The Nasdaq Composite Index entered a bull market in December 2022. In about 18 months, this technology-driven index has risen 76% driven by the surge in interest in artificial intelligence (AI). However, according to historical patterns, these gains may just be the beginning. #AI boom# #2024 macro outlook# #2024 investment strategy# #technology#

Since 1990, the average return rate of Nasdaq during a bull market is 215%, lasting for an average of about 40 months. If the current bull market follows the historical average level, then the Nasdaq will rise another 139% from the cyclical low in the next 22 months. This indeed means that the annualized return rate would reach 61%, which is somewhat unrealistic. However, investors still have sufficient reasons to believe in the long-term growth of Nasdaq. In the past twenty years, the index has risen a total of 2,420%, with an annualized return rate of 11.3%. The period covers a wide range of economic conditions, and investors have reason to expect similar returns in the future.

Considering the broad prospects, Alphabet and Roku are worth considering for investment now.

(1) Alphabet

Alphabet's revenue mainly comes from digital advertising and cloud computing. Its subsidiary, Google, is the world's largest advertising technology company as it can attract internet users and collect data. It has six consumer-facing products and services that reach 2 billion monthly users, including Google Search, YouTube, Chrome, and Android. Its coverage and insights provided are valuable to advertisers.

According to Emarketer's prediction, by 2024, Google will account for 27.4% of global digital advertising revenue.

At the same time, Google Cloud is the third-largest cloud infrastructure and platform services provider. Google Cloud lags behind Amazon Web Services and Microsoft Azure in market share, but it has increased by one percentage point in the past year, which may continue as artificial intelligence (AI) and machine learning (ML) account for a larger proportion of IT budgets.

In fact, a recent CIO survey by Morgan Stanley predicts that Microsoft will gain the largest incremental market share in AI/ML workloads over the next three years, but Google will be the second-largest beneficiary in this area. This conclusion is supported by the early success of Google's multimodal model Gemini, which aims to compete with the model behind ChatGPT. Google's Gemini is currently the second most popular AI cloud service.

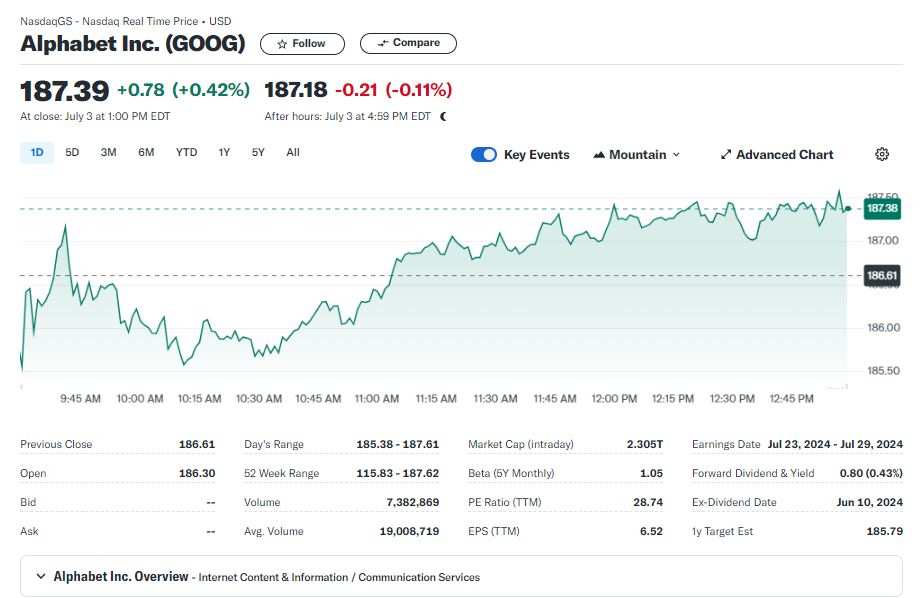

Alphabet showed its financial strength in the first quarter, with revenue and net income both accelerating. Revenue grew 15% to $80.5 billion due to the strong momentum of the Google Cloud division. Meanwhile, GAAP net income surged 57% to $23.7 billion, thanks to strict expense management.

