Source: Wall Street See

Barclays pointed out that Azure's second-quarter revenue growth is expected to exceed the consensus of 30.2% year-on-year. It is concerned about Microsoft's profit guidance for the next fiscal year. Continued investment in AI may lead to a slight decline in profit margin in the 2025 fiscal year.

Just last week,$Tesla (TSLA.US)$,$Alphabet-A (GOOGL.US)$/$Alphabet-C (GOOG.US)$Disappointing second quarter performance has repeatedly dragged down Wall Street, causing the Nasdaq to plunge. This week, leading more tech giants will release their financial reports, and Wall Street is eagerly awaiting to see if they can reverse the current unfavorable situation.$Microsoft (MSFT.US)$More tech giants will release financial reports this week, and Wall Street is holding its breath to see if they can turn around the current unfavorable situation.

Microsoft is scheduled to release its Q4 FY2024 (Q2 FY2024) earnings after the U.S. market closes on July 30 (early morning on Wednesday, Beijing time). The current consensus on Wall Street is that Microsoft's Q2 revenue will increase by 14.5% year-on-year to $64.36 billion (compared to Q1's year-on-year growth rate of 17%), with earnings per share of $2.93, up 8.9% year-on-year.

Barclays believes that despite high expectations from Wall Street, Microsoft is still capable of delivering a satisfying Q2 report card. However, Microsoft's stock has already risen by 14.7% this year (as of last Friday's closing), far exceeding the industry average, so the market may not react too much to the upcoming financial report. Barclays rates Microsoft as a "buy" with a target price of $475, an 11.7% increase from last Friday's closing price.

In a research report released last Friday, Barclays analyst Raimo Lenschow wrote:

"We doubt that the Q4 earnings report will be a key driver for further short-term gains in the stock price, as the market has already digested these positive signals."

Microsoft's stock price has been steadily rising since early 2024, reaching a historic high earlier this month. In recent weeks, affected by recession fears and market rotation, Microsoft has given back some of its gains. But overall, Wall Street remains optimistic about Microsoft's prospects and believes that with AI support, its stock price still has room to grow.

Barclays rates Microsoft as a "buy" and sets a target price of $475, an 11.7% increase from last Friday's closing price.

How strong is Azure business?

The market is highly anticipating Microsoft's upcoming financial report and subsequent conference call, particularly focusing on its AI product line, including cloud computing service Azure and AI assistant Copilot's performance and latest developments.

Barclays believes that Azure will have another impressive quarter, with second quarter revenue expected to grow by more than the consensus estimate of 30.2%, roughly equal to Q1's 31% growth rate.

However, due to macroeconomic uncertainties and limits on AI capacity, Barclays believes that Azure's growth this quarter may not be as strong as in previous quarters.

Wall Street expects Azure's Q2 revenue to be $1.448 billion, up 7.6% from the previous quarter, lower than the average of 11% over the past four years.

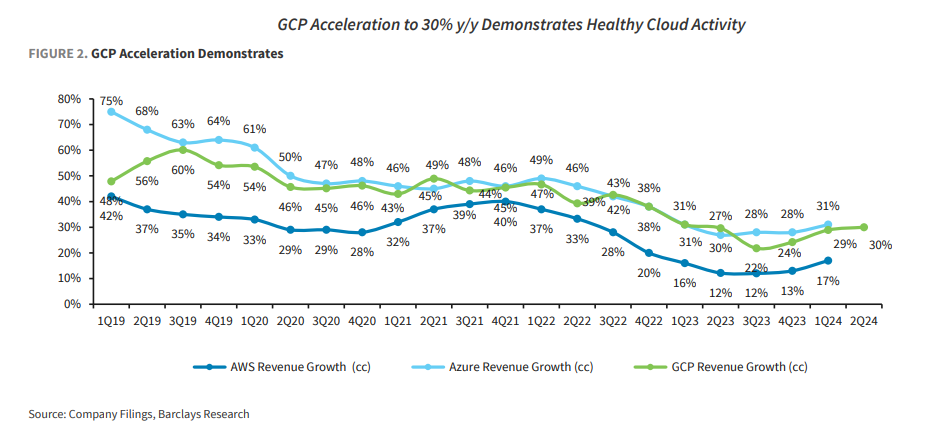

By observing network traffic data and the positive performance of Google Cloud Platform earlier, Barclays believes that market demand for cloud computing services continues to be strong, which may support Azure in achieving or slightly exceeding the upper guidance.

As for Q1 FY2025 (Q3 FY2024) and the entire fiscal year, Barclays expects Azure's year-on-year growth rates to be 29% and 28%, respectively, with expected consumer growth in AI services continuing to drive further growth on the massive base.

Microsoft's VARs (value-added dealers) survey showed that large trading activities showed strong seasonality in Q2, releasing healthy demand signals, indicating a healthy market demand for Microsoft's AI services, which provides support for Azure's short-term performance.

What is the impact of AI investment on profit margins?

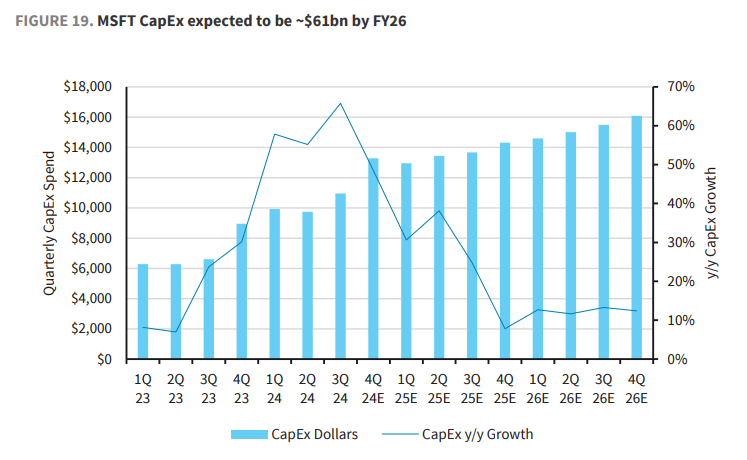

Barclays believes that as FY2025 approaches, Microsoft will increase its investment in the AI field, and related costs will increase, which may put pressure on profit margins.

In the Q1 conference call, Microsoft management also pointed out that the operating profit margin for FY2025 should only decrease by 1% year-on-year, which has already taken into account the impact of increased AI investment and the acquisition of Activision Blizzard.

Barclays is confident that Microsoft will achieve this goal, but there are some important factors to consider in the process.

For example, Microsoft's current capital expenditure may result in depreciation and amortization exceeding market expectations, further leading to a slight decline in profit margins in FY2025.

Traditionally, the second quarter has always been the peak of Microsoft's capital expenditures, followed by a continuous decline starting in the third quarter. However, this trend was broken last year and Barclays believes it may be broken again this year.

Barclays expects Microsoft's capital expenditures to increase by 20% year-on-year in 2025 and then gradually slow down to below 15% in the 2026 fiscal year.

Editor / jayden