Source: Zhongjin Dim Sum

Authors: Zhang Jundong, Fan Li, Zhang Wenlang

As the market is generally stable and interest rate cuts are expected to begin in September [1], there has been a change in trading style. After data such as CPI and retail sales were released in June, there was a clear correction in large-cap growth stocks dominated by the AI concept, while gold, small-cap stocks, and real estate chain, consumer, manufacturing, and bank-related stocks in the Dow performed relatively well. The main trading line behind it seemed unclear, and the market's judgment on the “soft landing” vs “hard landing” of the US economy after interest rate cuts also showed great differences. Is the market experiencing short-term highs and lows or long-term style changes?

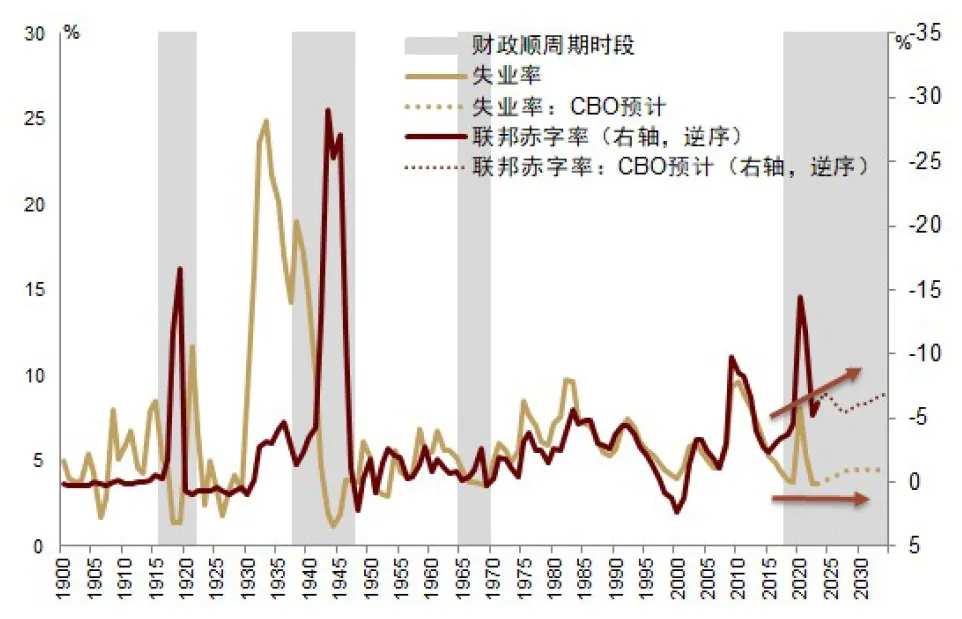

We believe that as expectations of interest rate cuts are basically filled, the space for interest rate cut transactions (“buy expectations”) may be significantly compressed, and “procyclical transactions” after interest rate cuts are immature (see “Interest Rate Cut Transactions” are all the same, and the trading logic after interest rate cuts is different”). Unlike interest rate cut transactions, procyclical trading mainly prices the recovery of terminal demand and the restart of the economic cycle after interest rate cuts. The supporting logic is the resilience of US household demand, big finance, and reindustrialization. More deeply, the total resilience and structural “breakaway from reality” of the US economy. Supported by total economic resilience, interest rate cuts may be relatively limited (that is, “shallow interest rate cuts”), which are more beneficial to the real economy, especially companies with profit support, while boosting valuation is relatively limited.

In terms of pace, “Trump Trade 2.0” is likely to accelerate the arrival of procyclical transactions, given the recent rise in the probability of Trump's victory in the election, as well as the characteristics of stronger fiscal dominance (monetary coordination), industrial return, and potentially weak dollars in Trump's administration philosophy. At the same time, we also suggest that due to the uncertainty of election results, US stocks may enter a period of relatively high volatility in July-October of the previous election year; while interest rates on US stocks and US bonds tend to rise after the election has resolved. On average after the election, value stocks performed better than growth stocks (see “Major Assets of the US Election Year: Finding Certainty in Uncertainty”).

