The Bank of Canada lowered the interest rate by 25 basis points to 4.50%, and hinted that further rate cuts may be made, becoming the first economy in the G7 to lower interest rates, leading to the largest gap in policy interest rates with the Fed since 2007. ING expects the Fed to cut rates in September, but the dramatic volatility in the U.S. bond market suggests that the pricing for next week's rate cut has deepened and that the doves may arrive in July.

In the wake of the Bank of Canada's rate cut, Governor Tiff Macklem's accompanying statement and news conference opening further boosted dovish pricing. He emphasized the downside risks to the economy further:"We need economic growth to rebound so that inflation doesn't fall too much, even if we work to lower it to our 2% target."

(Source:ING)

ING believes this is a fairly moderate view. At the same time, the statement also contains some cautious remarks about deflation, and the sequential meeting and data-dependent approach remains the basis for further policy decision-making. The new quarterly forecast for Canada has been released, including a target of 2.0% for overall and core inflation rates through the end of next year. GDP growth for 2024 is down from 1.5% to 1.2%, and for 2025 from 2.2% to 2.1%.

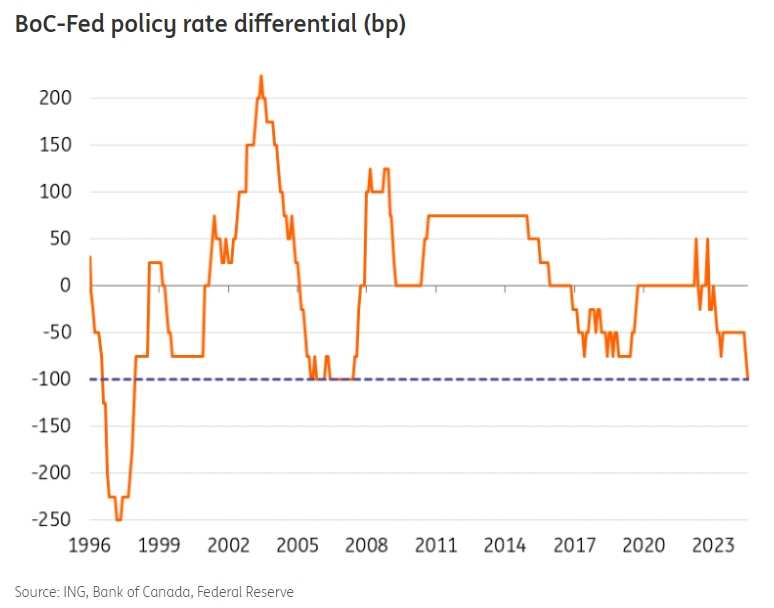

Some analysts argue that the current call to maintain interest rates is driven by concerns that the interest rate differential between the Bank of Canada and the Fed is widening and is currently -100 basis points, the largest negative differential since 2007. If the Bank of Canada cuts rates again before the Fed, the differential will be the largest in 25 years. But is this really a concern for the Bank of Canada?

(Source:ING)

McLemore said he did not believe the Fed's policy division would become a serious problem. This is understandable, as Canada's deflation process is more advanced than that of the United States, and the job market is also looser, with Canada's unemployment rate at 6.4%, 2.3% higher than the United States.

In foreign exchange, some worry that the Canadian dollar/U.S. dollar could be excessively devalued due to differences in the positions of the Bank of Canada and the Fed. However, ING stresses:"We need to note that the Bank of Canada's latest statement and monetary policy report did not mention inflation risks related to foreign exchange. By the way, since mid-July and since the Bank of Canada cut rates, the rise of the U.S. dollar/Canadian dollar pair has been only 1.2%, much less than other G10 currency pairs. We believe that as long as the U.S. dollar/Canadian dollar stays at 1.40, currently below 1.38, or even higher, there will be no discussion of excessive currency depreciation."

Despite the current meeting stance of the doves, market expectations for the September 4 meeting are only -15 basis points, perhaps because the Bank of Canada's meeting is two weeks earlier than the Fed's. After the rate cut, the year-end expectations have been hovering around -45 basis points.

