Source: Ren Shen Gong Fen.

Unpredictable, but manageable.

1. What are some low-probability events that are likely to occur?

Every time an investment article mentions "Black Swan," there are always people who ask, "Don't bother with the useless stuff. Just tell us what Black Swan events may occur in the next two years."

I always regretfully tell them, "The biggest characteristic of a Black Swan event is its unpredictability. They are events that most people did not expect, and the events that everyone worries about are often unlikely to become Black Swan events."

But some people are still not satisfied: "I understand that. Can't you tell us which events are more likely to turn into Black Swan events?"

Huh? Low-probability events with a high likelihood? Sorry, I have to go now!

Since it cannot be predicted, what is the point of discussing Black Swan events?

The author of "The Black Swan," Taleb, divided Black Swan events into two types: those that people talk about and those that no one knows about.

As a "low-probability event," Black Swan events cannot be predicted or even avoided (i.e., the second type); but as a "common phenomenon" that is likely to occur (i.e., the first type), they can be managed and even used to make a profit.

2. We do not know what we do not know.

The unpredictability of Black Swan events creates a significant cognitive obstacle: we cannot understand its rules from past experiences, which can be seen in three aspects.

First, Black Swan events are low-probability events that are easy to overlook.

As we have analyzed before, people's first impression of random low-probability events is, "Why should I waste my valuable energy and resources on something that is unlikely to happen?"

However, there are many low-probability events in life, not all of which have significant impacts. There must be some rules, right?

Unfortunately, there are rules, but they are not reliable, which is the second reason for the unpredictability.

Second, past experiences are unreliable.

Before a rear-end collision, you always thought that the distance between you and the car in front of you was appropriate, enough for you to react, and your basis was precisely that this distance had never caused you to rear-end before.

The unreliability of experience stems from the unreliability of "induction" itself. All of our experiences may be like "the turkey's view of the farmer before Thanksgiving," which constitutes the third reason for unpredictability.

Third, what we do not know is often the most important thing.

Assuming a legislator passed a law before September 2001 requiring airlines to install bullet-proof doors in the cockpit for pilots and lock them from the inside (this is a requirement after 9/11), what would happen?

Naturally, there would be no "911". But the problem is, if "911" never happened, who would acknowledge the legislator's "contribution"? It's more likely to increase costs for the airlines and be hated by industry personnel.

The author summarizes the inescapable reason for Black Swan events: "What we don't know is more important than what we know. That's the real reason for Black Swan events."

Small probability events, unreliable experience and things we don't know are three characteristics of Black Swan events.

Of course, people always hope to take control of the situation. In the financial field, due to the system being too complex and significant, governments have designed many mechanisms to prevent the occurrence of Black Swan events.

Taking the financial crisis of 2008 as an example, the financial crisis of 2008 is not a Black Swan event to some extent. It lasted for a year and was a crisis that all markets were worrying about and all parties were mobilizing for, but they watched it happen.

In fact, this reflects the three characteristics of Black Swan events, such as small probability events, unreliable experience, and things we don't know.

Third, the crisis can only be completely resolved by letting it break out completely.

In the years before the subprime mortgage crisis, many people issued warnings in advance that the mortgage data was abnormal. Many smart investors began trading crises in advance, the most typical of which was based on the issuance of various CDOs. CDS exploded.

CDS is equivalent to a financial institution "buying insurance" for its own holdings of junior debt. They feel very uneasy but subjectively think that the problem is controllable. This seemingly cautious but actually optimistic mood hits the feature of "unreliable experience in the past" of Black Swan events.

A series of events that followed seemed to "verify" people's experiences. The prelude to the subprime mortgage crisis was opened in April 2007, and New Century Financial Corporation, the second largest junior loan size applicant, filed for bankruptcy protection, becoming the first financial institution to collapse in the subprime mortgage crisis.

At that time, the mortgage crisis was already obvious. The mortgage default rate exceeded a record of 1 million sets, but the stock market only slightly fell "to show respect" and continued to reach new highs.

The truly unpredictable black swan factor in the financial crisis is the government's "response" to the crisis- investors assume that someone is solving the problem, and therefore believe it is unlikely to cause a crisis.

In early July 2007, bond rating agencies felt that "the paper could not hold the fire", and began to downgrade the risk rating of junior debt, but the market only fell for a day.

It wasn't until late July that related fund products of the junior loan began to burst, and the market realized that the crisis had spread from junior debt to a large number of financial products. It was the most serious crisis after 9/11. The market finally had a decent "plunge" of more than 10%.

