He particularly reminds holders that this fund does not have the possibility of continuous rapid upward movement; the equity position continues to decline to a low level due to new subscription; and it is very cautious to select the appropriate direction on the basis of cost performance ratio to increase the equity ratio.

On July 19th, Cailian News reported (by Zhou Xiaoya) that Yongying Stock Dividend Selection managed by Xu Tuo won the championship of active equity fund returns in the first half of this year with a return of 29.98%, and the latest adjustment trend has been released.

Under the remarkable performance, Yongying Stock Dividend Optimizer continued to absorb gold. At the end of the second quarter of this year, the total number of fund shares was 1.091 billion shares, an increase of 663 million shares or 154.91% over the end of the first quarter. Net purchased shares mainly focused on Class C shares, with an increase of 539 million shares in the second quarter. The fund's size increased to 1.536 billion yuan, an increase of 990 million yuan or 181.17% over the previous quarter.

"It must be declared that this fund is not a racing product." In the face of the influx of funds, Xu Tuo emphasized in the quarterly report that the product is not simply sorted by the dividend yield, nor does it have the attributes of bond funds, but pays more attention to shareholder return represented by dividends.

He also specifically reminds holders that this fund does not have the possibility of continuous rapid upward movement, and investment decisions should not be based solely on recent performance.

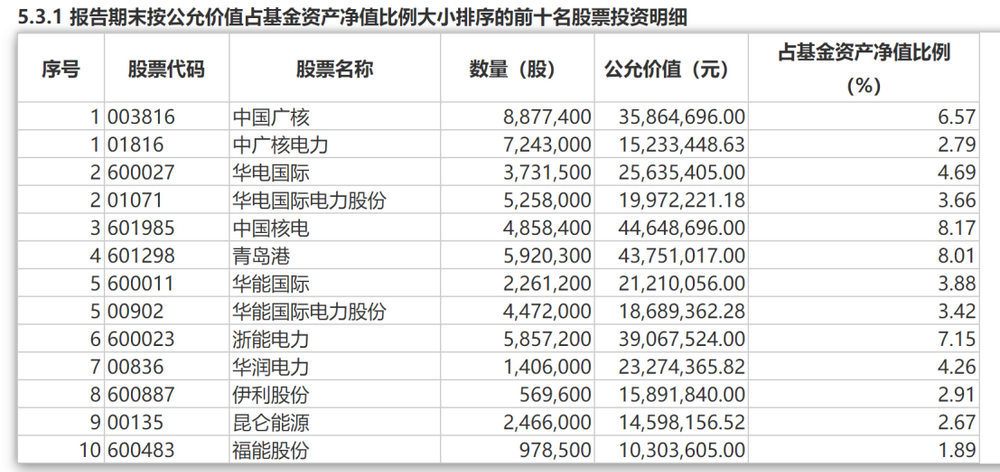

Reducing stock position holdings and adjusting four of the top ten heavy positions.

In the second quarter of this year, Xu Tuo further lowered the stock position of Yongying Stock Dividend Optimization to 59.74%, the Hong Kong stock position was synchronously lowered to 15.39%, and the total position of bank deposits and settlement reserve funds increased to 29.56%. While reducing the stock position, the concentration of holdings has also been lowered. As of the end of the second quarter, the total shareholding ratio of the top ten heavy-weight stocks of the fund was 42.5%.

In this regard, he mentioned in the quarterly report that the fund continued to adhere to a steady and conservative style in the second quarter. As the equity position continued to decline to a low level due to new subscription funds, new funds were invested in a non-hurried and non-high-chasing manner, and new investment focus continued to be on industries and pinpointed stocks to reduce portfolio volatility.

Specifically, four stocks, namely China Mobile, Sinopec, China Telecom, and Xinhua Winshare, China Resources Power, Inner Mongolia Yili Industrial Group, Kunlun Energy, and Fujian Funeng withdrew from the top ten heavy-weight stocks, while China Guangdong Nuclear Power and Hong Kong stock China Guangdong Nuclear Power became the fund's first largest heavy-weight stocks, with an additional holding of 4.8896 million shares and 3.666 million shares from the end of the first quarter, respectively. In addition, Huadian International and Hong Kong stock's Huadian International Power , CGN Power Co., Ltd., and China National Nuclear Power were also increased holdings in the second quarter, while Zhejiang Zheneng Electric Power holdings remained unchanged, and Qingdao Port International was reduced.

