Since the stock price hit a 52-week high in early March of this year, the heat of American AMD (NASDAQ: AMD) on Wall Street has significantly declined, with the stock price falling by 23%. On the market, the company's AI business growth in the first quarter of 2024 fell short of expectations, leading to a decline in its stock price. 100-300 billion yuan products operating income were 401/1288/60 million yuan respectively.

Due to lower-than-expected growth in the first quarter of 2024 in the artificial intelligence (AI) business, the company missed market expectations, which was reflected in its stock price.

# AI boom # # 2024 macro outlook # # 2024 investment strategy # # technology #

In addition, Bank of America Merrill Lynch recently downgraded the stock from buy to neutral, noting that investors' expectations for its AI business growth were too high.

While the company's main business units are recovering, the bank believes that there is limited room for AMD's stock to rise. However, it may be too early to write off the semiconductor company.

The following highlights why AMD is worth a buy for investors through two aspects.

(1) AMD is in a good position to capitalize on growth to meet the increasing sales of AI-enabled computers.

According to data from Mercury Research, AMD's market share in desktop central processing units (CPUs) for the first quarter of 2024 was 23.9%, up 4.7 percentage points from the same period last year. At the same time, its share of notebook CPUs increased by 3.1 percentage points to 19.3%.

Intel controls the rest of this market, but it is noteworthy that AMD is quickly eating away at Intel's market share.

The good news is that AMD has set its sights on the AI PC market, with its next generation Ryzen processors equipped with dedicated hardware to support AI applications. Its new Ryzen AI 300 processor is three times more powerful than the previous generation on laptops. More importantly, AMD expects its processors to support more than 150 AI software experiences by the end of 2024, so its CPUs may continue to gain market share.

Therefore, AMD has a great opportunity to maintain its strong growth momentum in customer processor business. In the first quarter, its sales revenue from deployed CPUs for laptop and desktop computers increased by 85% year-on-year to $1.4 billion.

AMD is a smaller player in the customer CPU market. Therefore, if it continues to seize market share from Intel and fully utilize the AI-enabled PC opportunity, its customer revenue is expected to grow at a rate of 44% per year over the next four years.

(2) The data center business has several solid drivers.

AMD's data center business is benefiting from the popularity of AI.

First, the company's data center graphics processing unit (GPU) business is experiencing growth due to the huge demand for AI accelerators.

This year, AMD expects to generate $4 billion in revenue from data center GPU sales. As more customers purchase its chips, AMD has raised its revenue expectations from data center GPU sales in the past few quarters.

Considering that AMD's total revenue from the data center sector last year was $6.5 billion, it can be seen that the sector is expected to achieve strong growth in 2024. It is worth noting that AMD sold $0.4 billion of data center GPUs in the fourth quarter of 2023, which means that its quarterly revenue growth in this business area may increase significantly this year.

Due to the huge income opportunities in the AI chip market, as well as the company's efforts to expand its market share through accelerated product development in this area, AMD's data center GPU revenue may maintain a good growth trend in the long run.

However, due to another AI-related opportunity in the form of server processors, AMD has another AI-related opportunity in the data center market. The company's Epyc server CPU is being used for AI inference applications and is driving strong revenue growth in the data center along with GPUs. Specifically, AMD's overall revenue in the data center for the first quarter of 2024 increased by 80% year-on-year to $2.3 billion.

Considering that AMD's market share in the server processor market increased by 5.6 percentage points year-on-year to 23.6%, and that its revenue share increased to 33%, despite Intel's spending, this should result in good results for AMD's position in the global server market, which is expected to grow at a rate of more than 12% per year over the next five years.

These driving factors explain why AMD's growth is expected to improve.

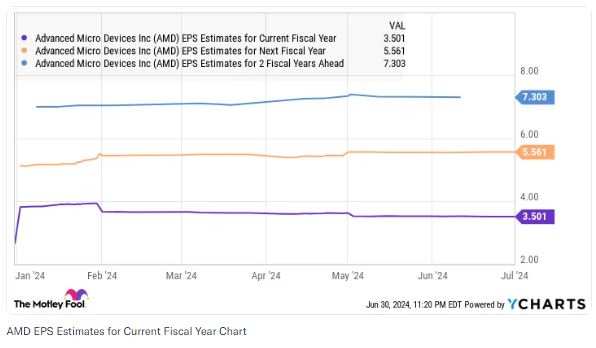

(The estimated EPS for AMD this fiscal year, image source: finance.yahoo)

Therefore, investors should keep a close eye on AMD's stock during any pullbacks, as the market may reward its stronger growth with higher future returns.

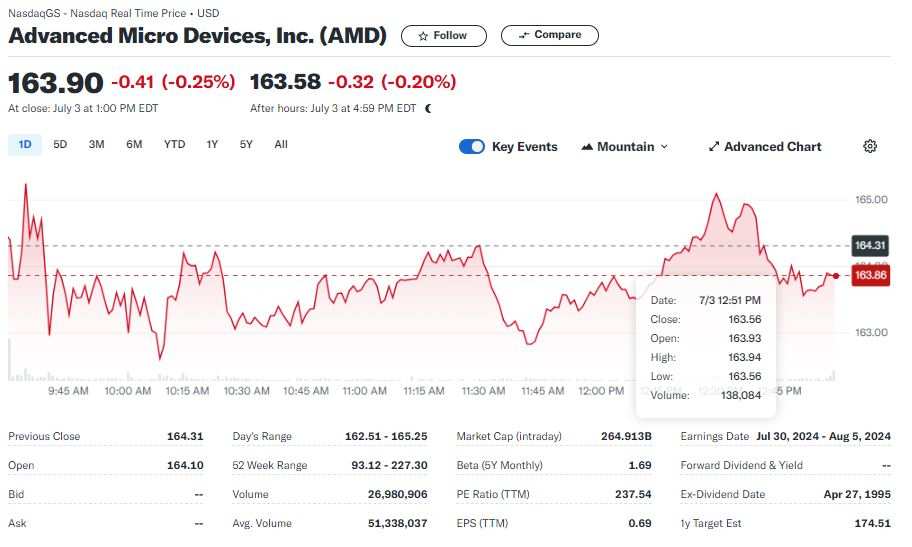

(Image source: finance.yahoo)

(Image source: finance.yahoo)