Source: Wall Street See

Nomura and other analysts point out that if the United States chooses to default, the credit of the US dollar will be damaged, which will lead to higher risk premiums for investors in US bonds, and may cause the government's interest payments to rise sharply. Without large-scale fiscal consolidation, the Federal Reserve loses its monetary policy independence, and the government implements strict financial regulation in order to press the real US bond yields to deep negative values and clear federal debt.

As Trump pursues the presidency again, the US debt crisis has once again been brought up for discussion.

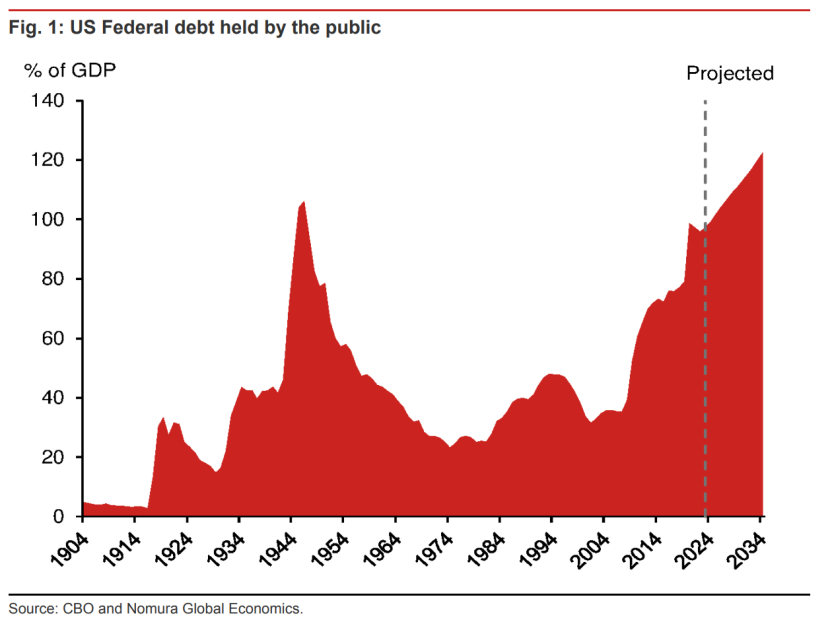

According to a report released by the Congressional Budget Office (CBO) in mid-June, US federal debt is expected to reach 109% of GDP by 2028, and will surge to 122% by 2034, which is 2.5 times the average GDP over the past 50 years. The CBO estimates that 2024 will be a milestone year when US debt interest payments exceed defense spending. However, in Nomura's view, CBO's forecast is still optimistic.

However, in Nomura's view, CBO's forecast is still too optimistic.

Nomura analysts Rob Subbaraman and Yiru Chen released a report on Tuesday stating that given the uncertainty of fiscal consolidation, inflation, and economic growth, the US fiscal problem is very serious and government debt has embarked on an unsustainable road.

When analyzing the future of the US economy, Nomura considers three scenarios: good, bad, and ugly.

The analysis points out that in extreme cases, if Trump is elected president of the United States and defaults on debt, the credit of the US dollar will be damaged, which will lead to higher risk premiums for investors in US bonds and may cause the government's interest payments to rise sharply. Without large-scale fiscal consolidation, the Federal Reserve loses its monetary policy independence, and the government implements strict financial regulation in order to press the real US bond yields to deep negative values and clear federal debt.

Good: The economy has entered a golden age, tax revenue has increased, and the deficit has decreased.

In the best of scenarios, Nomura believes that with the help of the Gen-AI revolution, the US economy may enter a period of strong growth and low inflation. By then, corporate and personal income will increase, and government tax revenue will also increase, which will help reduce the budget deficit.

At the same time, the government will use the low interest rates under low inflation to optimize the debt structure and reduce debt costs.

Under this scenario, Nomura believes that by the end of 2025, the yield on 10-year Treasury bonds will fall to 4.2% and on 2-year bonds to 3.7%.

But this scenario seems more and more like an elusive dream. Instead, the United States is more likely to face the next two more severe situations.

Bad: Inflation is high, the economy is sluggish, government revenue is decreasing, and the deficit is deteriorating.

In the bad scenario, Nomura said that inflation issues continue to exist, and the Federal Reserve's adjustments to interest rates are far less active than expected by the market.

This will lead to sustained low economic growth, and the US government will hardly make any progress in reducing the budget deficit. The Treasury Department will face the refinancing challenge of a large amount of short-term debt maturity, while private investors will require higher risk premiums to buy new long-term Treasury bonds.

This will create a vicious cycle: Government borrowing costs rise → net interest expenses increase → private investment is squeezed → economic growth slows → government revenue decreases → budget deficits continue to expand → public debt ratios rise faster than CBO initially predicted.

Ugly: Debt crisis strikes, Trump stops paying debts in extreme cases.

As for the ugly scenario, it is likely to be catastrophic.

Nomura pointed out that in this scenario, the US fiscal balance may reach a critical point - similar to the debt crises experienced by some emerging market countries. Private investors lose all confidence in US bonds, and the Treasury cannot borrow at affordable interest rates, which will trigger a severe fiscal crisis.

And the trigger for all this may be the US presidential election.

Nomura stated that whether it is the market's expectation of more fiscal stimulus caused by Trump's re-election or the loss of foreign investors' confidence in US institutions caused by election disputes, it may cause a major blow to the US's "excessive privilege".

The most extreme case is that Trump orders a suspension of debt repayment.

Nomura mentioned a recent prediction by Barry Eichengreen, former senior policy adviser to the International Monetary Fund: considering Trump's history of personal debt defaults, if he is re-elected president, he may instruct the Treasury Secretary to suspend debt payments. This decision may not be opposed by Congress or the courts, as currently about one-third of US government debt is held by foreigners.

The US default will undoubtedly trigger violent turbulence in the international financial market, and the US will suffer losses while killing a thousand enemies.

Eichengreen recently wrote that American institutions may not be as strong as they seem. If the US chooses to suspend debt repayment, even if it is eventually revoked by Congress, the courts or the next president, the credibility of the US dollar will be damaged. This will cause investors to demand higher risk premiums for US bonds, potentially sharply increasing government interest payments.

He also said that as the debt ratio rises, the federal government may need to cut discretionary spending, which may have a negative impact on economic growth.

For example, the chip bill and inflation reduction bill promulgated in 2022 aimed to stimulate economic growth by encouraging investment, but if the government needs to cut spending in response to debt growth, the effectiveness of these measures may be limited.

Nomura further pointed out that without large-scale fiscal adjustment, the Federal Reserve would lose its monetary policy independence, and the government would implement strict financial regulations in order to push the real US bond yield into deep negative territory and settle federal debt.

Nomura predicts that in the ugly scenario, the yield curve of US bonds may experience unprecedented compression, and the spread between 2-year and 10-year US bonds may drop to the lowest level in decades.

Future fiscal adjustments - a difficult challenge.

In terms of future fiscal adjustments, the United States is facing a series of challenges.

The report pointed out that the rise in debt servicing costs, the pressure of social security and medical expenses brought about by an aging population, the impact of deglobalization on economic growth and tax revenue, the increase in defense spending caused by national security concerns, the cost of climate change adaptation, and structural issues in fiscal spending limit the government's investment capabilities in key areas.

In addition, factors such as election results, policy changes, and changes in the international monetary environment have increased the complexity of fiscal adjustments.

Editor / jayden