Commonly used valuation methods include free cash flow discount method, dividend discount method, price-earnings ratio valuation method, price-earnings ratio valuation method, market-sales ratio valuation, PEG valuation method, etc. The first 2 are absolute valuation methods, and the last 4 are relative valuation methods.

I. Free cash flow discount method

In fact, there are many methods of valuation. The most authoritative and scientific valuation method is the free cash flow discount method (DCF). When discussing valuation methods, we can never bypass the DCF valuation method.

Buffett said, “The intrinsic value of a listed company is the discounted value of the cash flow that the company can generate in its future career.” However, Munger said he had never seen Buffett calculate the company's free cash flow.

Isn't it fun for the two bosses to break up each other's platforms? Actually, there's a reason for this; keep watching and you'll see.

The calculation basis for the free cash flow valuation method is the following 3 points: the enterprise's current free cash flow, the future growth rate of the enterprise, and the discount rate at the time of calculation of valuation.

Free cash flow = operating cash flow — long-term capital expenditure. Past and present free cash flow can be calculated through existing financial data;

Future growth rate: The growth rate of the enterprise is usually expected in the next 10 years, and then a sustainable growth rate is given; 3. Discount rate: The interest rate on 10-year treasury bonds is usually used, plus a risk premium rate (usually 2% to 3%).

After these 3 key data are given, the calculation is then initiated step by step to calculate the annual free cash flow level after future growth; discount the calculated results according to the determined discount rate; and calculate the discount value of sustainable value.

Finally, intrinsic value of the enterprise = sum of 10 years' discount+permanent value discounted value

Doesn't that sound like trouble, or would it be better to use Kweichow Moutai as an example to explain.

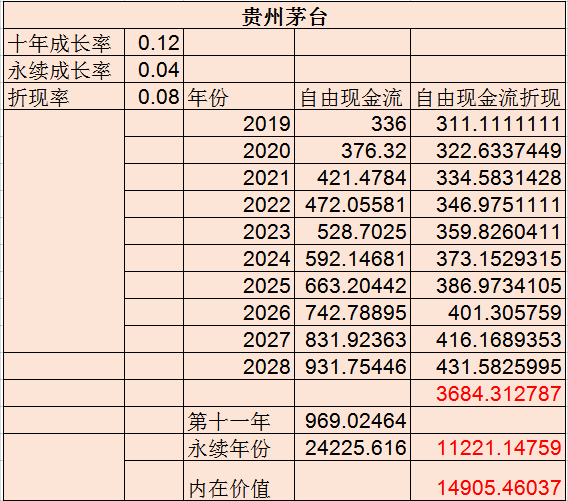

The first is free cash flow. Free cash flow = profit after tax+depreciation - capital expenses; Maotai's net profit in 2018 was 35.2 billion, depreciation was almost zero, and capital expenses (cash paid to buy and build fixed assets, intangible assets, and other long-term assets) were 1.6 billion, so its free cash flow in 2018 was 33.6 billion yuan.

The growth rate for the next 10 years is 12%, the sustainable growth rate is 4%, and the discount rate is 8%.

After calculation, it can be determined that the intrinsic value of Kweichow Moutai at the end of 2018 was around 1.49 trillion yuan.

At this point, some people may say that it seems that the free cash flow discount method is not that difficult. Build a formula, enter some numbers, and the intrinsic value of an enterprise comes out.

But what I want to say is that it really isn't that simple

In this set of calculation formulas, only one number is quite reliable, namely Maotai's free cash flow at the end of 2018, and the growth rate, sustainable growth rate, discount rate, etc. for the next 10 years are all hypothetical. For many other companies, the year-end free cash flow figure may not be very reliable.

So this set of free cash flow discounting methods brings us the most important 3 ways of thinking:

Growth is part of value, and it is a very important part; whether a business can operate for a long time is more important than growth; the risk factors faced in business operations (reflected in the discount rate) are also a very critical part of determining the value of an enterprise.

Why are you saying that? Let me answer this more carefully:

In this example, if the 10-year growth rate is assumed to be only 5%, then Maotai's intrinsic value calculation will drop to 902.7 billion, a decrease of nearly 40%; if the 10-year growth rate is assumed to be 0, then the intrinsic value calculation result will drop to 6301 billion, or about 58%.

