During a week of sustained market turbulence, Wall Street ignored political election uncertainties and stood out in the stock market, continuously breaking historical records. Economic data that fell short of expectations actually strengthened investors' optimistic expectations for a Fed rate cut, which boosted the stock market. In Europe, significant fluctuations were experienced in the market as Britain and France's elections took turns. In addition, gold showed a strong performance due to weak U.S. macro data, rising for two consecutive weeks to the highest level since May, while the crypto market encountered significant setbacks.

US stocks: Wall Street continuous breaking records, ignoring political pressure.

US stocks closing review: The 'mini' non-farm payrolls and ISM non-manufacturing PMI fell short of expectations this week. The most anticipated non-farm employment report further enhanced Wall Street's rate cut hopes, and the US stock market continued to hit new highs.

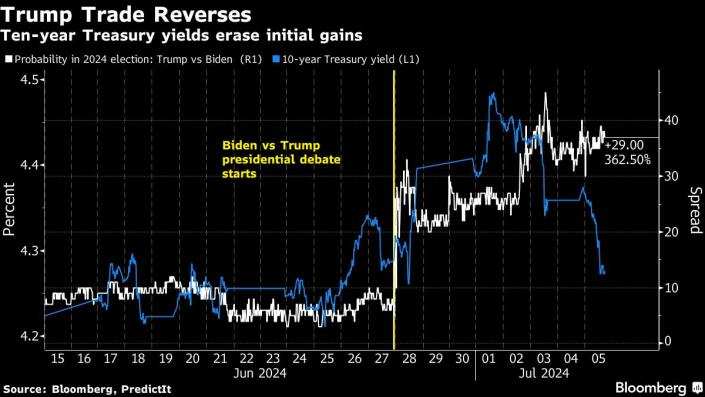

Data showed that the service industry shrunk, and unemployment rates rose, which enhanced people's optimistic feelings about a rate cut. Biden's poor performance on June 27 sparked bets that a Trump return to the White House will relax fiscal policies, causing the 10-year US Treasury bond yield to initially soar, but it subsequently erased gains, and the US dollar also did the same, experiencing its first decline since May.

(Source: Bloomberg)

In terms of the market, the three major indexes rose together this week. The Nasdaq rose by 3.5% over the week; the S&P 500 rose by almost 2%, the fourth week of growth in five weeks; the Dow Jones rose by nearly 0.7%. Excluding the July 4 US Independence Day holiday suspension of trading, the S&P 500 index rose continuously for four days, hitting three historical highs. Since the beginning of this year, the index has set 34 records, with a total increase of nearly 17%. The NASDAQ index also rose for the fourth consecutive week, continuously breaking previous high records.

(Source: Google)

(Source: Google)

This week, investors' resilience was once again demonstrated. Despite the frequent election turmoil, the S&P 500 index continued its trend of rising, rising every trading day for the past 11 weeks, and is still going up.

Although the continuous rise of the stock market is welcomed by the bulls, some people regard the increase in Trump's chances of winning the election as a catalyst, but this has also brought some unusually different backgrounds to the election. Data compiled by Bloomberg shows that the P/E ratio of the S&P 500 index is 26 times, and the current valuation is higher than any election period since at least 1990. Regardless of who wins the November election, the high state of the stock market may become a reason to lower performance expectations.

(Source: Bloomberg)

Dan Suzuki, Deputy Chief Investment Officer of Richard Bernstein Advisors, said: "The high valuation of large US stocks at present means that their performance in the next ten years will be significantly poor, and because they occupy a dominant position, the overall return of the US market may also be quite low." At the same time, when Biden won four years ago, the P/E ratio was also relatively high, which almost did not hinder the market's progress. Since Biden defeated Trump in November 2020, the S&P 500 index has risen by 65%. The market that fluctuated due to Biden's poor performance in the presidential debate, such as the U.S. Treasury bond market, has regained its vitality due to the strengthened expectations for a rate cut due to economic data.

Currently, the upward trend of risk assets continues despite the turbulent background, driven by people's confidence that economic expansion is sufficient to avoid recession, and it is still worth the Fed relaxing monetary policy. Corporate credit and commodity assets also joined the rally this week.

