Source: Jinduan. Author: Lin Yao Shi. Twelve years ago, the world's most powerful orthopedic giant was born, and since then the entire industry has been mired in endless internal rectification. In April 2011, the world's largest orthopedic company, orthopedics company announced a record-breaking $21.3 billion acquisition of another orthopedic giant Synthes. At that time, Johnson & Johnson, with its previous acquisition of DePuy, became the global leader in the orthopedic business market share, but only had a gap in trauma products, occupying only about 5% of the market share. Swiss medical device company Synthes, although its revenue is less than that of Johnson & Johnson, is the strongest competitor in the trauma product industry, with a 49% market share. The historical largest merger and acquisition transaction enabled Johnson & Johnson Orthopedics to successfully acquire Synthes and become the dominant orthopedic giant in the market with no shortcomings in the joint, spine, and trauma submarkets. Other orthopedic companies were only stuck in the internal rectification in front of Johnson & Johnson Orthopedics' absolute market share. However, the orthopedic market story did not end here.

Source: Jin Duan. Author: Lin Yao Shi. In April 2011, the world's largest orthopedic company.

Twelve years ago, the world's most powerful orthopedic giant was born, and since then the entire industry has been mired in endless internal rectification.

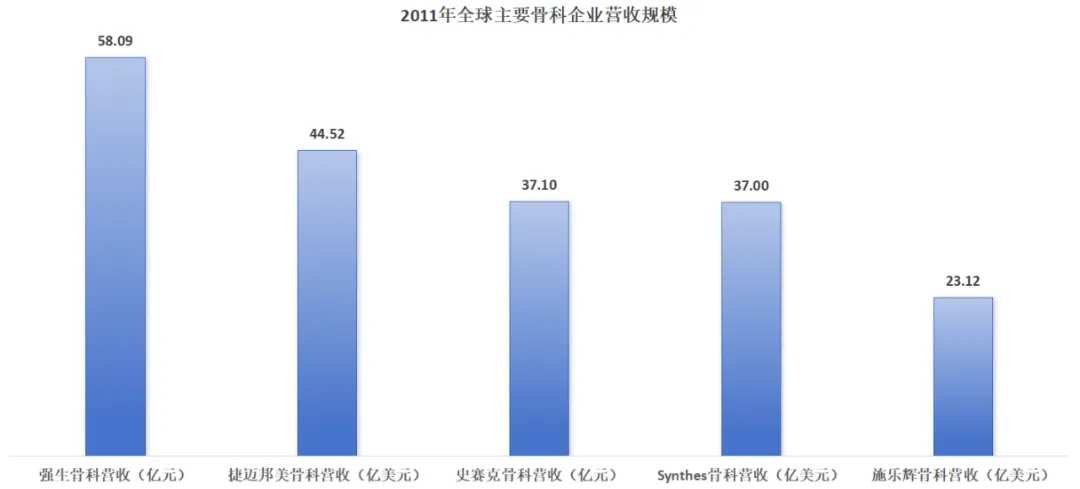

In April 2011, the world's largest orthopedic company$Johnson & Johnson (JNJ.US)$Orthopedics announced a record-breaking $21.3 billion acquisition of another orthopedic giant Synthes, the highest bid ever made by Johnson & Johnson.

At that time, Johnson & Johnson, with its previous acquisition of DePuy, became the global leader in the orthopedic business market share, but only had a gap in trauma products, occupying only about 5% of the market share. Swiss medical device company Synthes, although its revenue is less than that of Johnson & Johnson, is the strongest competitor in the trauma product industry, with a 49% market share.

Through this historical largest merger and acquisition transaction, Johnson & Johnson Orthopedics successfully acquired Synthes and became the dominant orthopedic giant in the market with no shortcomings in the joint, spine, and trauma submarkets.

However, the orthopedic market story did not end here.$Stryker Corp (SYK.US)$This also broke Johnson & Johnson Orthopedics' dream of ruling the empire.