But it stopped falling in mid-August, because the government finally acted: the Federal Reserve began to cut interest rates, released liquidity, and injected more funds into more financial institutions; the Bush administration provided loan guarantees to borrowers affected by the subprime mortgage crisis; Congress is also reviewing new plans and temporarily suspending tax burdens on homeowners due to mortgage default payments; the Treasury Department established a $ 100 billion fund to purchase troubled mortgage securities...

Everyone saw that all parties were taking action, the policy was out, and the economic situation itself was very good, but it was only a credit crisis in a specific area. This crisis even passed, and the result was that the stock market not only regained its ground, but also reached a new high in October.

In fact, during the period from October 2007 to mid-July 2008, the sales of the real estate market continued to deteriorate, and the related junior debts and default rates increased sharply. The crisis continued to deteriorate throughout the entire financial system. Junior debts and related products burst continuously, and financial institutions almost suffered huge losses. But on the other hand, these problems were all covered up by the Fed's upgraded fund plan and the government's increased package economic stimulus bill.

In the contest between crisis and dealing with the crisis, most people still believe in the Federal Reserve's monetary policy and the government's toolbox, so although the market slows down, it still gains support at a relatively high level.

There were two waves of crises before the real crash came in the market. One was the crisis of Bear Stearns, and the other was the crisis of Fannie Mae and Freddie Mac. Ultimately, the crisis was paused by acquisition and government takeover.

These two "rising tide and high tide" actions give the market a wrong impression. The government's "toolbox" is now large, and there will be no major financial crises. This makes some people, including the Fed and the government, reflect on whether they are "too cautious" and whether they are too restrictive. The public is also complaining that policies waste taxpayers' money.

This "illusion" and "reflection" precisely verify what is said in Taleb's book: "What we don't know is more important than what we do know." The result is that when facing the next object that needs help, Lehman Brothers, the Fed chose another way - let it go bankrupt.

This "black swan" finally found an opportunity to reveal its true face after lurking for nearly a year. Before the Lehman Brothers bankruptcy, the market only fell 15% in a year, and in the following two months, it plummeted 40%. The subprime crisis immediately evolved into a global financial crisis, freezing the credit of the whole society and affecting the real economy. The unemployment rate has reached the highest level since the end of World War II.

Everyone knows that the best way to deal with this type of financial crisis is to inject liquidity that far exceeds the level of the crisis and strangle it in the bud. However, if the stock market does not "show you death", how can Congress pass the 700 billion rescue plan so quickly? How can major Wall Street banks accept government capital injections?

Everyone knows that the Black Swan incident caused huge losses, but everyone will question the necessary sacrifices made in advance for this. Take the Fed's interest rate hike this year as an example. Everyone knows that raising interest rates when inflation just starts is the best way, but if inflation is really suppressed by one or two interest rate hikes, most people will start to question whether there is any inflation at all. The Fed is scaring people again.

This is the fourth characteristic of the financial "Black Swan" incident: only by letting the crisis fully erupt can it be completely solved.

Therefore, specific "Black Swan events" cannot be predicted and avoided, but there are some basic coping methods for the "Black Swan phenomenon".

4. Three ways to deal with black swan

There are three different attitudes towards dealing with Black Swan incidents:

The first is Buffett's "passive use" attitude towards

The most representative of Buffett's attitude towards Black Swan events is his letter to shareholders in 1994:

"We will continue to ignore political and economic predictions, which are expensive pastimes for many investors and businessmen. Thirty years ago, no one predicted the widespread spread of the Vietnam War, wage and price controls, two oil crises, presidential resignation, the disintegration of the Soviet Union, the Dow fell 508 points in one day, or the fluctuation of short-term government bond yields between 2.8% and 17.4%.

Surprisingly, these once sensational major events have never caused any flaws in Ben Graham's investment principles, nor have they caused any mistakes in buying excellent companies at reasonable prices.

Imagine how much we would pay if we delayed or changed our allocation and use of funds because of these inexplicable fears.

In fact, we usually use the timing when certain major macro events cause the market's pessimistic atmosphere to reach its peak to find the best buying opportunity.

It seems that Buffett's attitude towards the crisis is the simplest, that is, not to predict the crisis, and once it appears, seize the opportunity to buy good companies.

This approach seems to be the easiest for ordinary people to learn, but in fact it is not, because the Apple and Coca-Cola that later made Buffett earn a lot of money were not bought in the Black Swan incident. On the contrary, when he bought them, they were considered too expensive. His investment in the aviation industry in 2020 at the “bottom of the epidemic” was actually based on the experience of the 911 incident's brief impact on aviation stocks, which was later denied by himself.

Buffett can ignore the "Black Swan", but it is also difficult to use it because the stock price shocks caused by the crisis events seem large, but for long-term investments lasting more than ten years, the impact on the ultimate returns is minimal.