This week, technology giants once again led the way in the stock market. Tesla rose for eight consecutive trading days, with a 27% increase this week, wiping out the previous half-year's decline; Nvidia fell on Friday but rose nearly 2% this week, ending a two-week decline, and its market value of 3.1 trillion US dollars ranks third in U.S. stocks; Meta hit a new high this week with a cumulative increase of 7.08%; Google A hit a new closing high for two consecutive days, with a cumulative increase of 4.64% this week, up for five consecutive weeks. Apple hit a new closing high for four consecutive days this week, with a cumulative increase of 7.46% this week, up for two consecutive weeks; Microsoft also hit four consecutive highs, and its market value lead over Amazon was challenged. Amazon rose by 1.22%, tying its historical high.

Financial stocks are seen as the beneficiaries of Trump's victory, partly because of Trump's agenda of relaxing regulation and allowing financial stocks to rise, but the increase has been limited. Political factors have not yet fully reflected in the market. Although the likelihood of Trump's victory is continuously increasing, Bitcoin still fell sharply. Trump’s increasing support for cryptocurrencies in recent months has become more apparent. Traders attributed Bitcoin's decline to other factors, including the expected sell-off of the bankrupt exchange Mt. Gox.

Meanwhile, this week, the telecommunications sector rose by 3.91%, the technology sector by 3.85%, the optional consumer sector by 3.75%, the daily consumer goods sector by 1.03%, the financial sector by 0.93%, the industrial sector by -0.56%, the public utilities sector by 0.56%, the real estate sector by -0.23%, the raw materials sector by -0.46%, the health care sector by -0.96%, and the energy sector by -1.27%.

Bond market: The yield of the US 10-year benchmark treasury dropped by 11.97 basis points during the week and settled at 4.2745%. The yield of the two-year US treasury bond decreased by 15.20 basis points during the week and settled at 4.6014%.

Interest rate cut: Another round of data support is needed for a rate cut expectation in September. More importantly, the inflation data next week and next month may also affect the decision. Some analysts pointed out that there were contradictions in recent data. On the one hand, the non-farm payrolls data boosted the expectation of a rate cut in September and drove up the US stocks, but the same trend shown in various data is raising concerns about signs of a weakened US economy.

European stocks: French and British elections took turns, causing turbulence in European stock markets.

The headline news this week was the result of the UK general election, with the opposition Labour Party winning an absolute majority in parliament, defeating the Conservative Party, which had been in power for 14 years. Keir Starmer, the leader of the center-left Labor Party, has now become the new British prime minister.

The overwhelming victory of the British Labour Party in the election could pave the way for a rate cut by the Bank of England after the election. From historical experience, this election result may bring some good news to the British stock and bond markets. Some analysts expect that the victory of the Labor Party will boost the British market, especially in the housing construction sector over time.

Fund managers said they expected the Labor Party under the leadership of Keir Starmer to adopt more calm and moderate policies, bringing an end to the years of turmoil marked by the British bond crisis, Brexit and the Scottish independence referendum.

Stoxx 600 index rose 1.01% this week; the German DAX 30 index rose 1.32% this week; the French CAC 40 index rose 2.62% this week; the Italian FTSE MIB index rose 2.51% this week; the UK FTSE 100 index rose 0.49% this week; and the Spanish IBEX 35 index rose 0.73% this week.

One of the "Eleven Arhats" in European stocks, ASML Holdings, rose about 3% this week, approaching the 1,000-euro mark. Novo-Nordisk A/S fell 3.14% this week, and although Harvard University released a research report unfavorable to its weight-loss drug, the company's stock price continued to rise for the second consecutive day. Danish pharmaceutical company Zealand rose for the second consecutive day to a new closing high this week, with a cumulative increase of 6.6% this week and more than 46% in eleven days.

However, as more widespread risk aversion sets in, European stock markets have given back their gains. James Athey, portfolio manager at Marlborough, said, "Given the decent rebound in the market after the first round of voting, I guess traders are closing out positions ahead of the French election."

