The development of Robotaxi can be traced back to around 2010, and it officially entered the current 0-1 landing stage around 2018. Recently, the commercial progress demonstrated by Wuhan Luobo KuaiPao Robotaxi has exceeded the market expectations, and once again brought Robotaxi back to the market spotlight. In our previous report, we pointed out that the central and local governments have vigorously promoted the testing and standard development of L3/L4 level autonomous driving, and it is expected to accelerate the landing process of high-level autonomous driving. Taking this opportunity, we have reviewed the current progress of Robotaxi and the investment opportunities that we recommend readers to pay attention to.

Summary

The landing of Robotaxi is at the right time: central/local regulations are introduced one after another, and unmanned commercial operation is constantly expanding. The regulatory system for automatic driving in China and the United States is similar. The central government proposes an overall regulatory framework, and local governments carry out corresponding regulatory establishment and pilot according to their own situations. From small-scale human driving to large-scale unmanned driving. At present, many cities in China, such as Beijing, Shenzhen and Wuhan, have started pilot operations of unmanned commercialization. At the same time, many Robotaxi companies in China and the United States have carried out unmanned commercial operation, including Baidu Apollo, iDriverplus, Pony.ai, Waymo, etc. The scale of these fleets varies from hundreds to thousands of units. We believe that the increase in the number of cities that support Robotaxi opening and the number of Robotaxis allowed to be put into operation in a single city may be the two most direct observation indicators affecting the shift from Robotaxi landing from 0-1 to 1-10.

Front-end production is the preferred choice for Robotaxi; algorithm tends to be data-driven, but rule modules still need to be backed up. Robotaxi hardware has shifted from industrial-grade to vehicle-grade components, and the installation method has changed from scattered layout to platform-based kits. With the mass production and cost reduction of vehicle-grade hardware, and the convergence of configuration and commercial landing, mass production of front-loading has become possible. Various Robotaxi companies have reached cooperation with different vehicle manufacturers to support this development. In terms of algorithms, Robotaxi follows the trend of data-driven optimization of perception capabilities using large models, but it is still difficult to replace rule modules in regulatory algorithms in order to ensure safety.

We estimate that the long-term gross margin of Robotaxi may reach more than 45%, which can benefit the upstream and downstream of the industry chain. On the revenue side, Robotaxi and taxis charge passengers the same fare, but Robotaxi can operate for a longer time. On the cost side, from the perspective of operation, Robotaxi can avoid driver salary, but it also increases vehicle depreciation and remote security personnel costs. The difference here is the incremental revenue that can be obtained by Robotaxi business. The Robotaxi business chain can be divided into technology-manufacturing-operation-platform-cabin entertainment, and profit distribution depends on the competition pattern and the discourse power of each link. We believe that mastering the To-C consumer entrance and the To-B intelligent driving technology can lead to excess income.

Risk

Regulations are not as expected, intelligent driving technology development is not as expected, and Robotaxi promotion is not as expected.

Main text

Robotaxi policy regulations and commercial landing: How is the global progress?

Where is the global autonomous driving policy and regulation at?

As of June 2024, China, the United States, Germany, Japan and other countries have issued policies and regulations to support L4 level autonomous driving. Among them, Germany, Japan, and the United Kingdom have passed national laws to provide legal support for L4 level autonomous driving vehicle product standards, qualification requirements, safety officer configuration, driving range, and accident liability distribution. The legislative process at the national level in China and the United States is ongoing, and local governments as "experimental fields" have a leading role in formulating and implementing policies and regulations. We believe that the establishment of national autonomous driving laws will help standardize the development of local policies and regulations, reduce the friction costs caused by different policy and regulatory differences in the deployment of Robotaxi, and play an important role in promoting the large-scale landing of Robotaxi nationwide. Therefore, we recommend paying attention to the process of formulating national laws in China and the United States, as well as the coordination and adjustment of local and national policies and regulations.

China: The central and local governments jointly promote the construction of autonomous driving policy and regulatory system.

National legislation is underway. In March 2021, the "Road Traffic Safety Law (Draft for Revision)" was released, which for the first time clarified the requirements for autonomous driving vehicle road testing, passing, violation and accident liability determination at the legal level. However, the subject of responsibility only involves drivers and autonomous driving systems, and there are no clear regulations on the road use, violation and accident liability determination of L4/L5 level autonomous driving vehicles. We believe that there is still room for improvement in the identification of responsibility subjects, the rules of responsibility sharing, and the legal support for L4/L5 level autonomous driving vehicles.

