In 2023, the market share of PetroChina in the refining and petrochemical equipment industry in China is less than 1%.

Gelonghui learned that on July 10th, Richang International Holdings Co., Ltd. (hereinafter referred to as "Richang International Holdings") was listed on the main board of the Hong Kong Stock Exchange, with First Shanghai as the exclusive sponsor.

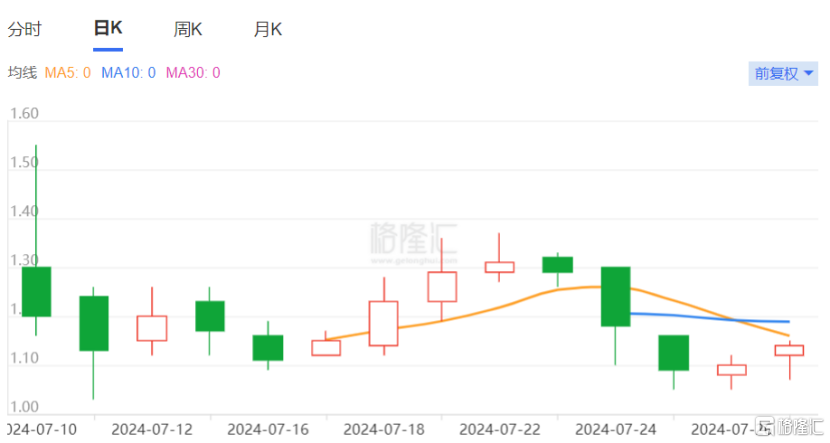

The issue price of Richang International Holdings (01334.HK) is HKD 1.05, which is located at the lowest end of the issue range of HKD 1.05 to HKD 1.39. The stock price fluctuates after the company went public. As of the close of July 29, the stock price was HKD 1.14 per share, with a total market value of HKD 0.57 billion.

Richang International Holdings stock price trend, source: Gelonghui

Established in 1994, Richang International Holdings is a manufacturer of petroleum refining and petrochemical equipment headquartered in Henan Province. The company has two production facilities in Luoyang City, Henan Province. One is responsible for producing sulfur recovery equipment, volatile organic compound incineration equipment and catalytic cracking equipment, and the other is responsible for producing process burners and heat exchangers.

The company's main market has always been in China, and it also has overseas layouts in Hong Kong, Canada and Brazil, hoping to expand market share. However, during the reporting period, the vast majority of the company's income came from contracts signed with Chinese customers, and its overseas sales office did not have substantial operations.

In this listing, Richang International Holdings will use the net proceeds of the global offering to provide funds for the construction of new production facilities. The first phase plans to build production workshops and supporting facilities for sulfur recovery equipment, volatile organic compound incineration equipment, and catalytic cracking equipment. The second phase plans to build office buildings, dormitories and auxiliary facilities; use them to enhance design and research and development capabilities; and for general operating funds and general corporate purposes.

1

Before going public, the company distributed dividends to shareholders many times but failed to pay social security contributions and housing provident fund for some employees.

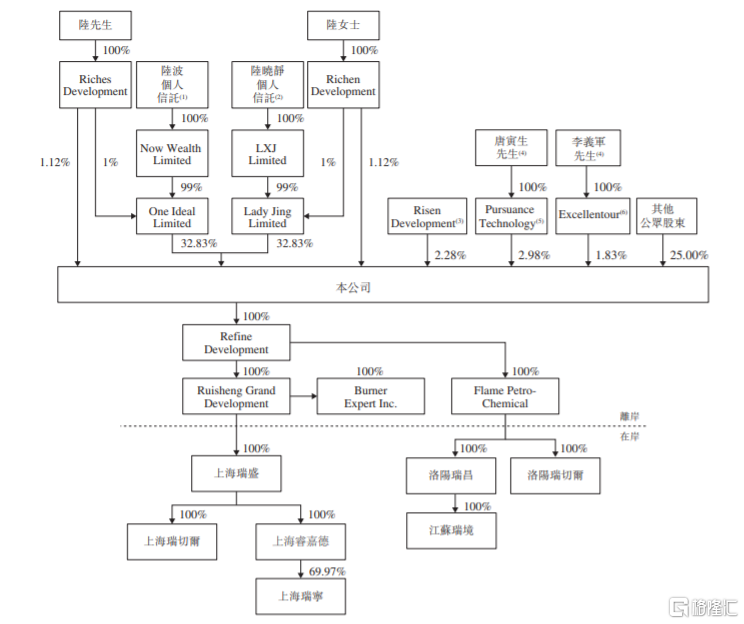

In terms of equity structure, the prospectus shows that after the issue is listed, Lu Bo holds a total of 33.95% of the shares of Richang International Holdings, and Lu Bo's sister Lu Xiaojing holds 33.95% of the shares.

