Yoshitsu Co., Ltd (NASDAQ:TKLF) just reported some strong earnings, and the market reacted accordingly with a healthy uplift in the share price. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Yoshitsu issued 16% more new shares over the last year. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Yoshitsu's historical EPS growth by clicking on this link.

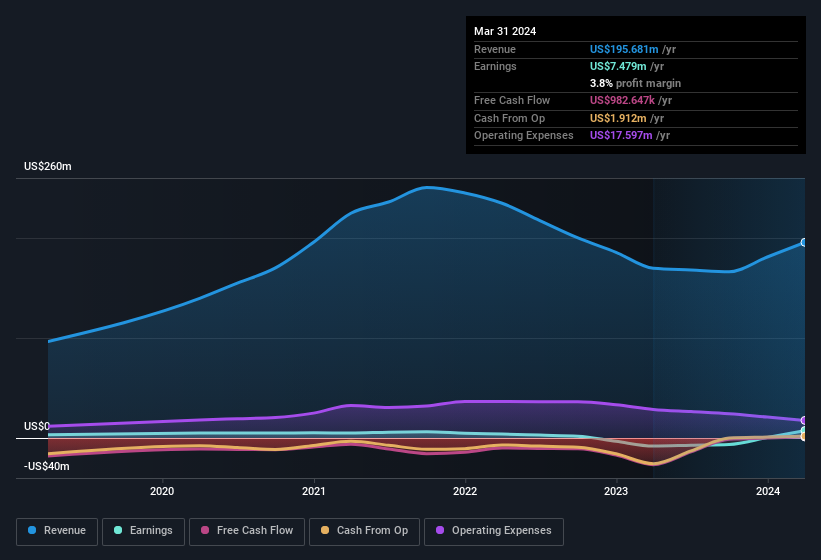

How Is Dilution Impacting Yoshitsu's Earnings Per Share (EPS)?

Unfortunately, we don't have any visibility into its profits three years back, because we lack the data. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is influencing shareholder earnings.

If Yoshitsu's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Yoshitsu.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Yoshitsu's profit was boosted by unusual items worth US$1.1m in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. If Yoshitsu doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Yoshitsu's Profit Performance

To sum it all up, Yoshitsu got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. And furthermore, it went and issued plenty of new shares, ensuring that each shareholder (who did not tip more money in) now owns a smaller proportion of the company. Considering all this we'd argue Yoshitsu's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about Yoshitsu as a business, it's important to be aware of any risks it's facing. For instance, we've identified 5 warning signs for Yoshitsu (3 are a bit concerning) you should be familiar with.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com