01 The answer is beyond the textbook.

When I was a child, the teacher taught everyone that we must study hard, and the answers to the exam are all in the textbook. However, there are no textbooks in life, and the answers to many things are often beyond people's imagination.

Orthopedics is a race track with extremely high user stickiness. Doctors, for safety reasons, often prefer to use their familiar implants, and changing to new products is not an easy task. Under this logic, the advantage of Johnson & Johnson Orthopedics' acquisition of Synthes was further amplified, and the company had obvious scale advantages in the joint, spine, and trauma submarkets. Johnson & Johnson Orthopedics' products have become doctors' safest choice. In order to grab a piece of meat from Johnson & Johnson Orthopedics, various orthopedic companies must either choose to reduce prices or innovate products, only in this way can they gain first-line opportunities. The industry's absolute leader Johnson & Johnson Orthopedics can continue to enhance its competitiveness by taking advantage of its financial strength and continuously acquiring excellent symbols.

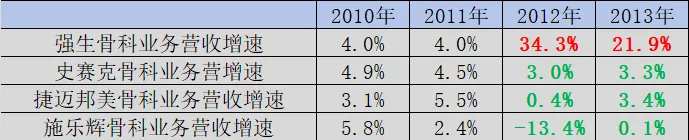

This is a competition pattern that makes all orthopedic companies despair, with Johnson & Johnson Orthopedics dominating the world and other orthopedic companies having to fend for themselves. From the perspective of data observation, after Johnson & Johnson Orthopedics completed the acquisition of Synthes, the growth rate of Stryker, J&JMD, and Zimmer's orthopedic business has shown a significant slowdown, and Xerox, which has weaker market competitiveness, has even experienced a double-digit decline in revenue.

Image: Revenue growth rate of Top Head Orthopedic Enterprises from 2010 to 2013, Source: Jin Duan Research Institute

This reshapes the competition pattern of the entire orthopedic track and breaks Johnson & Johnson Orthopedics' dream of ruling the empire.

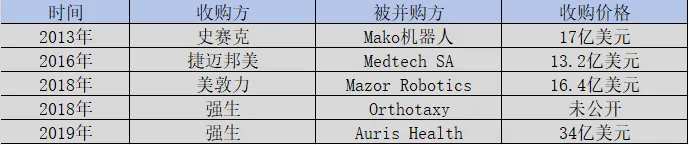

In the most difficult year of 2013, Stryker's management boldly and decisively acquired MAKO, the largest orthopedic surgery robot company at that time, despite investor opposition, for a price of $1.7 billion. After the news was announced, a group of investors collectively expressed pessimism about Stryker's stock price, which fell more than 5% at the time.

The reason why investors did not look favorably on Stryker's acquisition was partly because Stryker's offer was a 86% premium to MAKO's closing price at the time; on the other hand, it was because then U.S. President Obama launched the Affordable Care Act, which made it harder to sell high-end medical equipment, and high-priced surgical robots fell into this category. Investors believed that Stryker should still focus on the implant raceway.

During the initial merger, the MAKO surgical robot did not bring significant growth to Stryker, but Stryker did not give up and continued to integrate resources from both sides.

In 2015, Stryker launched the third-generation MAKO system, an upgraded version of the MAKO system that is tied to implants provided by Stryker and performs surgeries on the MAKO platform.

In 2016, Stryker combined its total knee arthroplasty system with the MAKO system, launching the first-generation total knee arthroplasty platform, MAKO TKA, and gradually extending joint replacement surgery to shoulder, elbow, ankle, wrist, and finger joints.