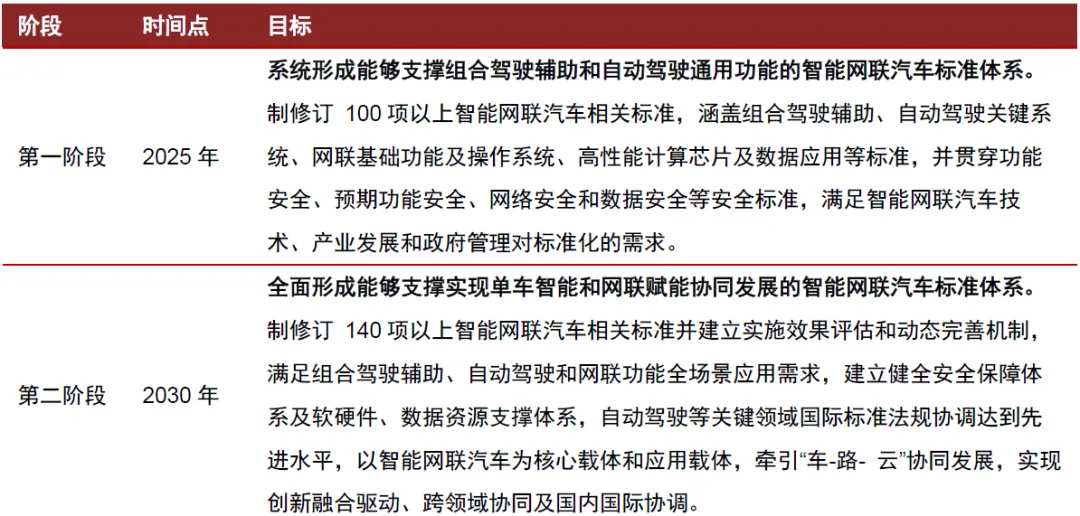

Strengthen the standard system construction. In 2023, the "National Vehicle Network Industry Standard System Construction Guidelines (Intelligent Networked Cars) (2023 Edition)" (hereinafter referred to as the "Construction Guidelines") was issued, which includes the intelligent networked car standard system covering general specifications, core technologies and key product applications. Through organizing the content of the "Construction Guidelines", we believe that in the first stage until 2025, the key directions for the improvement of the autonomous driving standards are key systems, functional safety and expected functional safety, with the aim of meeting the basic landing requirements. In the second stage until 2030, the standard system will be highly coordinated with international standards and regulations, and will meet the needs of autonomous driving in various scenarios and innovative applications.

Figure 1: Stages and Goals of Intelligent Networked Vehicle Standard System Construction

Access to automatic driving products, road testing, demonstration application, and commercial operation related guidance policies and normative documents are gradually enriched. In terms of vehicle product standards, the Ministry of Industry and Information Technology issued the "Opinions on the Management of Production Enterprises and Product Access to Intelligent Connected Vehicles" in August 2021, which stipulated the access requirements for autonomous driving vehicles and their production enterprises, providing standard references for the mass production of L3/L4 autonomous driving vehicles. In terms of vehicle road testing and demonstration application, the notice on carrying out trial pilot work for intelligent connected vehicle access and passage on the road issued in November 2023 clarified the norms for the access of L3/L4 autonomous driving vehicles, the use of main bodies, passage on the road, suspension and withdrawal, recognition of data security and cybersecurity responsibilities in accidents etc. In terms of commercial operation, the "Automated Driving Vehicle Transport Safety Service Guidelines (Trial)" (hereinafter referred to as "Service Guidelines") issued in December 2023 clearly defines the definition of an automated driving vehicle, its scope of application, application scenarios, personnel configuration, etc.

On the local level, automatic driving landing is being promoted in stages through pilot mechanisms. Beijing, Shenzhen, Chongqing, and Wuhan have allowed unmanned commercial operation pilots in vehicles. Taking Beijing as an example, in April 2021, Beijing established the "Beijing Intelligent Connected Vehicle Policy Demonstration Zone", which has undergone road testing, demonstration applications, and commercial operation pilots with "person on board" and "no one on board". The zone was officially opened for unmanned commercial operation pilot in July 2023 [1].

Figure 2: Beijing Autonomous Driving Vehicle Application Progress

On the local legislative level, Shenzhen issued the "Regulations for the Management of Intelligent Connected Vehicles in the Shenzhen Special Economic Zone" in June 2022, which is China's first intelligent connected vehicle regulation, which provides clear regulations on the design of autonomous driving vehicle products, access registration, road testing and demonstration application, and liability identification for accidents. As of May 1, 2024, the "Regulations on the Promotion of Testing and Application of Intelligent Networked Vehicles in Hangzhou" will take effect, clarifying the specific process of autonomous driving vehicles on the road through local legislation. We believe that the promulgation of the above-mentioned local regulations will provide important reference for national legislative and other provinces and cities.

USA: The federal government continues to improve its regulatory framework for autonomous driving, while state-level policies and regulations strongly support road testing and commercial operation.

At the federal level, national legislation was once obstructed, but the regulatory policy framework continues to be improved. The U.S. Congress, as a legislative body, conducted legislation on autonomous driving to prevent regulatory fragmentation. During the 115th Congress in 2017, the SELF DRIVE ACT was passed by verbal vote in the House of Representatives, and the AV START ACT was reported by the Senate Commerce, Science, and Transportation Committee. However, it did not officially pass due to differences on key issues such as safety and security. In July 2023, the U.S. Congress held a hearing on "Autonomous Vehicle Legislative Framework: Improving Safety, Quality of Life, and Mobility," which was considered by Reuters as a move to restart federal-level legislation [3]. Led by the U.S. Department of Transportation, its subordinate agencies have developed guiding documents such as AV1.0/2.0/3.0/4.0 since 2016, providing guidance on autonomous driving vehicle research and development, design, testing, and application. In recent years, it has been continuously improved in areas such as autonomous driving vehicle design and policy framework.