Although the French polls suggest that the parliamentary results may be inconclusive, Ipsos poll results show that Le Pen is expected to win 175-205 seats in Sunday's parliamentary election, far short of the 289 needed for an absolute majority, and the yield spread between French and German 10-year treasury bonds has narrowed to 65 basis points.

Asia-Pacific stocks: Japanese stocks ended five consecutive gains, while Chinese stocks fell.

Japanese stocks: the Nikkei 225 index rose by 3.36% this week, with most constituent stocks falling. In terms of heavyweight stocks, RECRUIT and SoftBank both set new historical highs this week.

A-shares: This week, the Shanghai Composite Index fell by 0.59%, the Shenzhen Component Index fell by 1.73%, and the Chinext Price Index fell by 1.65%. The Shanghai Composite Index has been down for seven consecutive weeks. The last time it fell for seven consecutive weeks was from May to July 2018. After falling from 3,219 points to 2,691 points, the index rebounded but did not break away from the downward trend. On the news front, the 2024 World Artificial Intelligence Conference was held in Shanghai, and the market's enthusiasm for AI has returned. In addition, the third plenary session showed the market's optimism for tax reform, fiscal and tax digitization, and Hainan Free Trade.

Forex: The US dollar continued to fall.

The DXY index fell by 0.24% to 104.875 points, down 0.94% This week and ending a four-week streak. The Bloomberg US Dollar Index fell by 0.18% to 1260.27 points, down 0.73% this week.

This week, the euro rose 1.18% against the US dollar, the British pound rose 1.35% against the US dollar, and the US dollar fell 0.34% against the Swiss franc; among commodity currencies, the Australian dollar rose 1.19% against the US dollar and the New Zealand dollar rose 0.88% against the US dollar. The USD/CAD fell by 0.25%.

Offshore yuan rose as much as 150 points or 0.2% in pre-market trading and reached 7.28 yuan, but then erased gains and returned to the level of 7.29 yuan. It is still not far from the eight-month low.

The USD/JPY fell by 0.33% to 160.74, breaking through the 161 mark. When the non-farm payroll report was released, it fell to a daily low of 160.35. It fell by 0.09% this week and showed an overall rise and fall trend.

Cryptocurrency: Flash crash.

Most mainstream cryptocurrencies fell. The largest market cap leader, Bitcoin, fell by 5.30% to $56,655.00, down 6.08% this week. The second largest, Ethereum, fell by 4.76% to $2,983.00, down 12.14% this week.

#Gold review# Good news from non-farm data supports overall metal gains. Gold has risen for two consecutive weeks to its highest level since May, with silver up more than 7.63% this week and copper up more than 3.59%.

#Gold Review# Good news from non-farm data supports overall metal gains. Gold has risen for two consecutive weeks to its highest level since May, with silver up more than 7.63% this week and copper up more than 3.59%.

(Source:Wall Street News)

Following the announcement of non-farm data, the gold price continues to rise, with a cumulative increase of 2.87% this week, an increase for two consecutive weeks, the largest weekly increase in nearly 13 weeks.

KCM Trade's Chief Market Analyst Tim Waterer said, "Gold has had a fruitful week, with precious metals benefiting from some weak macroeconomic data in the USA."

Oil prices: Strong demand outlook leads to four weeks of consecutive gains.

#CrudeOilClosingReview# Both oil prices have risen for four consecutive weeks. US oil has accumulated a 2.1% increase, while Brent oil has risen slightly.

Analysts predict that as summer fuel demand picks up, oil demand will be even tighter in the third quarter. The latest inventory data released by the US EIA further validates this prediction.

UBS predicts that global oil demand will increase by 1.5 million barrels/day this year, higher than the long-term growth rate of 1.2 million barrels/day. As the OPEC+ production cut agreement continues until September, inventory will further decline in the coming weeks, and Brent crude oil prices may reach $90 per barrel in the third quarter.

In addition, JPMorgan also predicts that Brent crude oil prices will reach $90 per barrel in August or September.

(Source:Wall Street News)