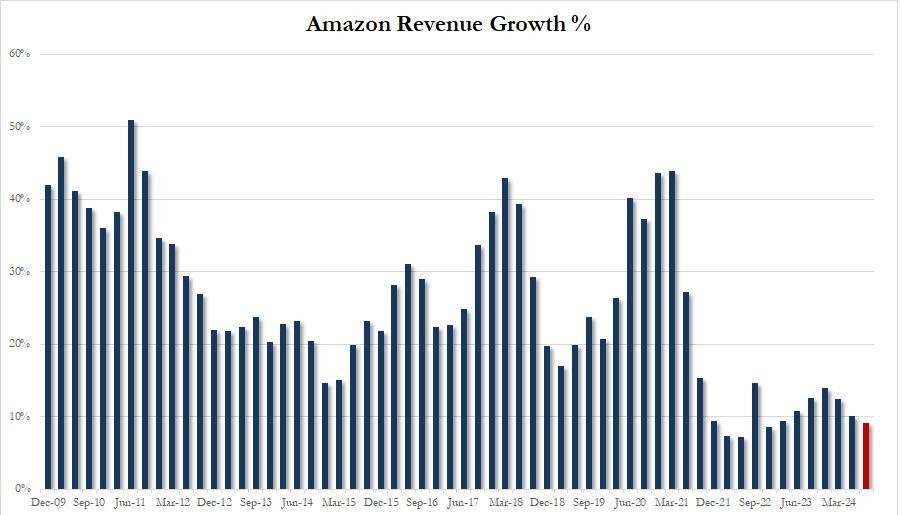

In the second quarter, Amazon's revenue and operating profit growth slowed to 10% and 91%, respectively, still exceeding expectations, and AWS cloud business revenues grew nearly 19% higher than expected. In the third quarter, revenue guidance is set to increase by a minimum of 8%, marking the slowest growth rate in over a year and a half, and operating profit guidance is greatly slowed and is expected to increase by less than 3%, reflecting the unexpected scale of investment in AI services.

Although AWS cloud business sales maintained strong double-digit growth in the second quarter, the overall sales guidance for the quarter was lackluster and raised a red flag for weak demand in the cloud business. At the same time, Amazon's third-quarter profit guidance was lower than expected, reflecting the pressure on tech giants' profits when investing heavily in artificial intelligence (AI).$Amazon (AMZN.US)$After the financial report was released, Amazon's stock fell nearly 1.6% on Wednesday, and the decline expanded rapidly, with a nearly 8% decline in after-hours trading.

Amazon released its Q2 financial data up to June 30, 2024, and provided Q3 performance guidance after the US stock market closed on Thursday, August 1.

1) Main financial data

Revenue: net sales of USD 147.98 billion in Q2, a YoY increase of 10%, analysts expected USD 148.78 billion, company guidance of USD 144 billion to USD 149 billion, Q1 YoY growth of 12.5%.

EPS: diluted EPS of USD 1.26 per share in Q2, a YoY increase of 93.8%, analysts expected USD 1.03, Q1 YoY growth of 216%.

Operating profit: USD 14.672 billion in Q2, a YoY increase of 91%, analysts expected USD 13.59 billion, company guidance of USD 10 billion to USD 14 billion, Q1 YoY growth of 219%.

Operating margin: operating margin of 9.9% in Q2, up 5.7 percentage points YoY, analysts expected 9.13%.

2) Sub-segment business revenue

E-commerce: net sales of USD 55.39 billion in Q2, a YoY increase of 4.6%, analysts expected USD 55.55 billion, Q1 YoY growth of about 7%.

AWS: net sales of USD 26.28 billion in Q2, a YoY increase of 18.7%, analysts expected USD 25.98 billion, Q1 YoY growth of nearly 17%.

Advertising: net sales of USD 12.77 billion in Q2, a YoY increase of 19.5%, analysts expected USD 13 billion, Q1 YoY growth of about 24%.

3) Performance guidance Revenue: Q3 revenue is expected to be between US$9.5 billion and US$10.3 billion, with analysts expecting US$9.7 billion.

Revenue: net sales for Q3 are expected to be USD 154 billion to USD 158.5 billion, analysts expected USD 158.43 billion.

Operating profit: operating profit for Q3 is expected to be USD 11.5 billion to USD 15 billion, analysts expected USD 15.66 billion.

After the financial report was released, Amazon's stock fell nearly 1.6% on Wednesday, and the decline expanded rapidly, with a nearly 8% decline in after-hours trading.

Q3 revenue guidance may show the slowest growth rate in more than a year and a half. Operating profit guidance slows down much more than expected.

Both revenue and profits in Amazon's Q2 slowed down compared to Q1, and the sales slowdown of its largest business, e-commerce, exceeded Wall Street's expectations. The sales growth of AWS in Q2 was stronger than expected and Q1, but AWS's operating profit margin declined slightly by 35.52% that season.

Compared with Q2 performance, Amazon's Q3 performance guidance exposed bigger problems. According to the guidance range, Amazon expects Q3 revenue to grow by about 8% to 11% YoY, with the mean below the analyst's expectation near the high end of the guidance. If the low end of the guidance forecast is correct, Amazon's Q3 revenue growth will be the slowest since December 2022.

Commentators believe that this guidance raises concerns about the precarious future of Amazon's revenue growth and cloud business prospects. The signal of lower-than-expected Q3 revenue suggests that Amazon's corporate customers are strictly controlling costs amid uncertain economic conditions, leading to weak demand for its cloud computing services.

Amazon's operating profit guidance for Q3 is all below analysts' expectations. Based on the guidance range, Amazon expects operating profit to grow by nearly 2.7% to about 33.9% YoY in Q3. Even at the high end of guidance, it's still significantly slower than the Q1's more than doubled growth rate and far lower than the analyst's expectation of nearly 40% QoQ growth.

Commentators said that the lower-than-expected profit guidance indicates that Amazon has invested more than expected in competition to meet AI service needs. Amazon CEO Andy Jassy has been cutting costs, focusing on the profit potential of Amazon's main business, e-commerce, while investing heavily in AI services. Amazon has referred to AI services as a business that represents tens of billions of dollars in revenue.

The market performance of technology companies during this financial reporting season shows that investors are becoming increasingly impatient with tech companies investing heavily in AI for profit. The shadow of cost is hanging over tech giants, and concerns about the return on investment of massive AI investments are becoming increasingly acute in the market.

Faced with market concerns, tech giants unanimously stated that they will firmly "burn money". After announcing the second quarter financial report last week, Alphabet, Google's CEO Sundar Pichai emphasized that for Alphabet, the risk of underinvestment in the field of AI is much greater than that of overinvestment.

Meta and Microsoft, which released their second quarter reports this week, are expected to increase capital spending. Meta emphasized that capital spending will increase significantly in 2025, and infrastructure costs are an important driving factor, which will continue to support AI research and product development work. Brett Iversen, Vice President of Microsoft's Investor Relations, said that the company will continue to increase spending in the future to meet "strong customer demand", and capital spending is expected to be higher than that of the 24 fiscal year in 2025.

Wall Street News recently mentioned that for enterprises, AI investment has become a survival issue rather than just pursuing incremental profits. Deutsche Bank's analysis believes that so far, the revenue has mainly been limited to the cloud business field, where enterprises train and run AI models. Outside of the cloud business, the signs of investment return are more qualitative than quantitative, and the return on investment in AI is still difficult to measure with specific numbers.

Editor/Somer