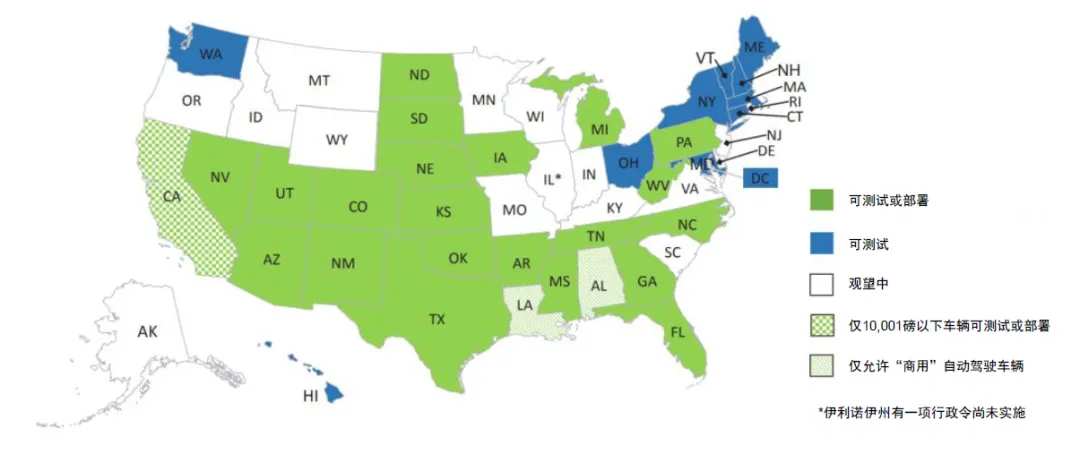

At the state level, legislative policies have blossomed and increasingly focus on safety. According to statistics from the National Conference of State Legislatures (NCSL) in the United States [4], as of May 2024, a total of 42 states have effective legislation related to autonomous driving vehicles (including definitions of autonomous driving, commercial landing, and insurance and liability determination), and places such as California, Arizona, and Texas have allowed for Robotaxi commercial operation. In California, the DMV and the California Public Utilities Commission (CPUC) are responsible for the issuance of permits for autonomous driving vehicles to be on the road and the authorization of commercial operation, as well as regulating the testing and commercial operation of autonomous driving vehicles. In the case of the growth of Robotaxi testing and commercial operation, and the frequent accidents, the California government pays greater attention to safety issues. In January 2024, it promulgated a regulation (SB-915) authorizing local governments to specify vehicle scale and service time and requiring the system developed by enterprises to ensure the control of safety personnel over vehicles.

Figure 3: Development of Autonomous Driving Related Laws and Regulations in US States (as of April 2024)

How far has Robotaxi commercial landing gone globally?

Robotaxi commercial (trial) operations have been launched in many countries. As of 2023, several cities in the United States and China have launched unmanned Robotaxi charge (trial) operations. San Francisco in the United States has approved unrestricted, all-weather, and all-unmanned commercial operations within the urban area. China has already begun commercial operation trials of driverless cars without safety employees on board (in Beijing, Wuhan, Chongqing and Shenzhen). According to the Roland Berger report, France, South Korea, Germany, and the United Arab Emirates have formally launched small-scale commercial trials with safety employees, while the United Kingdom, Singapore, Japan and other countries are in the road testing stage.

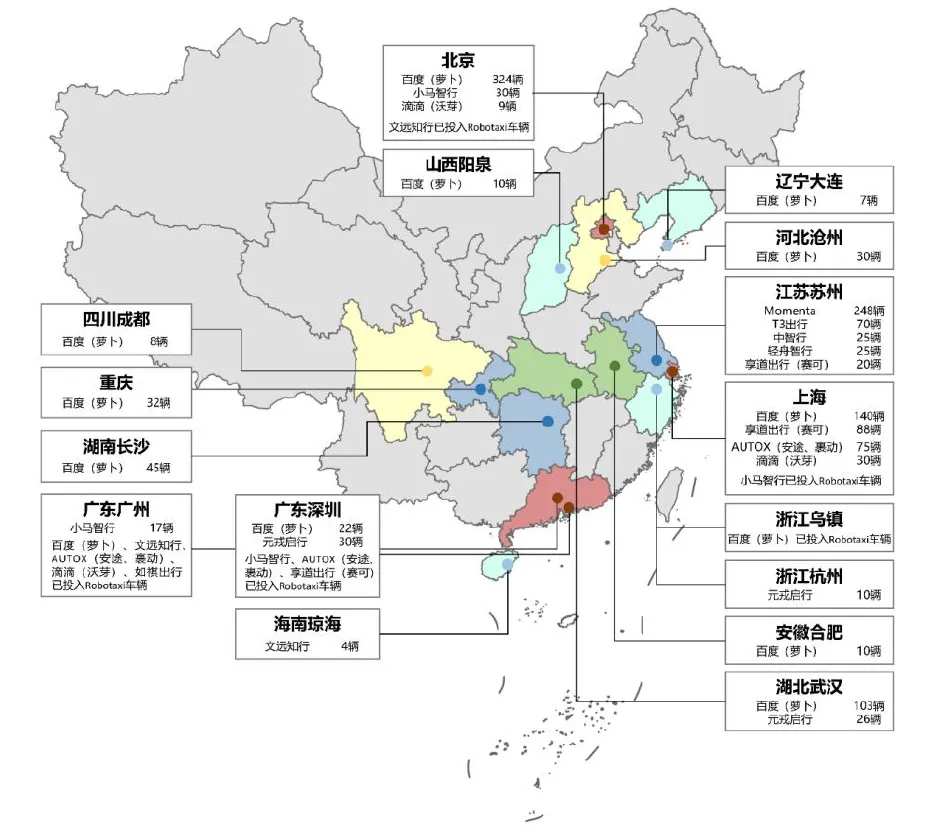

Figure 4: Robotaxi deployment in various cities in China (as of February 2023).