Path: From preventive shallow interest rate cuts to procyclical trading

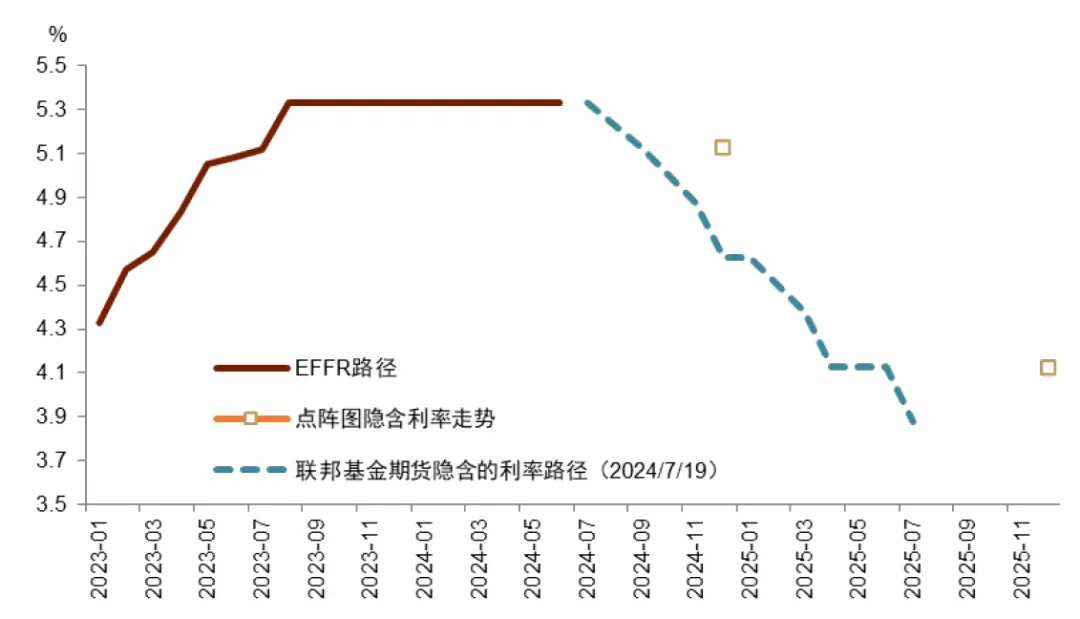

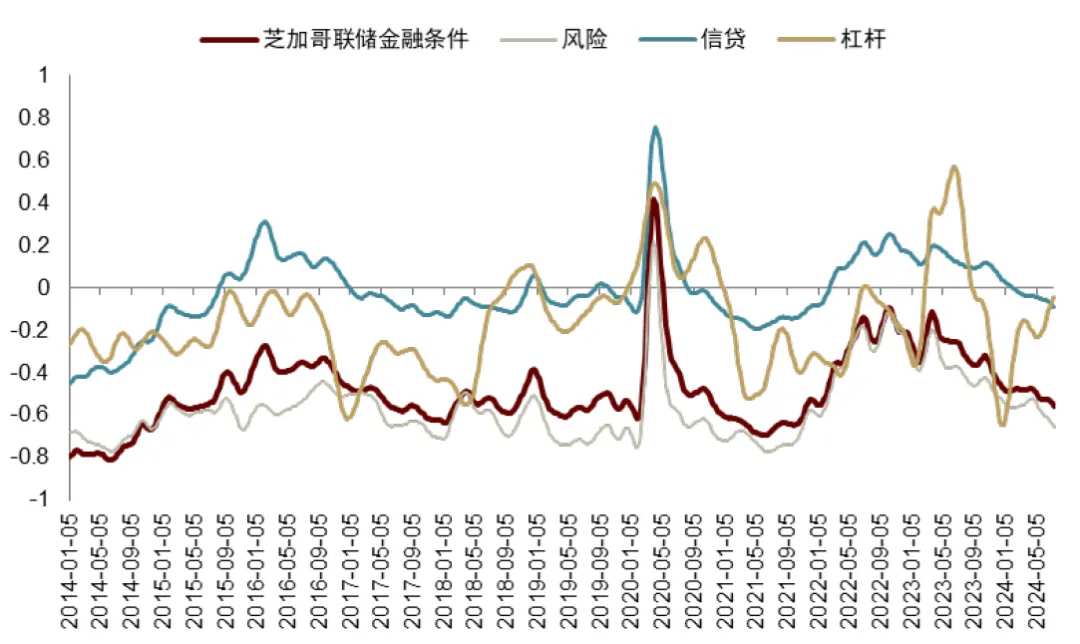

In “The Economic Logic and Asset Main Line of “Shallow Interest Rate Cuts”, we point out that higher short-term interest rates suppress small business operations, cause the labor market to cool down marginally, and may push the Federal Reserve to adopt preventive interest rate cuts. The June CPI fell short of expectations year on year. After turning negative for the first time since 2020, basic market pricing began to cut interest rates in September, and expectations for next year's interest rate cuts have also exceeded the June FOMC bitmap guidelines [2] (Chart 1). Interest rate cut transactions that “buy expectations” mainly benefit more liquidity-driven assets by lowering medium- to long-term interest rates, such as US debt, gold, and small-cap growth. Expectations of recent interest rate cuts have been digested relatively quickly. Financial conditions are close to the level of easing before the current round of interest rate hikes (Chart 2). The space for interest rate cut transactions has been clearly compressed, and at the same time, risks have also increased.

Chart 1: The market expects interest rate cuts to be faster than the bitmap guidance

Chart 2: The Chicago Federal Reserve Financial Conditions Index is close to the low before the rate hike

Looking ahead, since the US economy as a whole is still resilient, the pace of interest rate cuts is more likely to show a “prudent, fine-tuning and gradual” preventive (proactive) character. Active preventative interest rate cuts are often short and shallow, while passive stress (reactive) interest rate cuts are often long and deep. As a result, the upcoming interest rate cut cycle may be difficult to continue to push up market valuations; it is more beneficial to corporate profits and open up space for “procyclical transactions.” Specifically, “procyclical transactions” are more beneficial to small and micro enterprises sensitive to short-term interest rates, manufacturing industries related to US reindustrialization, and real estate chains and consumer sectors related to household resilience. The core logic behind this is the total resilience and structural “devoid of reality” of the US economy, which is reflected in the resilience of the household sector, major fiscal trends, and the long-term restart of the manufacturing industry.