By 2027, Wall Street analysts expect Alphabet's earnings per share to grow at an annual rate of 16%. This forecast makes its current P/E ratio of 28.2 times look reasonable. From this level, Alphabet has a good chance of outperforming Nasdaq in the next three to five years.

(Image source: finance.yahoo)

(2) Roku

Roku connects streaming content publishers and advertisers with consumers. By streaming hours, it is the leading streaming video platform in the United States, and its Roku OS is the best-selling TV operating system in the United States and Mexico. In the first quarter, about 40% of smart TVs in these two countries were Roku TVs.

In addition, it provides video-on-demand content and live TV through the ad-supported streaming service The Roku Channel, which has been among the top platforms. In fact, The Roku Channel has recently surpassed Peacock under Comcast and Max under Warner Bros. Discovery to become the seventh most popular streaming service in the United States.

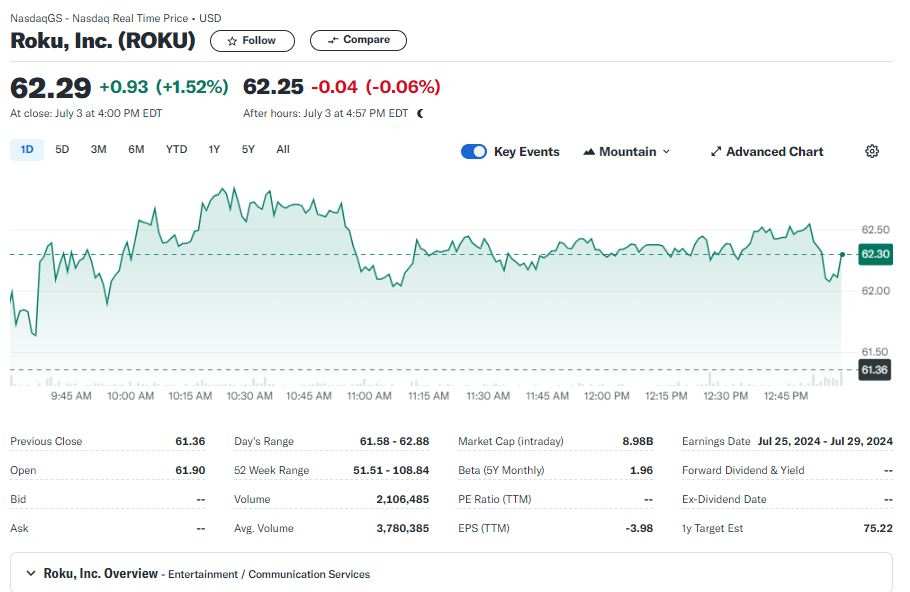

Roku reported encouraging financial performance in the first quarter. Revenue increased 19% to $882 million, accelerating from the 14% growth in the fourth quarter of 2023. Meanwhile, adjusted EBITDA improved to $41 million, compared to an EBITDA loss of $69 million in the same period last year. Investors have sufficient reasons to believe that this favorable momentum will continue.

Emarketer predicts that U.S. connected TV advertising spending will grow at an annualized rate of 13% by 2027. Roku will benefit from this growth due to its leading position in the streaming platform and the increasing popularity of The Roku Channel.

Roku will also benefit from its recent collaboration with the largest independent ad tech platform, The Trade Desk. Specifically, Roku will share data with advertisers using The Trade Desk to help them "better understand and optimize ad campaigns targeting TV streaming audiences." This will make Roku's ad inventory more attractive.

On average, Wall Street analysts expect Roku's revenue to grow at an annualized rate of 12% by 2027. Considering the broader connected TV advertising market is expected to grow faster, this estimate has room to increase.

However, even if Wall Street's forecast is correct, the stock still appears reasonably valued at the current P/S ratio of 2.4 times, and Roku has a great opportunity to outperform Nasdaq in the next three to five years.

(Image source: finance.yahoo)