ING said:"Our latest Bank of Canada forecast is in line with expectations that the Bank of Canada will pause in rate hikes in September, followed by consecutive 25 basis point rate cuts in October and December. However, Macklem's dovish comments today about disconnecting from the Fed's tight policy means a higher likelihood of rate cuts in September. This will largely depend on whether Canadian inflation continues to decline, and if there are further signs of deterioration in the job market and the overall economy, inflation rates may fall further. After all, McLemore seems to have shifted his focus from inflation to growth, no longer focusing on inflation."

ING emphasizes:"Obviously, the Fed's pricing will have some impact. If the market expects the Fed to cut rates in September, then the market may also partially expect the Bank of Canada to cut rates in September. However, in our basic forecast, the Fed will cut rates in September, and if domestic conditions permit, the Bank of Canada is likely to cut rates two weeks before the Fed. At that time, the risk of the Bank of Canada cutting rates twice by the end of the year will increase."

The Canadian dollar has not really been impacted by the Bank of Canada's rate cut, which has been fully reflected in prices. Recently, the protection of the Canadian dollar has been clearly stronger than that of the Australian dollar, New Zealand dollar, Norwegian krone and Swedish krona. This situation may continue in the short term, because the risks brought by Trump's new term are much smaller for the Canadian dollar than for other high beta G10 currencies, and the Canadian dollar's better liquidity makes it more resistant to risk aversion.

Nevertheless, the widening interest rate differential of the U.S. dollar/Canadian dollar implies that the currency pair will face continued upward pressure. ING's outlook suggests that if the market digests the impact of the Bank of Canada's rate cut in September, a breakthrough of 1.380 is entirely possible and the trend may continue to 1.390. In the short term, if the Fed eases its policy, the U.S. dollar/Canadian dollar pair may still see a pullback. "We still think it's bullish in the mid-term, and the U.S. dollar will fall below 1.350 against the Canadian dollar."

Former New York Fed Chairman William Dudley called for the earliest possible rate cut by the Fed next week to address concerns about an economic downturn, reversing his long-standing view that the Fed would stick to a long-term high-rate regime.

(Source: Bloomberg)

"The facts have changed, so I have changed my mind. The Fed should cut rates, preferably at next week's policy meeting," Dudley wrote in a Bloomberg column ahead of the July 30-31 Fed policy meeting.

For a long time, the strong performance of the US economy has indicated that the measures taken by the Fed to slow down growth are not enough because of the soaring stock market and still loose financial environment, but these facts have now changed. Dudley emphasized: "Now, the Fed's efforts to cool down the economy are producing noticeable effects."

He pointed out that low-income families are feeling the impact of higher credit card and auto loan rates as the labor market cools.

Dudley added that there were signs of a slowdown in job growth and he expressed concerns about the three-month average unemployment rate rising by 0.43% from its low point over the past 12 months to a level that could trigger an economic recession.

He said that this rate is now very close to the threshold of 0.5% determined by the Sahm Rules, which undoubtedly indicates an economic recession in the United States. Dudley's concern about the labor market is not without reason, and Fed Chairman Powell recently hinted that the weakness in the labor market now needs closer attention.

Powell testified before the Senate Banking Committee earlier this month, saying: "Rising inflation is not the only risk we face," and pointing out that "by many measures, the labor market has cooled significantly."

Meanwhile, the inflation rate continues to slow to the Fed's target level. Dudley added that the Fed's favored consumer price index, the core personal consumption expenditures index, rose 2.6% in May from a year earlier, "not significantly above the central bank's 2% goal."

Dudley acknowledged that the Fed may not want to cut interest rates too soon and take the risk of inflation rising again, and the Sahm Rules have not yet dominated the Fed's discussions.

Despite strong dovishness, market widely expects Fed voting members to vote to keep rates unchanged in the 5.25-5.5% range at next week's meeting.

Facing the further dovish rhetoric of the Bank of Canada and Mester, and Dudley's call for a rate cut by the Fed next week, traders have quickly taken action.

Bloomberg noted that the gap between 2-year and 10-year US Treasury bond yields had narrowed to about 14 basis points, the smallest gap since October 2023.

(Source: Bloomberg)

As the call for the Fed to cut interest rates as early as next week grows louder, the US bond yield curve has sharply steepened.

Further reading: Suddenly sharp steepening! US bond market sees "terrifying" trading Bloomberg: Fed to cut interest rates as early as next week...