After the release of non-agricultural data for the week of July 1-5, US stocks and US debt rose, and the US dollar was under pressure. US debt rebounded sharply after realising the “data detail” of 0.11 million in the first two months of non-agricultural production data, and the yield curve became steeper.

Investors have optimistic expectations for the Fed to cut interest rates. According to the CME Fed's observation tool, the possibility of cutting interest rates by 25 basis points in September increased from 66.5% to 71.1%. The possibility of cutting interest rates for the first time in November also increased, while the possibility of cutting interest rates for the second time in December rose to 46.5%. Investors fully expect the Fed to cut interest rates twice before the end of the year.

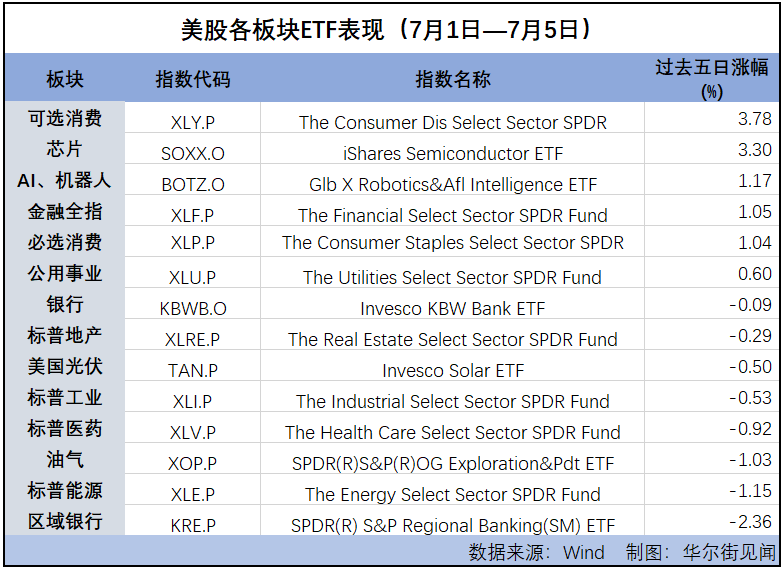

The three broad-based indices of US stocks rose this week, and the S&P market, NASDAQ, and NASDAQ all hit new closing highs. The price-earnings ratio of the Philadelphia Semiconductor Index rose to 55.6, and the valuation level increased further. At this stage, the S&P 500 Schiller price-earnings ratio has risen rapidly to 36.25, which is significantly higher than the historical average of 17.13 and the median of 15.98, which is more than double the historical average and median. US stocks are overvalued, and the US stock market will still be prone to shocks for some time to come.

As the second round of elections to the French National Assembly is approaching, uncertainties and changes in French economic policy can easily test the market. Furthermore, this week's election results for the lower house of the British Parliament also had a certain impact on the European market on Friday. Considering the weak European economy and European policy uncertainty, the valuation advantage of the European market is not obvious at this stage.

The Nikkei 225 index continued to rebound this week. At the same time, however, the issue of pressure on the yen exchange rate has not been resolved, and Japan's monetary policy is being further tightened. Since the timing of the Fed's interest rate cut still needs further confirmation, overseas emerging market indices such as Mexico's MXX, Brazil's IBOVESPA, India's SENSEX30, Indonesia Composite Index, and MSC Vietnam, which are expected to increase significantly in the previous period, will still have to wait for a more clear signal from the Federal Reserve to cut interest rates. Keep an eye on Powell's important speech and US inflation data next week.

This week, the euro rose 1.29% against the US dollar, and the pound rose 1.46% against the US dollar. The offshore renminbi rose as high as 150 points or 0.2% against the US dollar before the US stock market. At one point, it rose above 7.28 yuan. US stocks basically erased gains and returned to the 7.29 yuan line, and are still not far from an eight-month low. The dollar fell below the 161 mark against the yen.

On the commodities side, the US employment report raised expectations of interest rate cuts and reduced the opportunity cost of holding interest-free gold assets. Pressure on the US dollar supported the rise in precious metals prices, and industrial basic metals in London generally rose. International crude oil fell sharply, but oil prices continued to rise for the fourth week because the decline in crude oil inventories exceeded expectations, indicating that oil demand would rise.