Although the net increase in Netflix users in the second quarter of 8.05 million exceeded expectations, it has shown a gradual downward trend for several consecutive quarters, and both the guidance for third-quarter revenue and the outlook for full-year free cash flow are below market expectations, causing a sharp drop in stock prices after hours. However, the overall bullish situation in the second quarter report, the company said that there is significant growth potential in the India market, and raised the lower limit of the range of full-year revenue growth rate, and Wall Street maintains high expectations.

After-market trading on Thursday, July 18, the streaming media giant, Netflix, announced bullish Q2 earnings for 2024, but its stock price fell nearly 7% during after-hours trading due to lower-than-expected Q3 revenue guidance, slower quarter-over-quarter user growth, and a decline in free cash flow. $Netflix (NFLX.US)$As Netflix's stock price approached its historical high in November 2021, Wall Street had high expectations for this financial report. Netflix subsequently stated that there is still significant growth potential in the Indian market, and after an hour of the release of the financial report, the post-market stock price stopped falling and turned upward.

During Netflix's recent surge in stock price, the company announced that India's market still has a lot of room for growth, and following the release of its financial report, the post-market trading saw a turnaround in stock prices.

In the second quarter, Netflix's revenue and EPS exceeded expectations, and its net user growth more than doubled market expectations, but it also showed a quarterly decline trend.

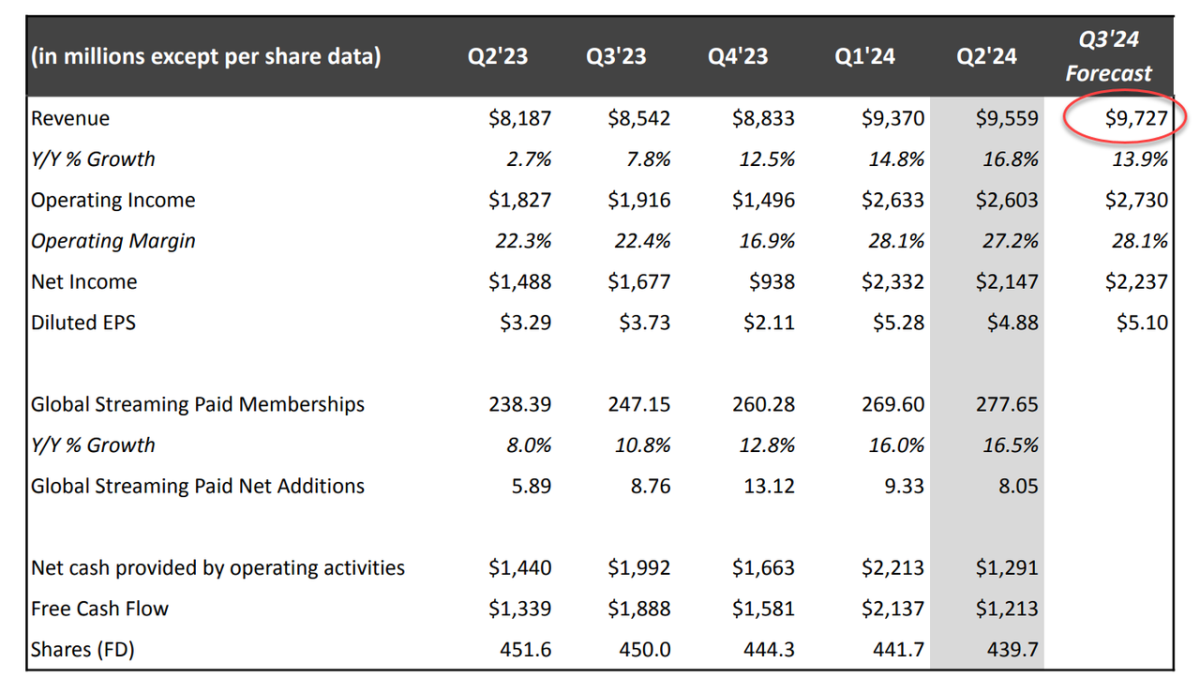

In Q2, Netflix's revenue increased nearly 17% year-on-year to $9.56 billion, higher than the analyst's expected $9.53 billion and higher than the company's official guidance of $9.49 billion. Q2 2023 saw $8.19 billion.

EPS increased 48% year-on-year to $4.88, exceeding the market's expected $4.74 and Netflix's guidance of $4.68. It was $3.29 in the same period last year.