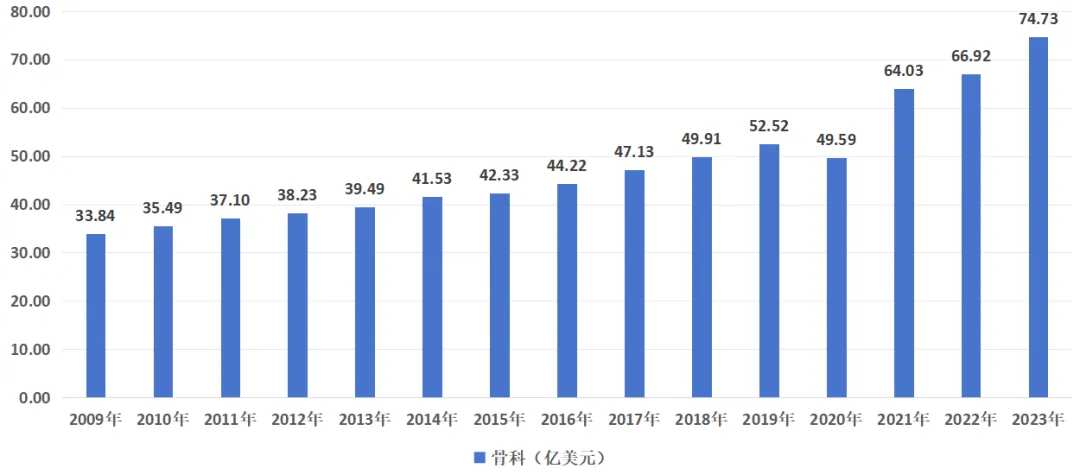

With the deep integration with the MAKO surgical robot, Stryker successfully broke free from Johnson & Johnson's size suppression and successfully transformed into the fastest-growing orthopedic giant in the past decade, with revenue soaring from $3.71 billion in 2011 to $7.473 billion in 2023.

Looking ahead, Stryker broke through the internal competition and surpassed Medtronic to become the second largest orthopedic company in the world by successfully combining with the MAKO surgical robot; while Johnson & Johnson's orthopedics business was trapped in its own size trap and did not grow at all in the past decade.

02 Breaking through the dimensional wall of mergers and acquisitions

Stryker's acquisition of the MAKO surgical robot is not a blindly logical acquisition, but a dying insight into the development logic of the industry.

As an upstream industry chain of orthopedic surgery, surgical robots should be an important part of the orthopedic industry. The Da Vinci robot in traditional surgery has already proved that surgical robots will be the future development direction of surgery. However, in the field of orthopedics, giants still focus on internal competition for scale.

With the early industrial prediction, Stryker successfully entered the no-man's-land of orthopedic surgical robots, quickly proving the safety of surgical robots to doctors by conducting a large number of clinical trials, and further integrating resources to migrate implants to surgical robot platforms. Thanks to the obvious first-mover advantage, Stryker quickly captured the hearts of many doctors. In a 2016 survey, Stryker's hip/knee joint robotic surgery had a market share of over 90%.

Breaking free from internal competition, Stryker not only avoided traditional internal competition, but also successfully developed the blue ocean market of orthopedic surgical robots, further deepening the brand advantage of Stryker's implants in the hearts of doctors. At the same time, MAKO also successfully sold 1,300 surgical robots with Stryker's marketing capabilities, which created a continuous revenue stream for Stryker. Almost one-third of knee joint surgeries worldwide are performed by robots, and Stryker is undoubtedly the biggest winner embracing the future.

Reviewing the key to Stryker's success, it did not indulge in traditional internal competition, but instead considered from the perspective of clinical unmet needs. Surgical robots can provide significantly better surgical results: better balance of knee joints and less soft tissue damage.

Stryker's layout is not a simple industry chain, but the future of orthopedic surgery.

As Stryker gradually validated the correctness of its acquisition of MAKO, other orthopedic giants began to make up for the lost time. The first to notice this trend was the then second-largest orthopedic company, Medtronic. In 2016, it acquired the Medtech company, which had Rosa Brain and Rosa Spine robot-assisted surgical platforms; two years later,$Medtronic (MDT.US)$With Johnson & Johnson joining the acquisition team, orthopedic companies and surgical robots remain an inevitable trend in the industry.