China Guangdong Nuclear Power and Hong Kong Stock China Guangdong Nuclear Power are the fund's first largest heavy-weight stocks, and the number of holdings increased by 4.8896 million shares and 3.666 million shares from the end of the first quarter, respectively. In addition, individual stocks such as Huadian International and Hong Kong stock Huadian International Power, CGN Power Co., Ltd., and China National Nuclear Power were also increased in the second quarter, while Zhejiang Zheneng Electric Power holdings remained unchanged, and Qingdao Port International was reduced.

In the quarterly report, it is mentioned that the fund's specific investment direction is mainly distributed in public utilities, telecom operators, publishing companies, ports, oil and gas and other industries, as well as some low-valuation industry leaders with obvious competitive advantages.

It is worth noting that in this quarterly report, many reminders and explanations of product investment logic are mentioned.

For example, Xu Tuo said that the investment goal of Yongying Equity Dividend Preference is to seek returns from certainty, hoping to obtain stable returns on the basis of relatively controllable volatility, and is not pursuing short-term rapid growth. The specific investment focus is mainly on related targets where the business model is simple and clear, the company's quality is better, the barrier is higher, the finances are stable, there is expected dividend, and the valuation is low and the volatility is small.

Due to the tendency of the underlying assets of the fund's main holdings to tend to steady operation, Xu Tuo also mentioned that the investment return of the fund is very testy on the patience of investors, and perhaps trading the time for the space is the best investment way for the fund.

Looking forward to the future, Xu Tuo said that the fund will be very cautious in selecting the appropriate direction to increase the equity ratio based on cost performance ratio. The direction of increased allocation will still choose individual stocks with relatively strong stability, certainty, and sustainability of ROE, and with moderate low-speed growth of business volume along with GDP increase, low valuation and emphasis on shareholder return.

Four stocks, namely China Mobile, Sinopec, China Telecom, and Xinhua Winshare, China Resources Power, Inner Mongolia Yili Industrial Group, Kunlun Energy, and Fujian Funeng withdrew from the top ten heavy-weight stocks

With impressive performance and inflow of funds, Wind data shows that Xutuo's managed public fund scale has increased from 3.657 billion yuan at the end of Q1 this year to 5.566 billion yuan at the end of Q2, including the newly established Yongying Qixin in early June with a scale of 0.435 billion yuan.

The investment situation of the new fund, Yongying Qixin, is also revealed in the quarterly report. As of the end of June, the fund's stock position was only 2.85%, with major holdings in Tangrenshen, Dongrui Stock, Muyuan Foods, China Mobile, Wens Foodstuff Group, and Jinduicheng Molybdenum.

According to Xutuo, the fund will maintain a relatively low risk preference and steady operation in the initial stage of operation. After the steady period, it will gradually shift towards pursuing elasticity. In view of the continuous downturn of the capital market since June, it has maintained a very restrained pace of investment, with most assets invested in short-term income varieties.

Newly added configuration of hog farming sector.

In addition to Yongying Guoxi Youxuan, the remaining Yongying Huitianying One Year, Yongying Changyuan Value, and the aforementioned Yongying Qixin all have stock holdings in hog farming sector individual stocks such as Wens Foodstuff Group and Muyuan Foods in the second quarter of this year.

In his view, the domestic hog farming industry has shown a significant contraction in supply, with a double-digit decline in the sow inventory. However, due to the unexpected decline in pig demand, such as dining decline, physical labor demand decline, and other meat protein substitutes, pig prices gradually recovered in the second quarter, and the increase was considerable.

Looking ahead, he believes that hog farming companies on the supply side do not have the willingness and ability to greatly expand again due to the heavy blow to profitability in the previous round and the tightening of financing in the capital market. The demand side is expected to recover with the economic recovery, so the probability of pig prices maintaining a high mid-cycle level is greater, and high-quality companies may benefit significantly from it.

In addition, Xutuo also mentioned that the two products, Yongying Huitianying One Year and Yongying Changyuan Value, still maintain their allocation to Hong Kong property and real estate leading State-owned enterprises, mainly due to the judgment that the real estate industry is gradually bottoming out and such companies have extremely low valuations, but they are not eager to obtain rapid returns in this sector.

Furthermore, Xutuo pointed out that the cycle of the hog farming industry is obvious and has typical cobweb model characteristics, that is, due to the large number of participants on the supply side and uneven breeding levels, the profit fluctuations of the participants bring about the output fluctuations in the same direction. Therefore, the cyclical nature is more obvious, and the cumulative advantage of high-quality companies gradually increases.