Operating profit increased 42% year-on-year to $2.6 billion, higher than the market's expected $2.43 billion. Operating margin was 27.2%, higher than the same period last year's 22.3%, and slightly lower than the previous quarter's 28%, but in line with expectations.

At the same time, Netflix's net user growth in Q2 was nearly twice as high as the market expected. The total number of global paying users increased by 16.5% year-on-year to approximately 278 million, while analysts expected about 274 million. In the quarter, the net increase in paying streaming media users was 8.05 million, and the market expected an increase of 4.87 million.

Among them, the net increase in paying users in the largest market, the United States and Canada, was 1.45 million, a year-on-year increase of 24%, exceeding the market's expected increase of 1.19 million; the net increase in the Asia-Pacific region was 2.83 million, a doubling growth of 164%, the market's expected increase was 1.25 million; the EMEA region's net increase was 2.24 million, which was a year-on-year decrease of 7.8%, but higher than the expected increase of 1.56 million; the Latin American market increased by 1.53 million, a year-on-year increase of 25%.

Some analysts pointed out that North America and Latin America have taken the lead in the year-on-year increase in net new paying users, but the month-on-month growth has slowed. Although the overall net new paying users exceeded last year's increase of 5.9 million, it showed a quarterly decline. For example, Q4 2023 saw an unexpected increase of 13.12 million users, and Q1 2024 saw an increase of 9.3 million, which was nearly double the expected increase.

Starting from 2025, Netflix will stop reporting the data on new subscription users and ARPU (average revenue per user), which has raised concerns about long-term user growth trends. However, the company stated that this is because it will shift its focus from subscription user growth to focusing on income and operating profit margin as the main financial indicators and measuring customer satisfaction by user engagement (i.e., time spent on the platform).

Netflix raised the lower limit of the year-on-year growth rate range but had a poor outlook for Q3 revenue and full-year free cash flow.

In terms of financial outlook, Netflix expects its full-year revenue in 2024 to increase by 14% to 15% year-on-year, which was previously expected to increase by 13% to 15%, and the lower limit of the revenue increase range was raised. The market still expects revenue to increase by about 15%.

Wall Street also expects Netflix's annual revenue growth rate to remain at an average of 13% in the next three years. This year, Netflix's EPS may grow 53% to $18.41 per share, up from last year's $12.03, and increase by 21% to $22.29 per share by 2025.

At the same time, Netflix expects the company's operating profit margin to be 26% for the full year, and analysts expect it to remain unchanged at the level of 25%. Netflix maintained its full-year free cash flow (FCF) expectation of approximately $6 billion, lower than the analyst's expected $6.59 billion.

It is worth noting that although Netflix expects EPS to be $5.10 per share in Q3, higher than the market's expected $0.474 billion, Q3 revenue is expected to be $9.73 billion, significantly lower than the analyst's expected $9.83 billion.

Financial blog Zerohedge stated that Netflix's free cash flow fell by nearly 50% month-on-month in Q2 and hit the lowest level since 2022. The company also reiterated that its net increase in subscription users in Q3 will be lower than that of the same period last year, the first full quarter after cracking down on shared accounts.

Netflix is actively developing its revenue-generating advertising business and currently offers ad-included packages for $6.99 per month in 12 countries / regions around the world. The company said that the number of subscribers of ad-included subscription packages increased by 34% year-on-year in the second quarter, accounting for more than 45% of all users in the above-mentioned market. But Netflix also admitted that the road to actually providing revenue contribution through advertising is still long:

"We don't expect advertising to be the main driver of revenue growth in 2024 or 2025. The biggest challenge it faces in advertising is to provide more products to advertisers and improve its technology capabilities."

What is your main concern?

According to Analyst Benjamin Swinburne from Morgan Stanley, despite many positives for Netflix already reflected in the stock price, considering that there is still great growth potential in the future, it remains bullish on the stock.

On the one hand, investors appreciate Netflix's entry into sports event content and hosting live events. In May of this year, the company announced that it had won streaming rights to two NFL (National Football League) games on Christmas Day for the next three years.

Netflix's revenue potential for advertising continues to be highly sought after. In May, Netflix revealed that its lowest-priced subscription package with ads had gained 40 million global monthly active users, a significant increase from 15 million users in November last year, an increase of 35 million from the same period last year.