Unmanned Robotaxi commercial operations run throughout the day, and have been launched in the United States. According to the '2024 State of AV' report by the American Autonomous Vehicle Industry Association, by April 2024, nine cities in the United States had launched autonomous vehicle operations (including San Francisco, Los Angeles, Las Vegas, Austin, Houston, and Phoenix). The autonomous vehicle had traveled a cumulative road length of 70 million kilometers (an increase of 59% compared to July 2023). In August 2023, the California government agreed to the full-day commercial operation of Robotaxi by Waymo and Cruise in San Francisco [5]. (Cruise's operating license in California was revoked due to frequent traffic accidents). We believe that this resolution has a breakthrough significance for the deployment of Robotaxi in the United States on a large scale.

The commercial deployment of Robotaxi in the United States has slowed down after the imbalance of 2023. Due to the insufficient maturity of technology, Cruise suffered frequent accidents and pedestrian injuries after its full-day unmanned Robotaxi service was approved in San Francisco, and its automatic driving vehicle testing and deployment license was revoked in November 2023 [6]. Cruise has also suspended its Robotaxi business in the United States to regain public trust [7]. Although Cruise resumed its Robotaxi service in Phoenix, Arizona in May 2024, it ensures safety by having a safety officer seated. [8] We believe that the deployment of commercial Robotaxi should be based on the safety and reliability of Robotaxi. Active government supervision makes better solutions obtain more resource tilts.

Figure 5: Partial autonomous deployment of some states in the United States (as of May 2024).

