On the morning of July 24, the new energy car giant released its Q2 2024 performance.$Tesla (TSLA.US)$Released Q2 2024 performance on July 24.

In Q2 of this year, although Tesla's auto sales did not increase significantly, it was better than market expectations. Coupled with the doubling of income from the sale of carbon emissions credits, Tesla's auto business revenue and gross margin were barely maintained.

In the medium and long term, Tesla's future killers in auto business - FSD and Robotaxi - are expected to have catalysts in the second half of the year; in the short term, Tesla's energy business has begun to hold up part of the profit banner, with growth levels of revenue, gross margin, and energy storage product deployment exceeding expectations.

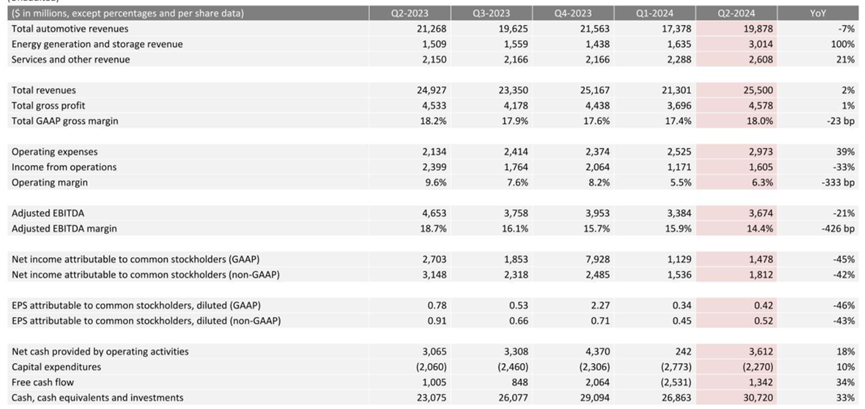

In Q2 2024, Tesla achieved revenue of $25.5 billion, a YoY increase of 2.3%, higher than the market expectation of $24.63 billion; net income was $1.813 billion, a YoY decrease of 42%; gross margin decreased YoY by 0.2 percentage points to 18%.

1. Sales growth is still weak, but the production-sales gap has reversed.

In Q2 of this year, Tesla reduced the frequency of price reductions and promotions in China. Only after Xiaomi SU7 was launched, it reduced the prices of all models by RMB 0.014 million, lowering the starting price of the Model 3 below that of the Xiaomi SU7 Pro (approximately RMB 0.2319 million). Instead, Tesla introduced a limited-time zero down payment or zero interest car purchase plan for the Model 3 and Model Y.

After direct price reductions, insurance subsidies, and service package subsidies, Tesla's new strategy - zero down payment and zero interest - has played a certain promotional role. Although Tesla's sales growth failed to turn positive YoY, the MoM decline finally stopped, better than expected.

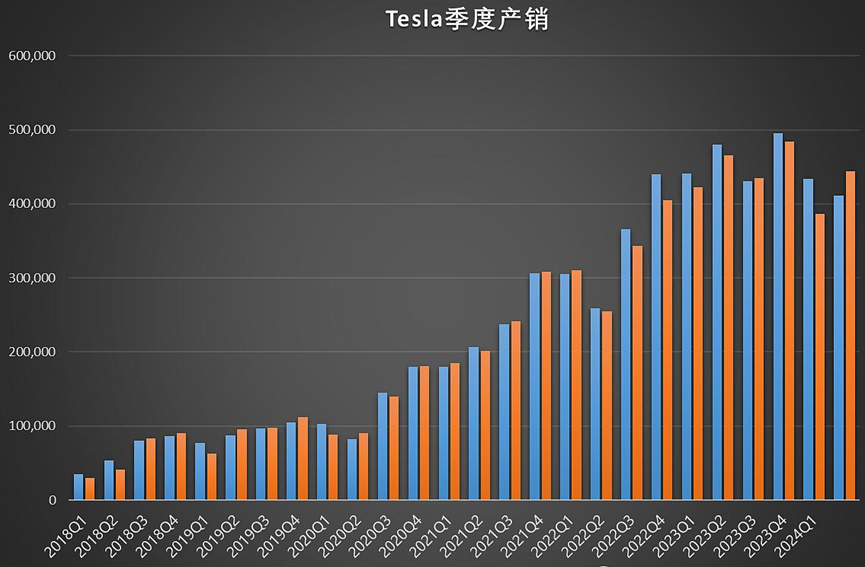

In Q2, Tesla's production volume was 0.411 million vehicles, a YoY decrease of 14.5% and a MoM decrease of 5.2%; deliveries were 0.444 million vehicles, better than the market expectation of 0.4393 million vehicles, a YoY decrease of 4.8%, but a MoM increase of 14.8%.

Since Q1 of last year, Tesla's production volume has been basically higher than its sales volume, leading to a historical high inventory in Q1 of this year (production was 0.047 million vehicles more than sales).

In Q2, Tesla clearly controlled its production pace, and its production volume both YoY and MoM declined, leading to sales exceeding production and inventory no longer accumulating (inventory turnover days decreased from 28 days in Q1 to 18 days in this quarter).

Of course, this is not a long-term solution. Previously, the factor that limited delivery was production capacity rather than demand during Tesla's high sales growth period. Now that it needs to control its production level, it indicates that Tesla has foreseen weak sales growth.

It is worth noting that in the first half of this year, Tesla's global sales were only 0.831 million vehicles, and its market share in China fell below 10% to 6.8%, and its market share in the United States also fell below 50% for the first time in Q2, to 49.7% (59.3% same period last year).