The US manufacturing cycle may be becoming the new engine of the global economic cycle. From the top down, America's fiscal and industrial policies determine the trend of the US manufacturing cycle; from the bottom up, US terminal demand and the resilience of the residential sector determine the elasticity of the manufacturing cycle. Taken together, the return of US industrial capital, or moving away from false reality, is the underlying logic that determines the long cycle of the US manufacturing industry.

Logic: Total resilience and structural “moving from fiction to reality”

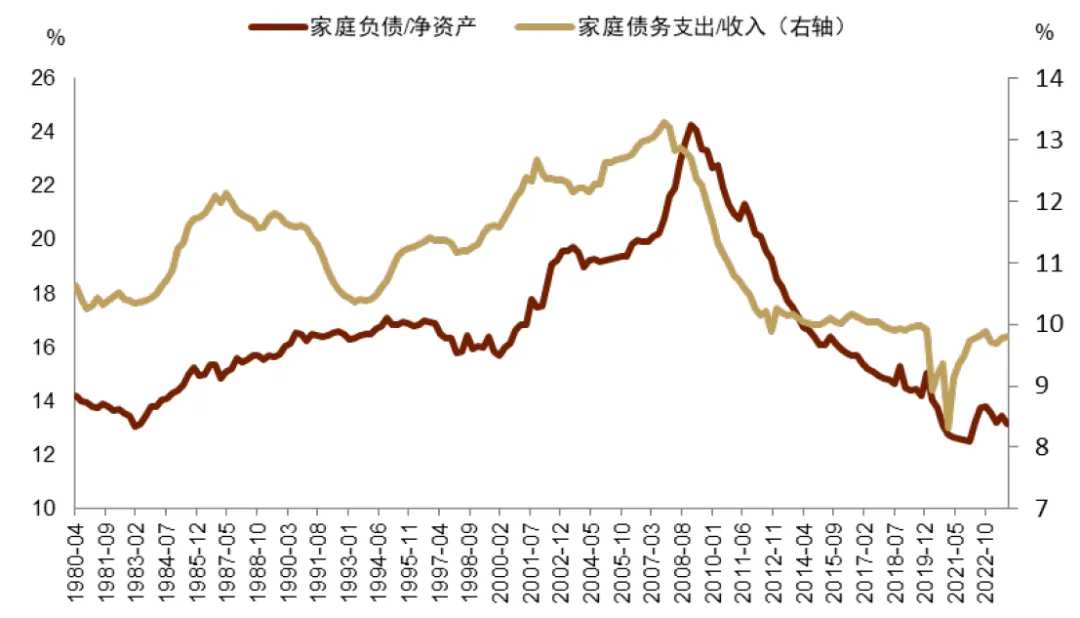

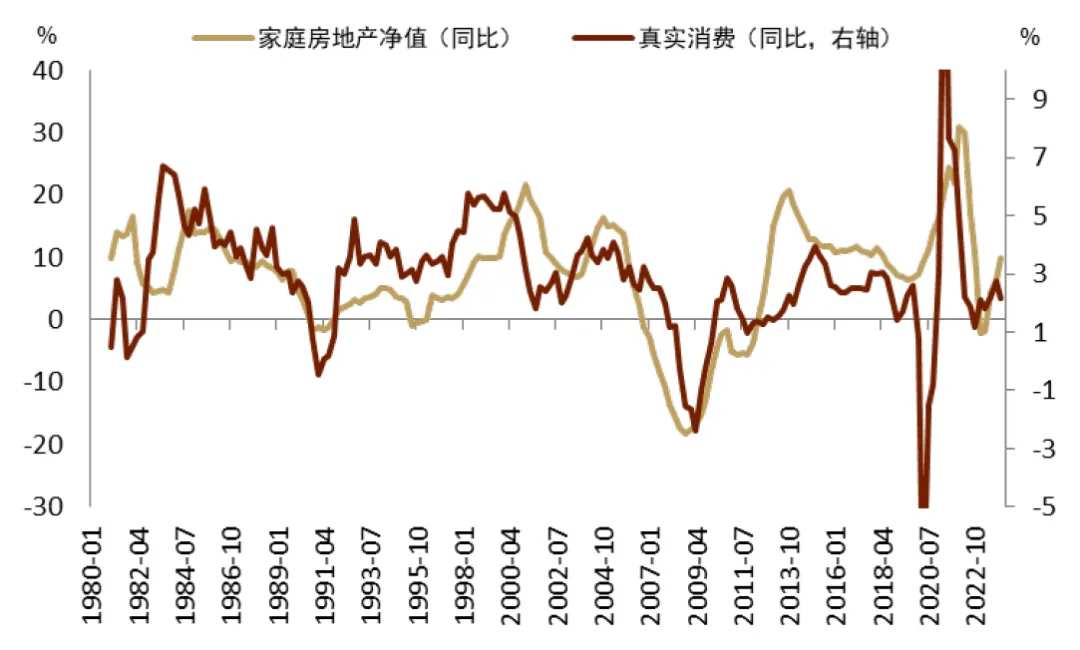

The household sector supports total resilience. In “Second Half of 2024: The Meaning of Assets Under the Economic Rebalance between China and the US”, we pointed out that the US household sector's leverage ratio and debt payment pressure are at historically low levels (Chart 3). However, as the upward financial cycle brings wealth effects and the restart of terminal demand after interest rate cuts drives up income, household consumption of durable goods may strengthen again (Chart 4), fundamentally supporting the US manufacturing industry and moving the economic cycle forward.

Chart 3: Household debt burdens are historically low

Chart 4: Real estate recovery boosts household consumption

The total amount of financial support and structural adjustments. Functional finance is gradually replacing balanced finance to solve problems such as industrial hollowing out and the gap between rich and poor that have gradually accumulated since the 1980s. Procyclical fiscal deficits support aggregate demand (Chart 5), and the fiscal dominant environment may fundamentally alter pricing logic. In “Early Interest Rate Cuts, Confirmation of the End of the Era of Low Interest Rates”, we pointed out that during the period of monetary expansion and “financialization” after 2008, abundant liquidity (“cheap money”) was keen to find growth, and low interest rates helped leading industry companies to form industry monopolies through financing expansion, to the detriment of small and medium-sized enterprises that had no advantage in financing. However, under fiscal leadership, interest rates have moved upward, ending cheap financing, while functional fiscal spending is focusing on rebuilding the domestic US industrial chain, which is equivalent to bypassing the financial market and directly investing financial capital into the production process through subsidies and orders, thus creating an environment conducive to the development of small and medium-sized enterprises and manufacturing industries.