The second is Taleb's "active use" attitude

Taleb's attitude is completely opposite to Buffett's. For most people, Black Swan events are risks, but if you stand on the side of the majority's trading opponents, it is a winning lottery.

Taleb has many trades based on the Black Swan theory, such as buying "5-dollar put options for General Motors" at extremely low prices, when General Motors' stock price was still above 30 dollars. It's like betting with others that Maotai will fall to 300 yuan when it's 2,000 yuan, which looks like a stupid deal, so he can buy it almost for free. But when the 9/11 attacks occurred, these put options didn't look so outrageous, and the price naturally went up. The hedge fund he managed, Empirica, had many similar investments, all of which made a lot of money during the crises of 9/11 and 2008. Product structure, 10-30 billion yuan products operating income of 401/1288/60 million yuan respectively.

"But Taleb's methods are harder to learn, and his own assessment is:"

"Expecting Black Swan events to happen is full of risk, and you will pay the price of "bleeding". You lose a little bit every day for a long time until an event occurs that gives you disproportionately high returns. No single event can cause you to fail horribly, but on the other hand, certain changes can bring you huge returns that can make up for small losses for years, decades, or even centuries."

To reduce the difficulty, Taleb later spread it into a "barbell strategy" in the book Anti-fragility, with 90% of assets allocated to almost risk-free government bonds and money market funds, and a small part of assets allocated to products like those mentioned above that can profit from "Black Swan events".

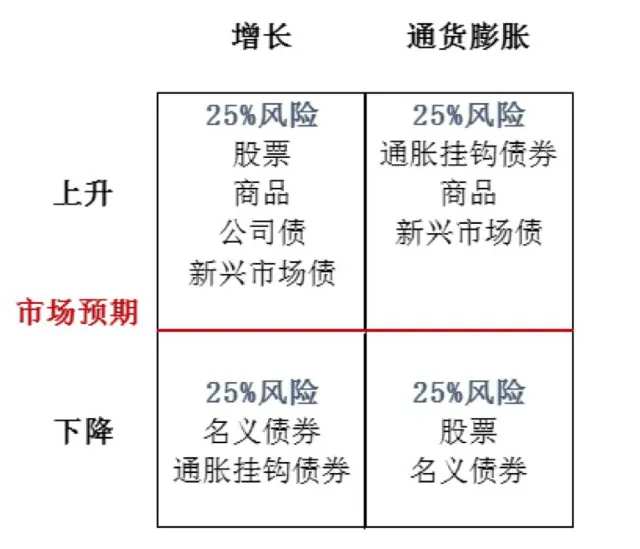

The third is Bridgewater's "all-weather strategy".

Bridgewater's most famous "all-weather strategy" model has two dimensions, "economic upswing and downswing" and "inflation upswing and downswing", forming four quadrants representing four major asset classes with equal risk weightings that correspond to four environments, allowing the portfolio to have higher yields while maintaining lower drawdowns.

Different from the traditional portfolio strategy of allocating different assets to different cycles, the "all-weather strategy" uses the above strategy to deal with all economic environments - including extreme cases such as Black Swan crises.

In order to achieve "risk parity of all assets", it is necessary to use high leverage in certain low-risk varieties (such as bonds), which requires Dalio to consider Black Swan risks as part of the overall portfolio. To this end, Dalio studied all the extreme events that have occurred in the major economies over the past few hundred years, which is obviously in conflict with Taleb's belief that"past experience is unreliable".

But in any case, Bridgewater's portfolio has survived most recent financial crises intact (although its portfolio almost "blew up" in the first wave of the global Covid-19 outbreak in 2020), and has also outperformed the market when there are no crises. As for whether it will still be effective in future Black Swan events, I hope we can know the answer in our lifetime (maybe sooner than we think).

Most of the "macro hedge fund" products on the market are derived from the "all-weather strategy", so this type of product is currently the simplest way to deal with "Black Swan events" - but if you firmly believe in Taleb's philosophy, this type of product may not be reliable.

V. Conclusion

Key points of Black Swan thinking:

1. The unpredictability of Black Swan events stems from its three characteristics: small probability events, unreliable experience and things we don't know;

2. The fourth characteristic of financial Black Swans: only by allowing the crisis to break out completely can we completely solve the crisis, so the government's response is the biggest Black Swan;

3. Black Swans are unpredictable, but can be dealt with in three ways: passive utilization, active utilization, and all-weather strategy;

Finally, there is a basic attitude that Taleb tells us: You must love failure as long as you avoid decisive failure.

Editor/Lambor