According to sources, since it was first introduced into the service in 2022, advertising revenue has increased by 70%, 70%, and 65% on a quarter-on-quarter basis in the third, fourth, and first quarters of last year, respectively. Goldman Sachs estimated that advertising may generate nearly $3 billion in revenue for Netflix in 2024.

In May, Netflix also said that 40% of all new registered streaming users chose the ad-included package of $6.99 per month and plans to launch an internal advertising technology platform by the end of next year. However, Bank of America believes that advertising will not contribute substantial revenue until next year.

How does Wall Street look at this?

Many analysts have raised their target price for Netflix prior to the second-quarter earnings report. Bank of America raised its target price from $700 to $740, "reflecting the continued development momentum of the underlying business," and is optimistic about "world-class brand, leading global user group, and innovative leading position," It's expected that advertising revenue will "(no fear of intense competition and) increase significantly" in 2025 and 2026.

JPMorgan is also optimistic about Netflix's significant scale advantages in the streaming media field, saying that there are still huge opportunities in the future, such as Netflix's still less than 10% share on TV viewing time in mature markets such as North America, the company's free cash flow generation and strong balance sheet advantages also contrast sharply with competitors that have drastically reduced costs:

"Our analysis of Netflix's user engagement data continues to show that it is unique, especially in terms of international content strength and consumption depth. Strong core execution, anti-sharing of fee-paying accounts, and ad-included packages that help penetrate more price-sensitive groups are helping Netflix achieve its highest net increase in users in history in 2024."

TD Cowen raised its target price to $775 and raised its forecast for this year's subscription user growth, stating that Netflix continues to benefit from the action of cracking down on shared fee-paying accounts. Its survey shows that 23% of consumers surveyed in the second quarter said they use Netflix most often to load video content on television, ranking first, followed by Google's YouTube.

KeyBanc raised its target price to $735 and maintained an "overweight" rating, believing that "recent price increases by competitors in the streaming media market and Netflix's continued low customer churn rate will support the company's price increase again in the coming quarters."

JPMorgan has raised its target price to $75 billion, stating that Netflix's large scale, strong user engagement, and diversified content will make it the default choice for users to consume television, movies and other long-form content, and will make greater progress in the live sports event.

Although Wedbush Securities did not modify its target price, it upgraded its rating to "overweight", believing that the biggest advantage of ad-included packages is limiting user churn, that Netflix continues to strengthen its position as the winner of the "streaming media war":

"Netflix has found the right model through global content creation, balancing costs, and improving profitability. We believe the company will continue to expand its profitability and generate more and more free cash flow.

Netflix has successfully established an almost insurmountable leadership position in the streaming media war, and we expect competitors to continue to struggle when trying to replicate Netflix's business model.

What will be the focus in the future?

However, Citibank maintains a cautious "neutral" rating and a target price of $660. Moody's warns that although 18 months have passed, Netflix's significant ad revenue potential has not yet been confirmed and much effort is still needed to expand the advertising scale.

"In addition to competing with Google's YouTube and Amazon's Prime Video to attract advertising customers, Netflix also competes with social media short videos for user time. Artificial intelligence tools may significantly reduce the entry barriers for producing high-quality, professional videos and pose a competitive risk."

Stock research institution MoffettNathanson raised its target price to $565 while maintaining a "neutral" rating, acknowledging that Netflix has indeed made "significant progress" in cracking down on shared accounts for paid subscriptions. The proportion of users who access the platform through other people's home accounts has dropped from 15% at the beginning of last year when the crackdown began to 9% in the first quarter of this year, but future efforts will be increasingly challenging.

In addition to the trend of adding new subscribers and advertising revenue, the market will also focus on Netflix's plan to open two "Netflix Houses" in Pennsylvania and Texas in 2025, which will provide immersive experiences including "hot IP" products, food, and experiential products related to popular series such as "Bridgerton", "Stranger Things", and "Squid Game".

In addition, some analysts pointed out that Netflix's price increase for the no ad package is to attract more users to use the ad package. Canceling the cheapest no ad package in the UK and Canada may further promote the development of advertising.

Some analysts also believe that Netflix's investments in gaming, live streaming, and sports-related content may bring good revenue growth but will also have an impact on profits. Netflix is vigorously promoting cheaper ad-supported packages, which, together with higher digital marketing expenses, could squeeze profits.

Editor/Somer