Even according to the flat target of 1.8 million vehicles for the whole year, Tesla needs to reach the quarterly average sales volume of 0.4845 million vehicles in the second half of the year, which is at a historical high and is not easy to achieve.

2. Auto business profit and revenue are barely holding up, and the future depends on the three big aces.

In Q2 of this year, although Tesla's promotion strategy changed, it still did not change the nature of the price reduction, and the embarrassment of the continuous decline in Tesla's single-car revenue did not change.

In Q2, Tesla's single-car revenue was $0.0427 million, a YoY decrease of $0.0033 million and a MoM decrease of $0.0022 million. Fortunately, the income from the sale of carbon emissions credits remained strong, reaching a new high of $0.89 billion in Q2, a YoY doubling, which to some extent compensated for the poor performance of car sales.

Finally, Tesla's auto business revenue reached 19.9 billion yuan, which is basically in line with the market expectation of 19.7 billion yuan; however, the auto gross margin, in the context of price reductions and zero down payment promotions, paid the price for stabilizing sales, which still declined MoM by 1.7 percentage points to 14.6%.

It is worth noting that Musk stated in the conference call that the Robotaxi will hold a formal press conference on October 10th, which will provide a major increment for Tesla's future auto business.

(1) Tesla's FSD is expected to quickly enter China, which will greatly enhance its value.

This time, Musk directly stated that the FSD system will enter multiple countries including China and Europe in version 12.5 (with 5 times the parameter volume of the previous version, greatly improving stability) or version 12.6, and is expected to be approved by China and the European Union by the end of the year.

Previously, Tesla stated that due to insufficient training in regular scenarios, the FSD V12.4 version had poor smoothness under daily driving, resulting in delayed release and unable to be pushed as scheduled in July.

During the Q1 earnings call, Tesla stated that in the first quarter after the release of the V12 supervision version, the growth of FSD-related revenue was considerable (the contribution of automotive gross margin was about 1.7 percentage points), and Tesla FSD was only used in North America and other few regions. If FSD can enter more markets as scheduled, related revenue will bring new growth.

If FSD can enter more markets in the future as planned, related revenue will bring new growth.

(2) Tesla's Robotaxi has great potential.

Another market focus is Tesla's Robotax, which will be launched in October this year.

In the US domestic market, Tesla's self-driving taxi business faces few competitors, mainly Waymo, Cruise and Amazon Zoox.

Tesla is fully capable of taking a larger share of the US domestic market with its advanced self-driving technology, excellent automotive products, outstanding brand effect, and high customer recognition.

3. Highly anticipated robots and AI also develop rapidly.

In addition to the automotive business, Tesla's highly anticipated robots Optimus and AI have also received good news.

Musk said on the earnings call that the Optimus robot is expected to start trial production early next year, just like the Optimus humanoid robot will be officially put into use at the end of this year. Thousands of robots in the initial stage will undertake a certain amount of mass production tasks at Tesla's factory. With the improvement of production efficiency, the second production version of the Optimus robot will also provide sales channels for external customers.

In addition, although Tesla's capital expenditures continued to decline to 2.27 billion yuan in the second quarter, a year-on-year decrease of 0.04 billion yuan and a quarter-on-quarter decrease of 0.5 billion yuan, infrastructure expenditures related to AI computing power increased by about 0.6 billion yuan in the second quarter. It is worth noting that Musk said on the earnings call that the total capital expenditure this year will exceed 10 billion yuan, and the main expenditure will be on AI, because Tesla will increase and go online with a GPU cluster of 50K, as well as expand FSD and improve AI capabilities.

4. Tesla's energy business is booming and has become a short-term major source of incremental revenue.

Tesla's energy business is booming.

(1) Energy storage deployment doubled.

Specifically, in terms of energy storage deployment, Tesla deployed 9.4 GWh of energy storage products in the second quarter, a significant increase of 157% year-on-year and 129% quarter-on-quarter, setting a new historical high (the deployment volume in the first half of the year was close to last year's annual level). In early July, Tesla and Intersect Power announced another cooperation agreement, signing a 15.3 GWh energy storage order, which set a new record of the single energy storage contract of Tesla.

(2) Energy storage production capacity doubled.

In terms of energy storage production capacity, Tesla's Lathrop energy storage plant in California will complete the construction of a new production line this year, achieving a doubling of production capacity from 20GWh to 40GWh; Shanghai's energy storage super factory is also expected to be put into operation in the first quarter of next year, with a production capacity of up to 40GWh. The increase in Tesla's energy storage production capacity fully keeps up with the growth rate of deployment volume and can provide power for the continuous growth of Tesla's energy business in the future.

(3) Energy storage business gross margin greatly increased, and revenue accounted for more than 10%.

In terms of the profitability of the energy storage business, in the second quarter of this year, Tesla's energy business revenue reached 3.01 billion US dollars, a year-on-year increase of 100%, exceeding Tesla's previous guidance of a 75% year-on-year increase.

The proportion of Tesla's energy business in total revenue has risen from 4.8% in 2022 to 12% in the second quarter of 2024, with a gross margin of up to 25%, far exceeding the automobile business's 14.6%. It can be seen that Tesla's energy storage business is quickly turning rapid sales growth into revenue and profit growth.

It should be noted that the delivery date of Tesla's Megapack product has been delayed until mid-2025, and it has begun to enter a period of rapid growth. The only limiting factor for the short-term growth of Tesla's energy storage products is production capacity.

Even with continuous price reduction strategies, Tesla's pure car sales business is unlikely to make progress in the short term. In the future, we can only hope that Tesla will be able to make a beautiful comeback with the rise of FSD, Robotaxi, and energy business.

Edited by Jeffrey