If the company only survives for 10 years, and other conditions remain unchanged, then Maotai's intrinsic value will drop dramatically to 368.4 billion dollars, shrinking to 75.3%!

Depending on the amount of risk faced in business operations, the discount rate must be adjusted when calculating intrinsic value. When the discount rate is 9%, Maotai's intrinsic value calculation will change to 1168 billion dollars, a decrease of about 22%; if the discount rate is adjusted to 7%, Maotai's intrinsic value calculation result will become 2.03 trillion yuan, an increase of about 36.3%.

Looking at this, do you notice that there are too many factors that have changed this valuation method? Whether the 10-year growth rate, sustainable growth rate, or discount rate changes, the calculated intrinsic value fluctuates greatly.

In fact, this is true, so I actually rarely use this valuation method.

However, through today's calculation of Maotai, I found that Maotai is probably really not that expensive. After all, the 10-year growth rate of 12% and the sustainable growth rate of 4% should be quite reliable, and the discount rate of 8% seems to be a bit higher. After all, is the risk-free return rate of 6% in society now? Absolutely not! And I'm still using 2018's cash flow, and now 2019 is almost over...

II. PEG Valuation Method

The PEG valuation method was first proposed by British investment guru Slater, and promoted by Peter Lynch, the best investment manager ever in the US, and is mainly used to value growth stocks.

What does PEG mean? PEG = PE/G, PE refers to the price-earnings ratio of an enterprise, while G refers to the potential profit growth rate of an enterprise. There is a very obvious misunderstanding here. Many people use the PEG indicator to calculate the past growth rate. This is the most common misunderstanding about PEG.

Price-earnings ratio ÷ profit growth rate = PEG. If PEG > 1, you can get an overvaluation of the enterprise; if PEG <1, you can get an undervaluation of the enterprise.

As an example, if the price-earnings ratio of the current company is 20 times, if you expect the company's growth rate to be 25% in the next 3 years or so, then PEG = 0.8, then you can conclude that the company is undervalued; if you expect the growth rate of the company to be 10% in the next 3 years or so, then PEG=2 can conclude that the company is overestimated.

If PEG = 1, then it can be judged that the company's valuation is reasonable, that is, 20 PE corresponds to a 20% growth rate in the next 3 years or so, a very reasonable valuation. If PEG is 0.9 to 1.1, then there is no need to worry about such small details at all; it can be considered that the company's valuation is reasonable.

There is a problem here. If a company's future growth rate is about 5%, then how should PEG be used to value it, and should it only give a price-earnings ratio of 5 times? More exaggerated, if the company's future growth rate is 3%, will it only give 3 times the price-earnings ratio? Stocks such as Changjiang Electric Power and Daqin Railway have very average growth, but it is clearly inappropriate to give such low valuations.

If a company's price-earnings ratio reaches 50 times, the PEG valuation doesn't seem appropriate because there are too few companies that can maintain a growth rate of 50% for 3 years!

Therefore, the scope of application of the PEG valuation method is relatively narrow, and it only applies to companies with strong predictability of performance and a performance growth rate between 15 and 25%. It is not applicable to low-growth companies, cyclical companies with large fluctuations in performance, companies with price-earnings ratios greater than 30 times, etc.

OK, I'll write this much today. It's over 2000 words long. Later, I'll go on to talk about price-earnings ratio, price-earnings ratio, dividend discount methods, and market-sales ratio valuation methods that use more and are more practical.

Finally, I would like to make a special reminder that any valuation method is first based on the understanding of the enterprise. The operation of the enterprise is dynamic, and the quality of the enterprise always comes first, and the most critical factor that determines the quality of the enterprise is also the ability and moral level of the majority shareholders and management of this enterprise. Therefore, we should give priority to choosing good companies and good entrepreneurs, and only then carry out a static valuation.

The core standards that should be followed in investing are a good industry, a good company, and a good price. A good industry and a good company are prerequisites. Good prices are fundamental; none of these three are missing.

Editor/Edward