The Universal Stainless & Alloy Products, Inc. (NASDAQ:USAP) share price has done very well over the last month, posting an excellent gain of 33%. The annual gain comes to 142% following the latest surge, making investors sit up and take notice.

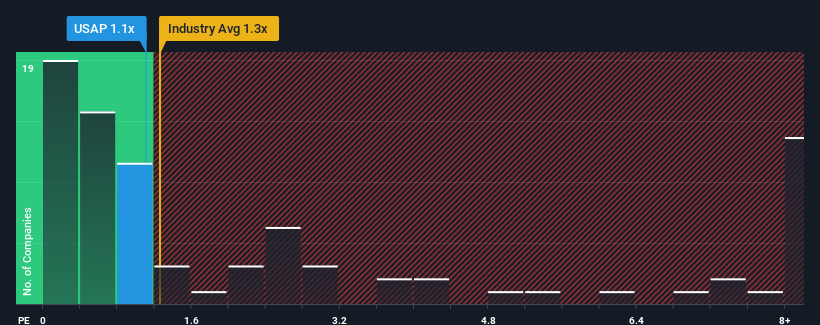

Even after such a large jump in price, there still wouldn't be many who think Universal Stainless & Alloy Products' price-to-sales (or "P/S") ratio of 1.1x is worth a mention when the median P/S in the United States' Metals and Mining industry is similar at about 1.3x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

How Has Universal Stainless & Alloy Products Performed Recently?

With revenue growth that's superior to most other companies of late, Universal Stainless & Alloy Products has been doing relatively well. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Universal Stainless & Alloy Products.Is There Some Revenue Growth Forecasted For Universal Stainless & Alloy Products?

The only time you'd be comfortable seeing a P/S like Universal Stainless & Alloy Products' is when the company's growth is tracking the industry closely.

The only time you'd be comfortable seeing a P/S like Universal Stainless & Alloy Products' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered an exceptional 31% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 116% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 9.4% as estimated by the sole analyst watching the company. Meanwhile, the rest of the industry is forecast to expand by 19%, which is noticeably more attractive.

In light of this, it's curious that Universal Stainless & Alloy Products' P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Its shares have lifted substantially and now Universal Stainless & Alloy Products' P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that Universal Stainless & Alloy Products' revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Universal Stainless & Alloy Products with six simple checks on some of these key factors.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com