According to the recent report from TSLombard economists, if the unemployment rate rises in June, a rate cut in July may ultimately be triggered.

TSLombard economist, Steven Blitz, recently stated in a report that the Fed is "slowly moving towards a rate cut in July". Here are the four key points summarized in the report:

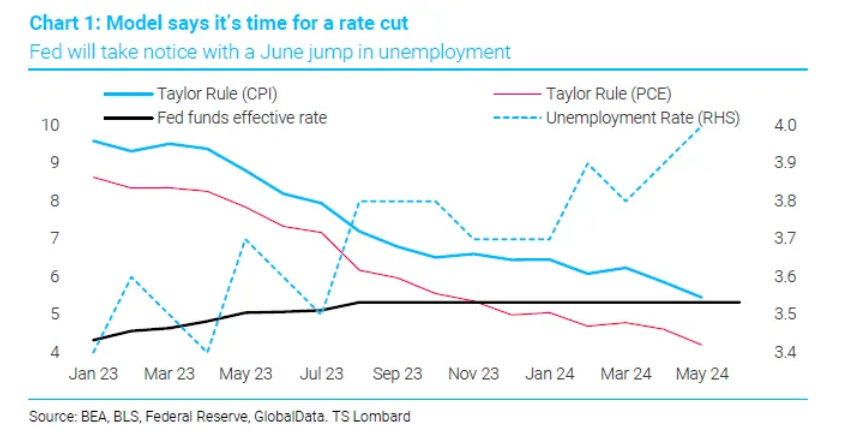

1. According to the revised Taylor rule, given that the current core PCE is 2.6%, the federal funds rate "should" be 4.2%. 2. According to TSLombard's model, if the unemployment rate increases in June, the rate cut in July may be triggered. 3. Commodity inflation is back on a downward trend, though the reason this time is different. 4. Service sector inflation has not cooled down significantly yet, but the housing market is collapsing, indicating that service sector inflation will soon see a downturn.

Blitz's report highlights the policy actions that the Fed might take. The report states that the Fed may cut rates as PCE data falls, affecting the push towards the Taylor rule. The Fed is shifting its focus from inflation control to managing economic growth signals, with this week's June employment data playing a critical role in its decision-making.

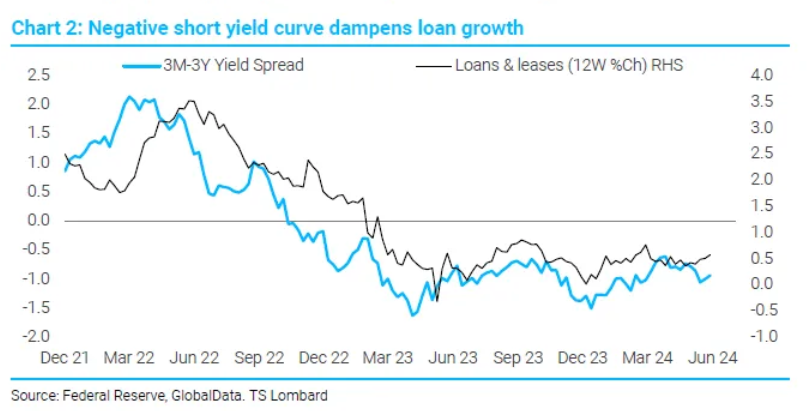

As far as the economic situation is concerned, Blitz believes that it remains as complex and changeable as ever. The Fed's goal is to maintain stability when the public is troubled by current problems. Despite a challenging environment, actual growth has shown resilience thanks to ample liquidity, and a drop in short-term interest rates could accelerate this liquidity excess. However, the threat of economic recession still exists due to an inverted yield curve and actual bank loan growth in the negative, suggesting that future economic growth will slow down.

Actual yield curve inversion and negative actual bank loan growth.

Blitz's revised Taylor rule model points to a federal funds rate of 4.2% after considering the current core PCE inflation rate of 2.6%, which means a possible 25 basis points rate cut in September. If June's employment data supports, the announcement of a rate cut may come in July.

The report also provides a detailed explanation of the inflation situation. Although overall inflation, not including food, energy, and housing, is modestly up year on year at 2.2%, this is mainly driven by commodity inflation, rather than a general decline in service sector inflation. The inflation rate for the service sector, not including housing and energy, remains above 3%, but has slowed down in recent months, indicating economic deceleration but not enough to immediately trigger concerns about recession.

Recruitment and actual discretionary spending are both slowing down but still growing. Actual discretionary spending on commodities is gradually returning to the trendline between 2012 and 2019, indicating a return to normal after the pandemic. Similarly, actual discretionary spending on services is consistent with pre-pandemic levels, but has not fully recovered. The overall economic outlook suggests that a recession will not immediately occur but that fragility is evident, particularly in the housing sector.

The report also provides a detailed explanation of the inflation situation. Although overall inflation, not including food, energy, and housing, is modestly up year on year at 2.2%, this is mainly driven by commodity inflation, rather than a general decline in service sector inflation. The inflation rate for the service sector, not including housing and energy, remains above 3%, but has slowed down in recent months, indicating economic deceleration but not enough to immediately trigger concerns about recession.

Recruitment and actual discretionary spending are both slowing down but still growing. Actual discretionary spending on commodities is gradually returning to the trendline between 2012 and 2019, indicating a return to normal after the pandemic. Similarly, actual discretionary spending on services is consistent with pre-pandemic levels, but has not fully recovered. The overall economic outlook suggests that a recession will not immediately occur but that fragility is evident, particularly in the housing sector.

Editor/new