Chart 5: The US is in a rare fiscal procyclical period

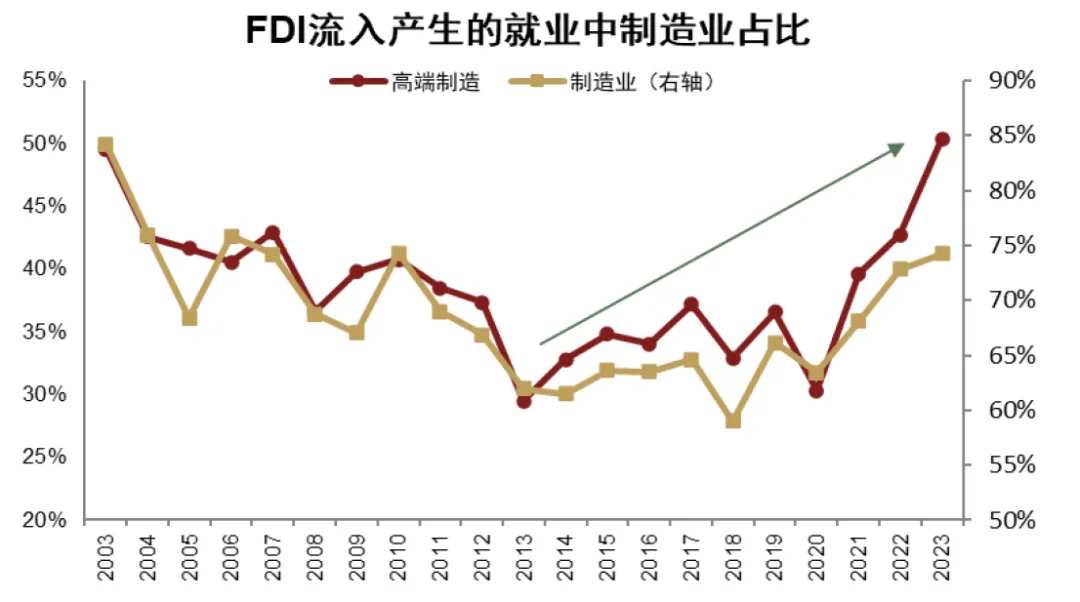

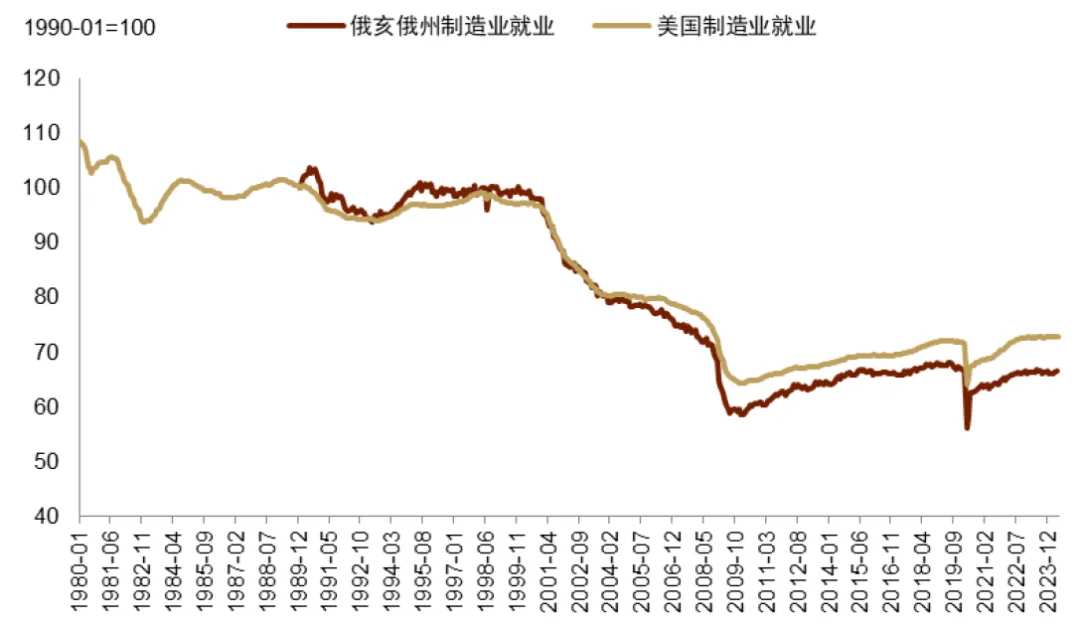

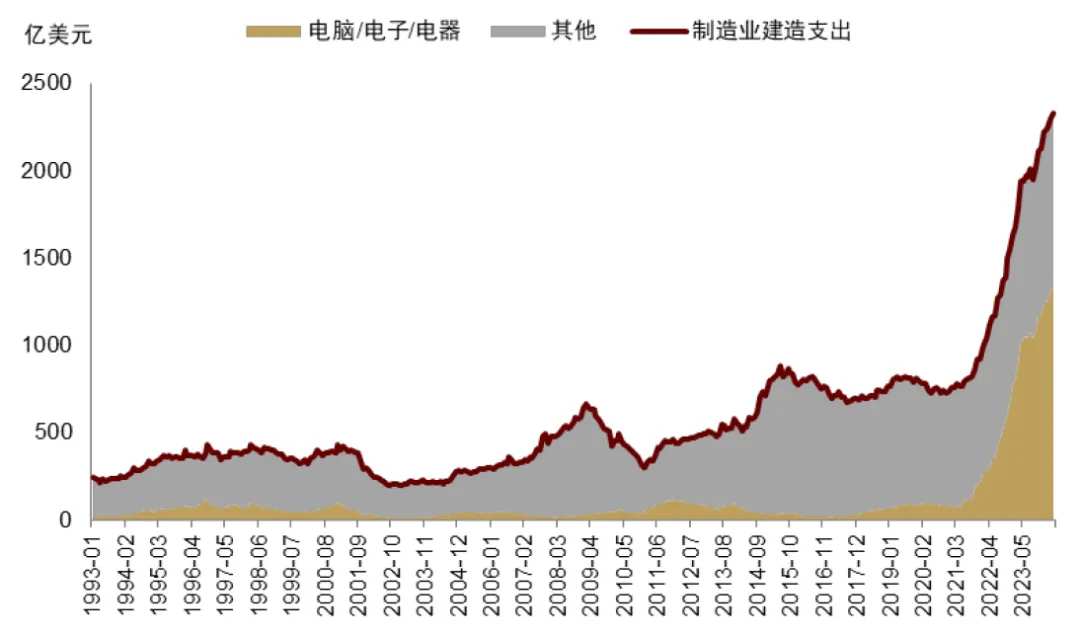

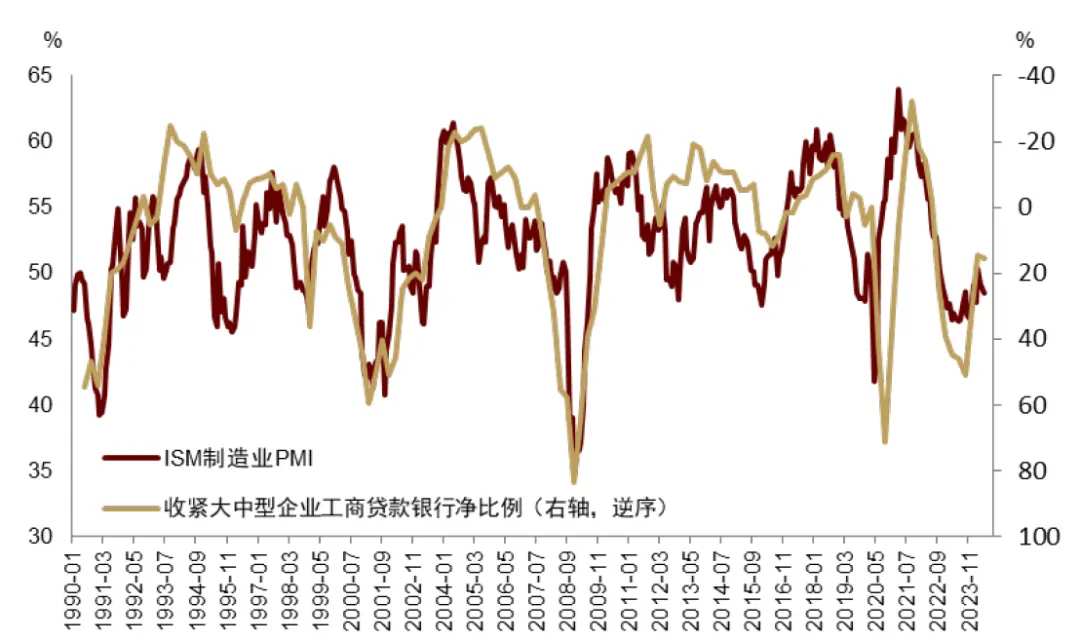

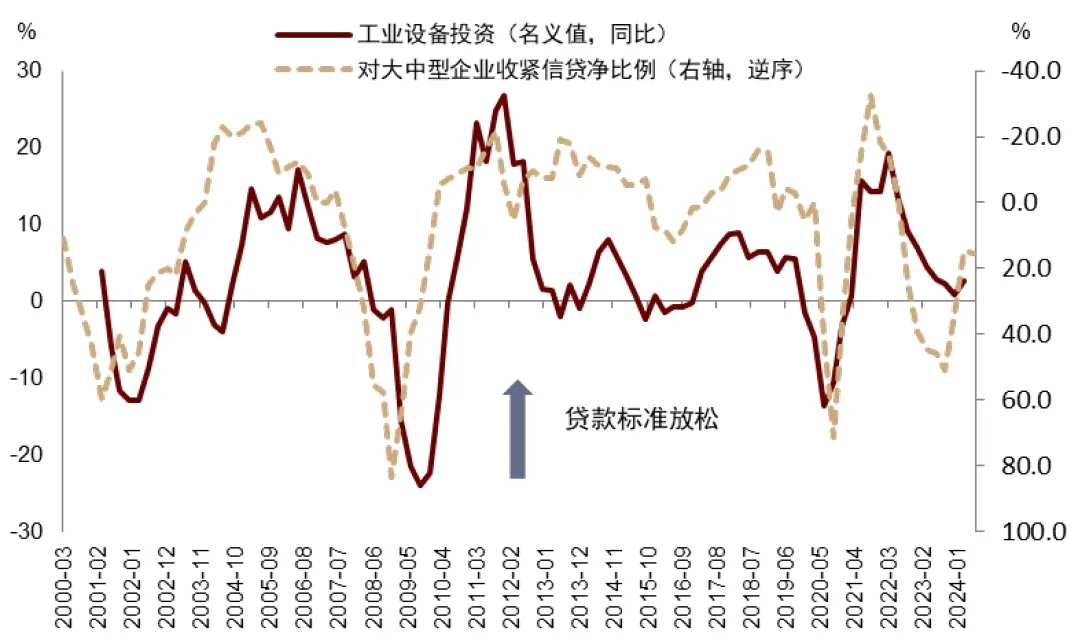

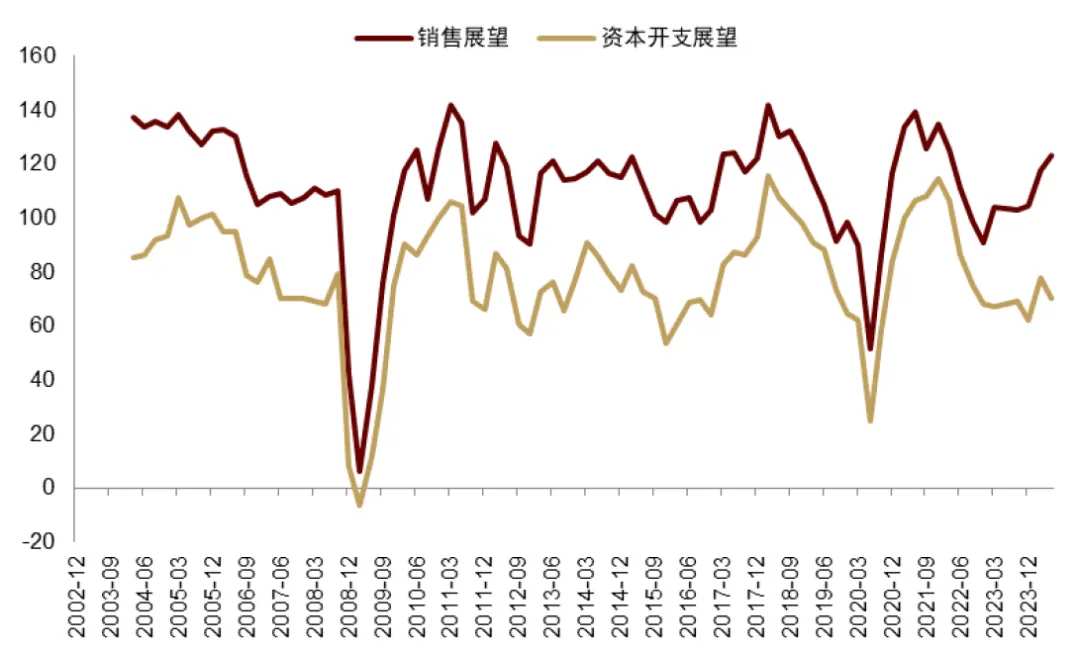

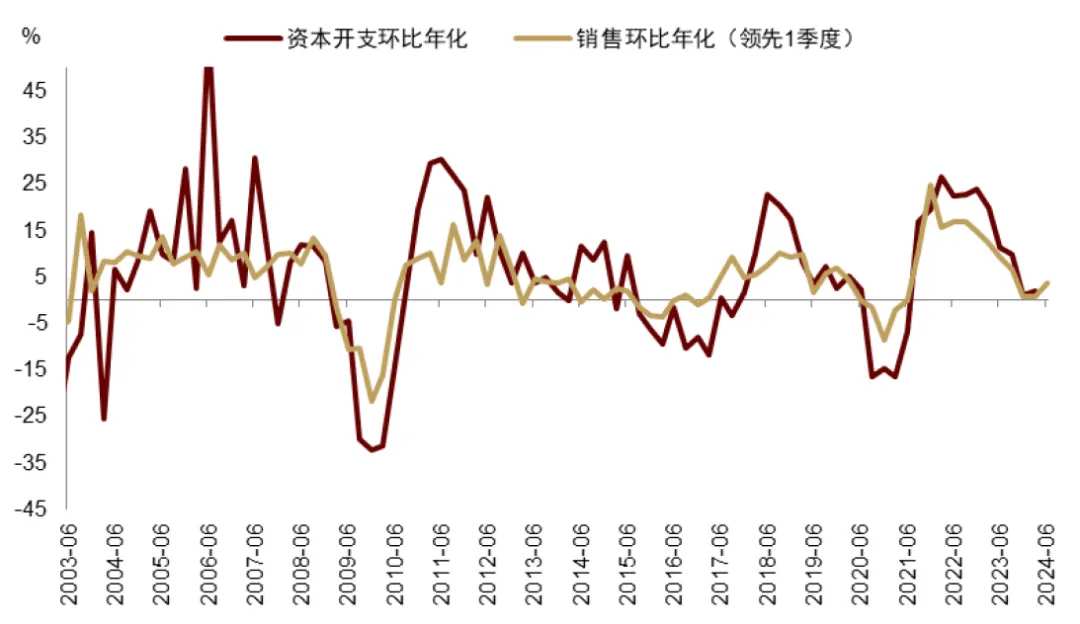

Reindustrialization is accelerating. We pointed out in “Between Breakups in 2024: Consensus and Variables in Overseas Markets” that supporting the return of manufacturing has gradually become a bipartisan consensus in the US. Since the Obama administration, the return of manufacturing has continued to create jobs in the US, and this trend has continued to strengthen during the Trump and Biden administrations (Chart 6). The Trump campaign introduced J.D. Vance from the “Rust Belt” of the Appalachian Mountains as a vice presidential candidate [3]. Ohio, where he served as a senator, was