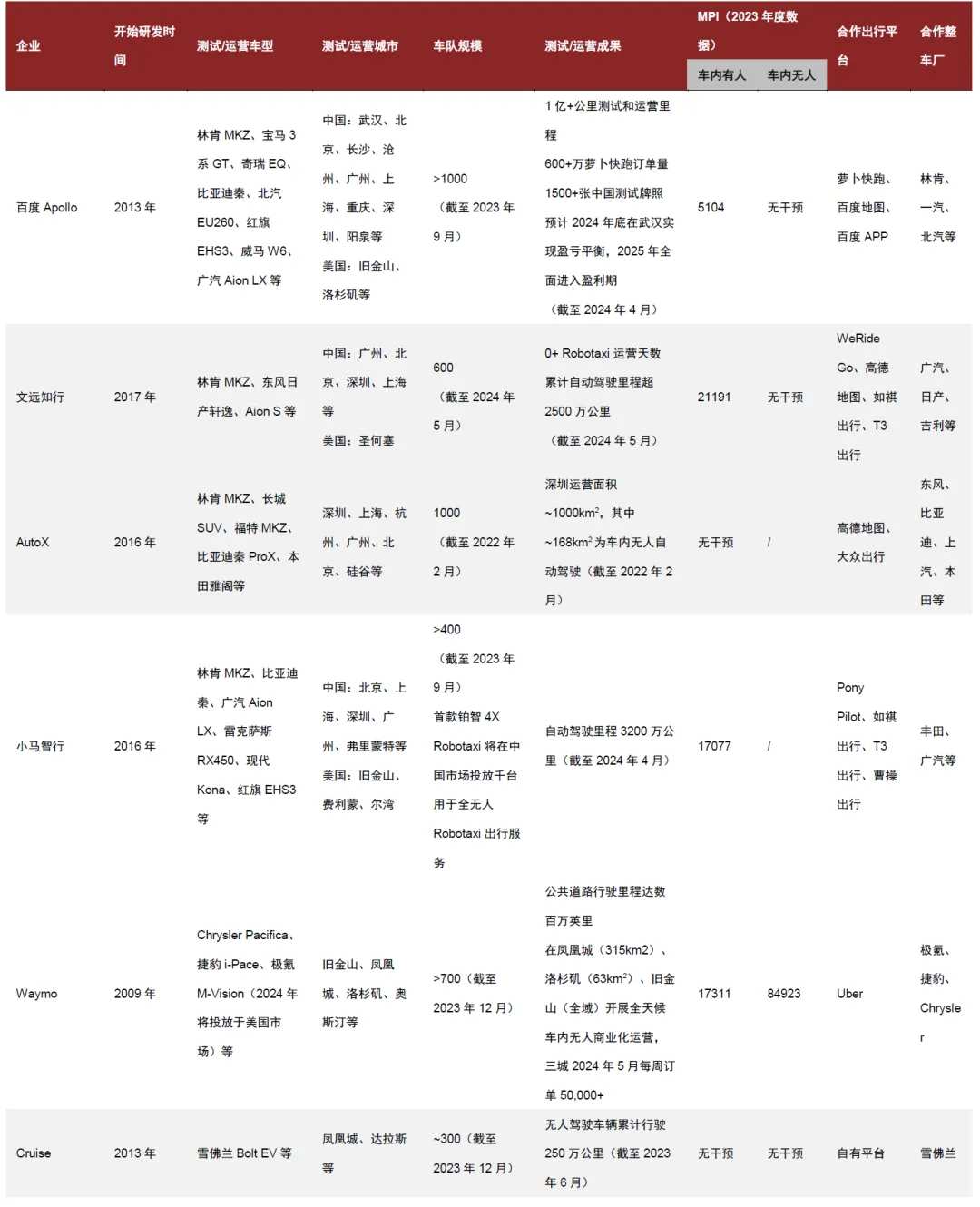

Robotaxi enterprises in China have strong momentum to catch up. Although China first issued road test licenses for autonomous driving cars in March 2018 [9], and many Robotaxi companies started late, Chinese Robotaxi companies have advantages in 1) larger-scale commercial landing size; 2) stronger reliability of autonomous driving systems, realizing passenger miles per intervention (MPI) of more than 20,000 miles and driverless operation; and 3) competitive testing and operational mileage, order quantity, and scale of fleets.

Figure 6: A summary of major Robotaxi enterprises' operations at home and abroad.

Note: 1) Company MPI (per manual intervention mile) depends on the company's selected road test route, density, and road test vehicle model; 2) '/' means the company did not conduct this test or operation in California in 2023; 3) The specific time range of '2023' is from December 2022 to November 2023.

Data source: various company official websites, California DMV Autonomous Vehicle Road Test Report 2023, Cyber Automotive, Verge, Low-Speed Unmanned Driving Industry Alliance, Research Department of China International Capital Corporation.

Robotaxi software and hardware technology and production status.

Hardware end: reuse of vehicle-level components, improved reliability and cost-effectiveness.

Sensors: further support for front-loading mass production.

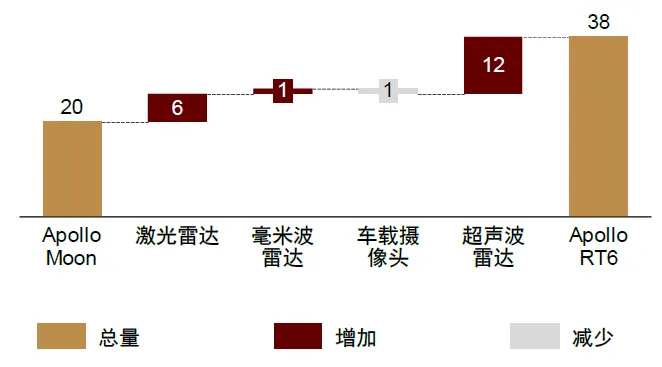

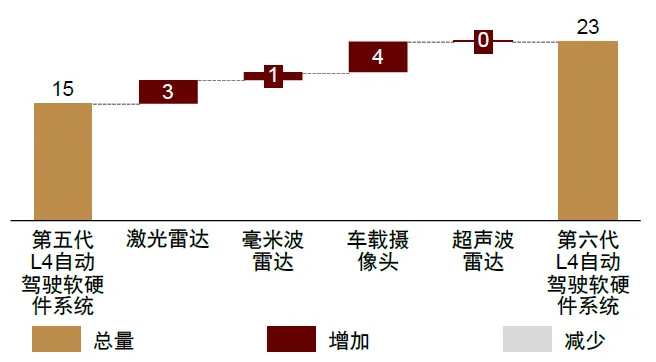

By comparing the number of sensors in the fifth and sixth generations of Robotaxis of Baidu Apollo Moon and RT6, and Xiao Ma Intelligent Control, we find that the main increase is in LIDAR (Light Detection and Ranging) sensors. We believe that the increase in the number of sensors is mainly due to 1) the optimization of sensor configuration and cost reduction. For example, the configuration of LIDAR has changed from a mechanical steering half-solid-state main radar + pure solid-state filling blind radar combination (such as Baidu Apollo RT6), and the price shows an obvious trend of cost reduction. For example, on the first-quarter earnings conference of Velodyne, the ASP of ADAS LIDAR was reduced from 4,000 yuan in 1Q23 to 2,600 yuan in 1Q24; 2) the commercial use of Robotaxi has increased the requirements for safety/reliability, thus increasing the redundancy of sensors and realizing 360° coverage of cameras, LIDAR and millimeter wave radar; and 3) the front-loading mass production of Robotaxi can have more space to integrate various sensor configurations. According to the Wayve official website, the single-vehicle sensor program that achieves Level 4 autonomous driving typically includes 15-30 on-board cameras, 5-20 millimeter wave radars, and 5-7 LIDARs. We believe that the number of sensors will be relatively stable in the future when the redundancy of 360° coverage is achieved in most cases.

Figure 7: Detailed distribution of sensor increase in Apollo Moon and RT6 models of Baidu.

Chart 8: Xiaoma Zhixing's fifth and sixth generation L4 automatic driving software and hardware system sensor incremental breakdown.

Chart 9: Major autonomous driving companies sensor and computing power configuration (as of June 2024).

