The market is starting to bet on the yield curve returning to normal.

After the unexpected rate hike and balance sheet shrinkage by the Bank of Japan, the market will also face the impact of the July rate decision of the Federal Reserve tonight.

At present, the Federal Reserve is unlikely to cut interest rates, but what the market is most concerned about is the Fed's attitude towards a rate cut in September.

"No rate cut in July" is already nailed down?

The Federal Reserve will announce the July rate decision at 2 a.m. tonight, and Powell will hold a press conference at 2:30.

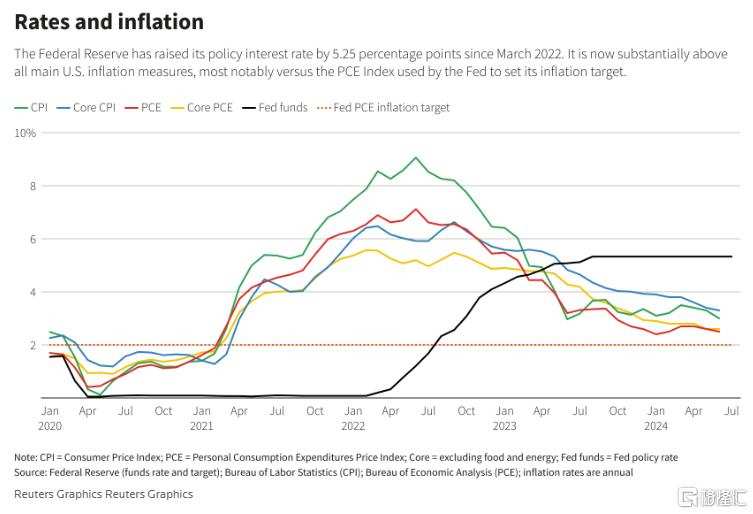

The current federal benchmark interest rate is 5.25%-5.5%, and the Federal Reserve is likely to continue to hold steady this time.

Since the last 25 basis point rate hike in July last year, the Federal Reserve has been holding steady for a year, keeping interest rates at their highest level in 23 years.

Although the probability of a rate cut is low, market participants believe that officials may at least discuss this option at this meeting.

Recently, several prominent figures have called for a rate cut in July, including former Fed Vice President Alan Blinder, Goldman Sachs chief economist Jan Hatzius, and former New York Fed President Dudley.

Data also show that US inflation is gradually sliding towards the 2% target, and a rate cut is coming soon.

Therefore, the statement after the decision and Powell's statement at the press conference will be crucial.

Will there definitely be a rate cut in September?

At present, the market expects a 100% probability of a rate cut in September, a 87.7% probability of a 25 basis point rate cut, a 11.9% probability of a 50 basis point rate cut, a 57.7% probability of a 75 basis point rate cut this year, a 32.9% probability of a 50 basis point rate cut, and a 7.4% probability of a 100 basis point rate cut, a 1.5% probability of a 25 basis point rate cut.

Bloomberg economist Anna Wong believes that the market has already fully absorbed the impact of the Fed's rate cut in September, but the biggest question at the July meeting is: How will the FOMC send this signal clearly? The July meeting statement will only provide a preliminary hint of a rate cut in September, and Fed Chairman Powell may say, "If the data develops as we expect," a rate cut may occur.

Subadra Rajappa of Natixis Bank also believes that the Fed will change the wording of its statement to suggest a rate cut in September at the meeting.

In the July statement, the Fed may emphasize the improvement in inflation prospects, describing a rate cut as achieving "further progress" in tackling inflation, rather than the "moderate" progress mentioned in the June statement.

David Mericle, an economist at Goldman Sachs, expects the Fed to modify its statement to say that it only needs to "slightly increase confidence" to begin cutting rates.

Investors expect Fed Chairman Powell to take a "dovish stance" at the press conference, hinting that a rate cut may come as early as September, which would be the first rate cut in more than four years.

Will the yield curve return to normal?

As the easing cycle approaches, bond investors are betting that the yield curve will no longer invert and eventually return to a normal positive slope.

At present, the yield on 2-year/10-year U.S. Treasuries has been inverted for two years, the longest inversion in history.

In the past few weeks, the US bond yield curve has shown a "bull market trend", with short-term yields dropping more than long-term yields.

Market investors have significantly increased net long bets on short-term government bonds (such as 2-year government bonds), while net long positions on longer-term government bonds have not increased much or have declined.

Data from the US Commodity Futures Trading Commission shows that asset management companies increased their net long positions on 2-year government bonds to a record high last week, while their net long positions on 5-year government bond futures reached a historical high in mid-July and slightly fell last week.

"The yield curve has fluctuated greatly in the past six weeks, but it is still inverted, which is not normal," said Greg Wilensky, head of US fixed income at Janus Henderson Investors.

He pointed out, "We are entering a stage where the curve is moving towards normal and positive slope, and there is still a lot of upward potential for the curve."

Editor/Emily