seriously affected by the hollowing out of the manufacturing industry (Chart 7), and Vance's own policy philosophy also focused on protecting the US real economy [4]. Looking at the near future, a further boost in the manufacturing cycle is likely to occur. Since the enactment of the Infrastructure Investment and Employment Act in 2021, manufacturing construction spending has continued to rise rapidly (Chart 8). The commencement of interest rate cuts will help the banking sector continue to relax credit standards, thereby boosting manufacturing PMI and investment in industrial equipment (Charts 9 and 10). The capital expenditure cycle for US companies is bottoming out, and leading indicators show that it is expected to restart. Business Roundtable CEO Survey's capital expenditure expectations for the next six months have bottomed out and rebounded (Chart 11). The recovery in S&P 500 sales growth also indicates that the month-on-month growth rate of capital expenditure of listed companies is expected to begin to rise in the second half of this year (Chart 12).

Chart 6: The share of jobs created by the return of manufacturing has increased since the 2018 trend

Chart 7: Manufacturing employment in Ohio, where J.D. Vance is located, has declined by nearly 40% since the 1990s

Chart 8: Manufacturing construction spending continues to rise rapidly

Chart 9: Loosening credit standards help the manufacturing PMI to recover

Chart 10: Investment in industrial equipment is expected to accelerate as credit standards relax

Chart 11: Business Roundtable CEO Survey Capital Spending Outlook Bottomed Out and Rebounded

Chart 12: S&P 500 capital expenditure is likely to pick up month-on-month

Asset performance: “Trump Trade 2.0” strengthens procyclical transactions and lays out assets “moving from false to reality”

Combining the above structural factors, we believe that the continuity of this round of cyclical trading is likely to be strong. Meanwhile, the recent rise in Trump's probability of winning [5] is strengthening procyclical trading. We pointed out in “Major Assets of the US Election Year: Finding Certainty Amidst Uncertainty” that Trump and Biden agree on the direction of expanding finance and promoting America's reindustrialization. However, compared to Biden, Trump's administration philosophy, on the one hand, has a stronger anti-globalization and “isolationist” philosophy, which is more likely to accelerate the industrial return process. On the other hand, it is more inclined to weaken the independence of the Federal Reserve [6] and strengthen fiscal dominance, thereby boosting interest rates and the center of inflation, leading to a steep US debt curve, compounding its preference for weak dollars, and jointly strengthening its procyclical characteristics.