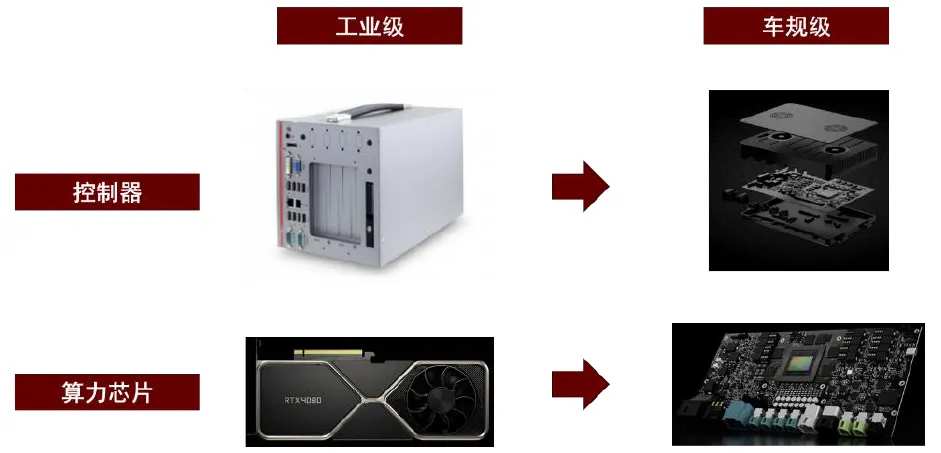

Computing power platform:

Evolution from industrial computer to vehicle-grade computing power platform. At present, Robotaxi in the testing and validation stage generally uses industrial computers as on-board computing power, that is, industrial-grade computing power platforms. Industrial computers usually use industrial-grade CPUs and GPUs, with a wide working temperature range than room temperature but narrower than vehicle-grade. The disadvantage of industrial computers is that their reliability is not as good as that of vehicle-grade hardware, and their integration degree is lower, resulting in higher deployment difficulty and limited space for cost reduction. With the trend of large-scale computing chips for vehicles, such as Nvidia Orin-X and Thor, L4 autonomous driving companies may gradually change their hardware solutions and transform industrial computers into vehicle-grade domain controllers to improve reliability and lifespan, as well as lay a foundation for subsequent large-scale production cost reduction.

Chart 10: Evolution of computing power platform from industrial grade to vehicle grade.

Wired chassis:

As cars move towards the era of intelligence, wired chassis technology is indispensable. Advanced autonomous driving relies on the efficient coordination of the perception layer, decision-making layer, and execution layer. A high-precision, fast-response, safe and stable execution system is a necessary condition for achieving advanced intelligent driving. Traditional mechanical and hydraulic control technology cannot meet the requirements. We believe that wired chassis is one of the core revolutionary technologies for mass production of autonomous driving, which not only improves the performance of L2 and L3 level intelligent driving cars, but also prepares for L4 and above autonomous driving.

Robotaxi vehicle cost continues to decline.

Vehicle cost has fallen to the level of mainstream passenger vehicles. According to Baidu Apollo Day 2024, Baidu's sixth generation unmanned vehicle RT6 is priced at only 0.2046 million yuan, a 60% drop compared to the fifth generation unmanned vehicle's 0.48 million yuan. After summarizing and integrating the cost evolution history of Baidu's Apollo sixth-generation unmanned vehicles, we believe that this is mainly due to the large-scale effect of Robotaxi front-loading production, autonomous driving components evolving into vehicle-grade products, and China's abundant production capacity for electric vehicles.

Chart 11: Robotaxi cost reduction path - using Baidu Apollo Robotaxi as an example.

Note: The price column Gen1~Gen4 data is extrapolated based on the publicly available information from the Baidu Apollo Robotaxi performance improvement of ten times and cost reduction of half in Apollo Day 2021. Source: Baidu Apollo official website, MEMS, Electric Technology, Autohome, Zhijia Net, China International Capital Corporation Research Department.

Source: Geshi Auto WeChat Official Account, 2022 Baidu World Congress, China International Capital Corporation Research Department.

Software side: modular architecture is dominant, and end-to-end architecture has broad prospects.

We believe that the transition from rule-driven to data-driven still requires some time, and rules may still be needed in the future. The commercialization of Robotaxi requires high safety and reliability of the autonomous driving system for various unknown and extreme scenarios, which requires a large amount of on-site and simulation testing and analysis of the model behavior. Therefore, the model should be verifiable and interpretable. However, end-to-end models are currently a "black box", and we have difficulty understanding which data, methods and reasons the model relies on to make decisions, making it difficult to make targeted modifications in case of errors or changes in requirements. Data and computing power determine the ceiling of end-to-end models, but model optimization requires a large amount of high-quality data. However, how to obtain low-cost, efficient, and high-quality data still depends on L4 autonomous driving solutions. Under the current situation of incomplete data infrastructure such as computing power, data-driven algorithm results may not be better than rule-driven ones. Therefore, we believe that data-driven algorithms are more suitable for improving perception performance, while rule-based algorithms are still needed for regulation and safety.

Ecology, technology, and policies in place are driving Robotaxi into mass production.