Although these acquisitions have weakened Stryker Corp's advantage in orthopedic surgical robots, its absolute leading position in the global orthopedic surgical robot track has already been achieved through continuous resource integration over the years. At present, Stryker Corp's first-mover advantage in the surgical robot track is still continuing to release, which is also the reason why US stock investors have been bullish on it in recent years.

03. Changes in the orthopedic track over the past decade

The past decade can be regarded as a transition period between the old and new industrial logic in the orthopedic track.

Johnson & Johnson's acquisition of Synthes in 2011 was the peak of the old logic in the orthopedic track, and it was an absolute leader in the old logic. Stryker Corp's acquisition of the surgical robot MAKO in 2013 was the beginning of the new logic in the orthopedic track. The new logic chose new platforms like surgical robots, not only embracing the future, but also reshaping the entire competitive landscape of the track.

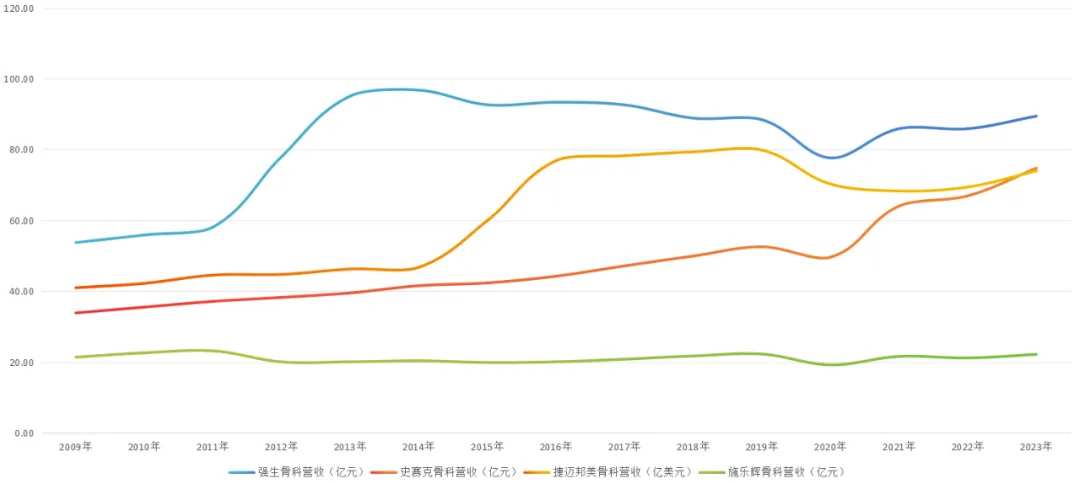

Looking back at the revenue trends of global orthopedic giants from 2009 to 2023, investors can clearly see that Stryker Corp's performance has continued to release under the blessing of MAKO robots, while Johnson & Johnson's orthopedic revenue peaked at $9.675 billion after acquiring Synthes, but the revenue trend has turned downward over the past decade, and the revenue scale in 2023 is only $8.942 billion, lower than the revenue level in 2013.

From a macro perspective of the entire orthopedic track, Stryker Corp and Johnson & Johnson's orthopedics belong to two extremes. The former embraces the future, while the latter relies on the past. This world will only continue to develop forward, and Stryker Corp, which embraces the future, defeats Johnson & Johnson's orthopedics, which relies on the past, and presents a wonderful drama of winning against all odds.

The invincible giant Johnson & Johnson's orthopedics has fallen into a vortex, which is enough to illustrate that the value of the pharmaceutical industry is not in the past, but in the future. Being fixated on the past will only cause internal friction, and looking to the future can achieve breakthroughs. This principle applies to international giants like Stryker Corp, as well as domestic pharmaceutical companies that are still in their infancy, and hope lies in the clinical blank space.

The opportunity for the pharmaceutical industry to explode must be hidden in the unmet clinical needs, which are the directions that pharmaceutical companies need to continue to cultivate.

Editor/Somer