On the stock market side, procyclical trading after interest rate cuts began is more beneficial to small-cap stocks (short-term interest rate sensitive) and value stocks (mostly procyclical sectors), while in the industry, it is more likely that resources, industrial products, real estate chains, durable goods consumption, banks, etc. will benefit from the real economy's bottoming out and rebound. However, we suggest that due to the uncertainty of election results, US stocks may enter a period of relatively high volatility in the three or four months before the election results are released, suppressing the overall performance of the stock market, and after the election is over, this suppression will quickly release support the upward trend in US stocks. On average after the election, value stocks perform better than growth stocks (see “Major Assets of the US Election Year: Finding Certainty in Uncertainty”).

In terms of commodities, we insist on being optimistic about the long-term allocation value of copper and gold. Although the Trump team does not promote new energy, its recommended re-industrialization goals also rely on large-scale construction of infrastructure such as power grids, which is a strong support for the long-term upward trend in copper prices. Additionally, keep an eye on Elon Reeve Musk's possible role on the Trump team [7]. Trump's policies mostly boosted the center of inflation (see “Major Assets in the US Election Year: Finding Certainty Amidst Uncertainty”), which is expected to boost the anti-inflationary demand for gold (see “The Beginning of Second US Inflation, Resonance Begins”), and his trade protectionism and local priorities may accelerate the global de-dollarization process and increase central banks' demand for gold purchases.

Looking at US bonds, the procyclical deal with Trump may accelerate the rise in interest rates on US bonds and the steeper curve. Short-term interest rates decline with interest rate cuts, while long-term interest rates may remain high, driven by economic resilience and rising inflation centers. We expect the 10-year US Treasury interest rate to rise to 4.5%-4.7% after interest rate cuts, while the interest rate center will remain around 4.5%. In fact, the following three factors will structurally boost long-term interest rates on US debt: In terms of monetary policy, if Trump substantially weakens monetary policy independence by suppressing short-term interest rates, leaving policy interest rates at a “stimulatory” level for a longer period of time, it will increase the risk of overheating demand and inflation, which in turn will increase upward pressure on long-term interest rates. In terms of fiscal policy, increasing spending and cutting taxes at the same time means more supply of US debt. We suggest that TBAC's expected issuance of US bonds in the third quarter increased to 847 billion US dollars, compared to only 243 billion US dollars in the second quarter. Larger US bond issuance may boost interest rates. In terms of trade and foreign policy, “isolationism” may also further push overseas to reduce US debt holdings.

Finally, judging from the underlying driving logic of global assets, the commencement of this round of procyclical trading may mark the establishment of a “break from false to reality” in the field of asset pricing. From the 2008 financial crisis to before the pandemic, China and the US simultaneously “broke from reality to fiction”. On the one hand, the expansion of US monetary policy supported the liquidity of the US dollar, and on the other hand, the upward trend in China's financial cycle promoted the expansion of land finance and supported long-term global asset performance. Currently, China is in the second half of the financial cycle. The US is ending the era of cheap money, and “light interest rate cuts” may be limited in boosting valuations. In this context, the market's focus on policy will also shift from China's credit pulse in the era of cheap money (which favors high growth) and the Fed's deep interest rate cut cycle combined with QE (which favors “buffaloes”) to more entity-oriented policies, such as the fiscal policy of China and the US, industrial policy, and the reindustrialization process of the US and other countries (see “Global “Cash Cows” under the New Macro Paradigm for details).

Under the new pricing logic, we once again emphasize the view in “Global “Cash Cows” under the New Macro Paradigm. In the period of de-financialization, we need to pay more attention to the profit quality and capital return cycle of enterprises, and suggest the allocation value of the three types of assets, namely: physical assets, assets that can generate stable cash flow, and efficient productive assets.

[1] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[2] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[3] https://www.npr.org/2024/07/15/nx-s1-5040236/jd-vance-vice-president-trump-rnc

[4] https://www.axios.com/2024/07/17/vance-trump-economic-philosophy-policy-conservative

[5] https://www.realclearpolling.com/betting-odds/2024/president

[6] https://www.wsj.com/economy/central-banking/trump-allies-federal-reserve-independence-54423c2f

[7] https://www.wsj.com/politics/donald-trump-elon-musk-alliance-d1fe43e3《Inside Donald Trump and Elon Musk's Growing Alliance》

Edit/jadyen