Equity structure of the company after going public, source: prospectus

Lu Bo, 51 years old, obtained a college diploma in automobile application and maintenance from Luoyang Polytechnic Institute (now renamed Henan University of Science and Technology) in China in 1993, and obtained a master's degree in business administration from the China Europe International Business School in 2017. Lu Bo started working for the company in 1994 and now serves as Chairman, Executive Director, and CEO.

Lu Xiaojing, 54 years old, obtained a college diploma in mechanical manufacturing technology and equipment from Henan Radio and TV University (now renamed Henan Open University) in 1989, and obtained a master's degree in business administration from the China Europe International Business School in 2021. Lu Xiaojing also started working for the company in 1994 and is now an Executive Director and Vice President of the company.

According to the prospectus, in 2021, Richang International Holdings announced dividends of approximately RMB 19.3 million to shareholders, and the company announced a total of RMB 20 million in dividends to be distributed to shareholders based on their shareholdings in 2024, with most of these funds going to the major shareholders.

It is worth noting that the company has failing to pay social security contributions and housing provident fund in full for some employees.

Richang International Holdings estimates that the total amount of social security contributions and housing provident fund owed in 2021, 2022, and 2023 is about RMB 3.3 million yuan, RMB 3.2 million yuan, and RMB 5.1 million yuan respectively, with a cumulative amount owed of tens of millions of yuan. The company may be required to pay additional social security contributions, housing provident fund, and late fees or fines imposed by relevant regulatory authorities.

2

Relying on the top five customers.

Richang International Holdings customizes products according to customer specifications and requirements in a contract manner, and its products are divided into four categories: sulfur recovery equipment, volatile organic compound incineration equipment, catalytic cracking equipment, and process burners.

Specifically, from 2021 to 2023, the revenue ratio of Richang International Holdings' sulfur recovery equipment and volatile organic compound incineration equipment category shows a downward trend year by year, while the revenue ratio of catalytic cracking equipment category shows a significant increase.

Revenue details divided by business activity, source: prospectus

In terms of performance, in 2021, 2022, and 2023, the operating income of Richang International Holdings was approximately RMB 0.248 billion yuan, RMB 0.419 billion yuan, and RMB 0.544 billion yuan respectively, and the corresponding net profits were RMB 13.246 million yuan, RMB 36.533 million yuan, and RMB 55.211 million yuan respectively. The overall gross profit margin during the same period was about 28.6%, 31.7%, and 35.2%, respectively.

Image source: Prospectus

Because there are as many as hundreds of types of petroleum refining and petrochemical equipment, and each product category accounts for a relatively small part of the overall petroleum refining and petrochemical equipment industry, the industry is fragmented.

Based on the total revenue of 2023, RuiChang International Holdings' market share in China's overall oil refining and petrochemical equipment industry is about 0.08%. At the same time, the company is the third-largest catalytic cracking equipment manufacturer in China's oil refining and petrochemical operation with a market share of about 7.6%, and the second-largest sulfur recovery equipment and volatile organic compound incineration equipment manufacturer in China's oil refining and petrochemical operation with a market share of about 3.4%.

RuiChang International Holdings' customers mainly include market participants in China's oil refining and petrochemical industry, specifically divided into equipment owners, third-party contractors, equipment manufacturers, and others. These include subsidiaries and branches of the three largest oil refining and petrochemical groups in China, as well as one of the largest engineering, procurement, and construction (EPC) contractors in the country.

According to the prospectus, in 2021, 2022, and 2023, the revenue of RuiChang's top five customers accounted for approximately 46.9%, 75.9%, and 73.6%, respectively, of the total revenue, where revenue from the largest customers in each year accounted for approximately 20.8%, 60.5%, and 35.2% of the total revenue, a significant proportion. If there are changes in the cooperative relationship between the company and its major customers, it may affect the company's operating performance in the future.

It is worth noting that in 2021, 2022, and 2023, RuiChang International Holdings' net trade receivables and bills receivable were approximately CNY 0.16 billion, CNY 0.31 billion, and CNY 0.327 billion, respectively, showing an increasing trend annually. Among them, approximately 48.5%, 78.6%, and 65.6% of the total trade receivables in each period are owed by the top five customers, and the company faces the risk of customer delays or default in payment.

In addition, most of RuiChang International Holdings' sales are based on contracts and generally require a competitive bidding or quoting process to obtain new contracts. The equipment provided to customers by the company has an average service life of 10 to 20 years, so the company's revenue may be non-recurring. If the company is unable to continue to obtain new contracts in the future, it may affect its operating performance.