The mass production of Robotaxi requires both autonomous driving technology companies and automobile manufacturers to work together. Autonomous driving technology companies need a certain scale of vehicle fleet as carriers to carry out road testing, demonstration applications, and commercial (trial) operations, in order to accumulate data, optimize models, and promote commercial model improvements and adjustments. However, expensive retrofit vehicles will increase their financial pressures. In the short term, automobile manufacturers will improve their production and sales by manufacturing and selling Robotaxis, and in the long run, they hope to enter the L4 level autonomous driving race. Therefore, autonomous driving companies and automobile manufacturers have carried out in-depth cooperation in vehicle architecture, chip selection, and network architecture to jointly develop new models for Robotaxi. We believe that the process and results of this cooperation will help autonomous driving technology companies promote the commercialization of Robotaxi, and automobile manufacturers accumulate L4 level autonomous driving technology.

Figure 12: Progress of mass production by autonomous driving enterprises (as of April, 2024)

Robotaxi profit model and value chain.

Robotaxi profit model: below 0.4 million yuan per car is at break-even point.

Based on the entire Robotaxi value chain, we constructed a single-car and single-year economic model to estimate the profit capability of Robotaxi. The participants in the Robotaxi value chain are numerous, and the cooperation models are diverse. The cost burden and profit distribution vary due to specific cooperation models, and the demands for ROE vary in terms of the scarcity and value created in each link. At present, the commercial operation of Robotaxi is still in its infancy, and the details of cooperation between various parties have not been fully formed. Therefore, we take a perspective of the entire value chain to construct a single-car and single-year economic model for Robotaxi, attempting to establish a comprehensive understanding of its profit capability.

We calculated the annual revenue of Robotaxi per car through "Robotaxi average unit price x daily average number of Robotaxi x 365".

►Assumption #1: The average unit price of Robotaxi is set at a certain discount compared to traditional online car-hailing to compensate for the experience drawbacks caused by imperfect technology. We assume that the unit price of traditional online car-hailing platforms will increase by about 3% annually. In addition, we believe that in the early stage, there is still room for optimization in the Robotaxi experience, and we are willing to set lower unit prices for C-end customers to make it a more economical means of transportation; later, as the riding experience of Robotaxi becomes similar to that of online car-hailing, the relative discount provided by online car-hailing platforms will be recovered.

►Assumption #2: Compared with traditional online car-hailing, the total daily operating time of Robotaxi is longer, and the number of orders per unit time increases with the maturity of technology and production acceptance. We reasonably assume that the daily unit order volume of online car-hailing is 20 orders. According to the "Research Report on Travel Platforms in China's First-tier Cities in 2021" published by the team of Tsinghua University, the average daily operation time of online car-hailing in China was about 11 hours in 2021; taking Beijing Yizhuang as an example, in July 2023, Luobo Kuaipao operated here from 7:00 to 22:00 every day (15 hours). We believe that with the maturity of technology and the relaxation of regulatory policies, the daily operating time of Robotaxi may reach 20 hours in the future (the remaining time is used for recharging and cleaning). Longer operating time means covering non-peaking travel periods, but the marginal effect of operation will be lower than human drivers due to the low order efficiency of Robotaxi per unit time. Therefore, we set a discount of operating efficiency to calculate the daily orderable quantity of Robotaxi.

We calculated the annual cost of Robotaxi per car through "vehicle depreciation + remote safety officer costs + power costs + platform costs + insurance costs + maintenance costs".

►Assumption #3: The cost per car of Robotaxi first decreases and then stabilizes, with a life cycle of 5 years. In the short and medium term, as the price of the autonomous driving kit decreases and Robotaxi front-loading mass production scales up, we believe that Robotaxi costs will gradually decrease. In the long run, we expect that the scale production of Robotaxi will reach a stable level around 2030, and the development of autonomous driving technology will enter a mature stage, so the cost will remain stable. Assuming that Robotaxi travels 0.01 million kilometers per month on average, and based on the "Mandatory Scrapping Standard Regulations for Motor Vehicles", we estimate that the total life cycle mileage of Robotaxi is 0.6 million kilometers, so we expect its life cycle to be about 5 years, with linear depreciation and zero residual value.

Assume #4: The number of remotely supervised vehicles for Robotaxi will increase, and it will remain stable in the long term. Taking Beijing Yizhuang as an example, Robotaxi has achieved a 1:1 ratio of human safety supervisors to vehicles. Some leading service providers have been approved to conduct L4 level testing at a ratio of 1:5. With the continuous maturity of autonomous driving technology, the safety and reliability of Robotaxi may be further improved. Therefore, we assume that the future human safety supervisor to vehicle ratio of Robotaxi will gradually decrease, and the number of vehicles supervised by a single safety supervisor will increase. When the technology is mature in the long run, the ratio will enter a steady state.

Assume #5: The power cost, platform cost, insurance cost, and operation cost of Robotaxi will remain stable as a percentage of revenue. We assume that the power cost, insurance cost, and operation cost of Robotaxi as a percentage of revenue will be similar to those of traditional online ride-hailing platforms and basically remain stable. The platform cost as a percentage of revenue will decrease. The power cost mainly includes electricity cost, as Robotaxi is basically a new energy vehicle. The operation cost mainly includes vehicle maintenance costs (such as replacement of parts during the vehicle lifecycle) and parking fees. As for insurance costs, before the pricing model is clear, it can refer to the pricing of passenger vehicles. But with the gradual validation of Robotaxi safety, its proportion of revenue may gradually decrease year by year. The platform cost mainly includes the IT costs of self-built and third-party platform commissions, data storage and server operation and maintenance, etc. The upper limit of the commission is mostly between 18% and 30% [10]. However, considering that self-built platforms are rising and their voice is gradually increasing, we assume that the platform cost as a percentage of revenue will decrease in the future.

Based on the above assumptions, we expect the gross margin of Robotaxi to turn positive in 2027, and the long-term gross margin to exceed 45%. In terms of revenue, Robotaxi runs for a longer period of time, so the daily order volume can be higher than that of traditional online ride-hailing, thereby achieving higher revenue in the long term. In terms of costs, with the decrease in the number of human safety supervisors and the decrease in the in-vehicle kit cost and the Robotaxi front-loading mass production, the proportion of vehicle depreciation and safety personnel costs as a percentage of revenue will approach 28% and 10%, respectively, around 2030, releasing greater gross margin space.

Chart 13: UE Analysis of Mid-term Single Car Model of Domestic Robotaxi

Note: For more detailed assumptions and long-term estimates, please contact the Automotive Group of the Research Department of China International Capital Corporation.

Source: China International Capital Corporation Research Department

Robotaxi Value Chain Breakdown

The Robotaxi value chain can be divided into five layers, including autonomous driving technology, dispatching platform, and services as the core layer of the value chain. The first layer of autonomous driving technology includes algorithm software and core computing chips that realize autonomous driving, which is the technical foundation for autonomous driving and has a high technical threshold. The second layer is the design and production of autonomous driving vehicles and corresponding parts. The third layer is fleet operation and insurance, mainly providing transportation, operation, and insurance. The fourth layer is the dispatching platform and service, which provides the Robotaxi To-C entry and has a higher voice in vehicle dispatching. Its resource orientation and demand docking efficiency relate to Robotaxi's profit-making ability. The fifth layer is passenger demand and experience, which builds intelligent cabins and improves passenger riding experience. We believe that autonomous driving technology (especially algorithm software providers) and dispatching platforms and services each control the two core resources of technology and customers, and both have high thresholds, so they have a higher status in the value chain and have a higher voice in the distribution of industry interests.

Chart 14: Layered Structure, Key Participants and Major Value Contributions of the Robotaxi Value Chain

Note: "Gross margin level evaluation in 2023" data represents the average gross margin or net margin of the company in 2023, calculated by calculation.

Source: Mobileye prospectus, representing the 2023 annual report of the company, China International Capital Corporation Research Department.

The 'Iron Triangle' model composed of autonomous driving technology companies, vehicle manufacturers, and ride-hailing service platforms promotes the commercialization of Robotaxi. In the 'Iron Triangle' model, each party is responsible for technology, production, and operation, respectively, and cooperates to improve the technology, mass production, operation and service, and market acceptance of Robotaxi, accelerating its commercialization.

Autonomous driving technology companies specialize in L4-level autonomous driving solutions under the 'Iron Triangle' model. They deploy vehicles through their own platforms or through third-party companies to obtain driving data to improve their algorithms. Cooperation with vehicle manufacturers to achieve mass production helps save vehicle production costs and improve reliability.

We believe that vehicle manufacturers are driven by short-term sales and long-term visionary layouts of the huge Robotaxi market, but their autonomous driving technology is relatively backward. Under the 'Iron Triangle' model, they provide vehicle design and manufacturing to support vehicle deployment, profit from vehicle sales, and accumulate experience in high-level autonomous driving systems.

We believe that Robotaxi is a business that can leverage its user base advantages and is helpful for increasing revenue scale in the long term for ride-hailing service platforms. Under the 'Iron Triangle' model, they are responsible for vehicle dispatch and maintenance affairs, C-side user drainage and education. Meanwhile, the platform can flexibly intersperse online ride-hailing and Robotaxi to ensure the wait time is controllable, guarantee the passenger experience and pickup rate of autonomous driving vehicles, enhance user stickiness, ensure order volume and revenue.

In addition to the 'iron triangle' model, we believe that the Robotaxi business may also land in a C2C model. After the automatic driving technology and Robotaxi vehicle production reach a certain level, L4 level automatic driving vehicles may be sold to ordinary consumers under policy and regulations. According to the speech by Tesla CEO Elon Musk at the 2024 shareholder meeting, the Tesla Robotaxi operation mode will be a combination of 'Uber and Airbnb': Tesla's own fleet operation mode is similar to Uber, and the vehicle owner's idle vehicle operation mode is similar to Airbnb: owners can add idle vehicles to Tesla Network (Tesla's travel platform) fleet at any time, and jointly provide taxi services to users with Tesla's own Robotaxi, and can withdraw as needed. Vehicle owners can earn income from taxi services, and Tesla, as the operating platform, will take an extremely low percentage cut of the income. As a result, some insurance costs, energy costs, and vehicle depreciation costs of the Robotaxi fleet will be transferred to vehicle owners, while Robotaxi capacity will be enriched, which will help improve platform operational efficiency and profitability.

Edited by Jeffrey