Tinengotinib, the core product, has the potential to become the world's first effective MTK inhibitor for the treatment of various recurring or refractory, drug-resistant solid tumors. Based on the growth rate of R&D expenses in 2023, the cash on the balance sheet of Pharmaron can probably support one year of R&D expenses. After completing the D+ round of financing, the post-investment valuation of Pharmaron has reached 4.59 billion yuan.

"Star Daily" news on July 2 (Reporter Zheng Bingxun): AI pharmaceutical company Crystal Pharmatech (2228.HK) was listed on the Hong Kong Stock Exchange last month, which seems to have driven the enthusiasm of pharmaceutical companies, especially innovative drug companies, to sprint to the Hong Kong Stock Exchange. Many companies have launched a sprint to the Hong Kong Stock Exchange recently.

"Yao Jie Ankang (Nanjing) Technology Co., Ltd." (hereinafter referred to as "Yaojie Ankang") re-submitted IPO documents to the Hong Kong Stock Exchange recently after a silence of nearly 3 years.

As an innovative drug company in the registration clinical stage, Yao Jie Ankang has not yet had a product approved for listing. In terms of business, Yao Jie Ankang focuses on discovering and developing small molecule innovative therapies for tumors, inflammation and metabolic diseases of the heart, with 6 clinical stage candidate products and 1 clinical pre-candidate pipeline.

Yao Jie Ankang stated in the IPO document that it plans to continue to expand the company's existing pipeline, which will undoubtedly expand the momentum of "burning money". However, as of the end of 2023, Yao Jie Ankang only had RMB 497 million in cash and cash equivalents, while R&D investment that year was as high as RMB 344 million.

It can be seen that the success of this listing is of great significance for the further development of Yao Jie Ankang.

At least 1 year is needed to see key clinical results.

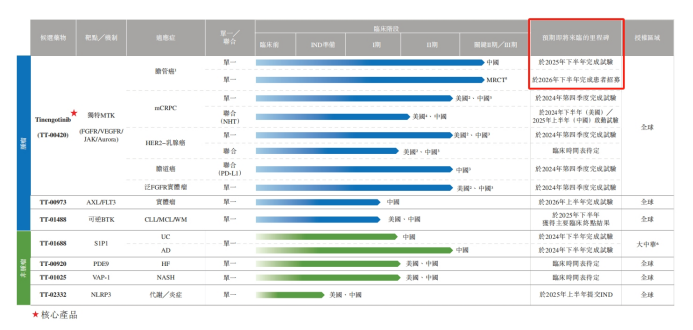

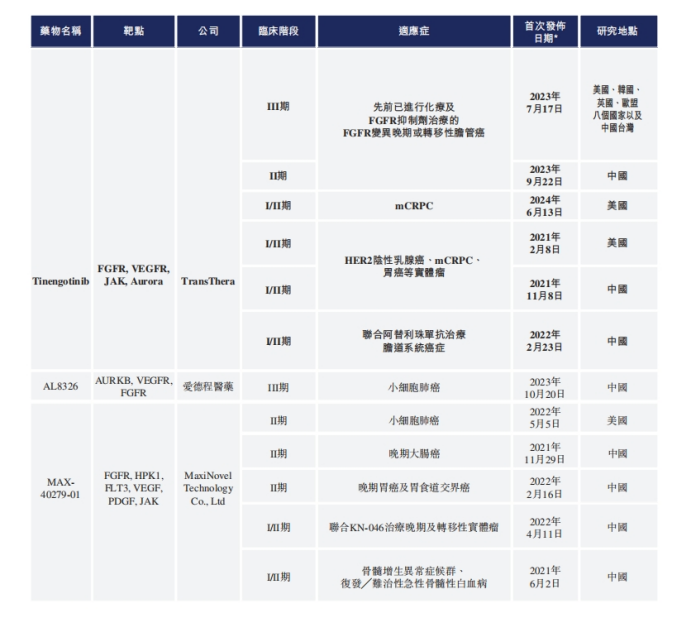

The IPO document shows that among all 7 product pipelines, Tinengotinib (TT-00420) is the core product of Yao Jie Ankang. Tinengotinib mainly targets three key pathways including FGFR/VEGFR, JAK and Aurora kinases, and has the potential to become the world's first effective MTK (multi-target kinase) inhibitor for the treatment of various recurrent or refractory, resistant solid tumors, including bile duct cancer, prostate cancer, breast cancer, cholangiocarcinoma and pan-FGFR solid tumors, etc.

Currently, Tinengotinib is the fastest R&D product among all of Yao Jie Ankang's products and is also the most promising product to achieve commercialization first. As of June 20, 2024 (the last actual feasible date), Tinengotinib has 8 clinical trials underway simultaneously, among which monotherapy for bile duct cancer indications is undergoing phase III international multicenter clinical trials in the United States, South Korea, the United Kingdom, the European Union and other places, while monotherapy for bile duct cancer indications is undergoing phase II key clinical trials in China.

Yao Jie Ankang expects that Tinengotinib will be conditionally approved in China first and then in other regions. Therefore, Tinengotinib has become the world's first and only research drug for FGFR inhibitors for recurrent or refractory cholangiocarcinoma patients that has entered the registration clinical stage.

However, it must be pointed out that the key phase II trial of Tinengotinib for bile duct cancer in China is expected to be completed in the second half of 2025, and the cross-regional phase III trial is expected to complete patient recruitment in the second half of 2026. This also means that it will take nearly 1 year for Yao Jie Ankang to know whether the key product has been successfully developed and then break the zero product sales revenue situation.

Looking at the market opportunities, Tinengotinib actually has good prospects.

For biliary tract cancer indications, Frost & Sullivan data shows that the number of biliary tract cancer patients worldwide increased from about 234,900 in 2018 to 280,000 in 2023, of which as many as 25.2% of biliary tract cancer patients observed FGFR mutations, and 7.4% of biliary tract cancer patients observed FGFR fusions and rearrangements.

The global biliary tract cancer drug market is expected to grow to $3.1 billion by 2026 and further to $5.4 billion by 2030. In 2022, the Chinese biliary tract cancer drug market reached RMB 2 billion and is expected to further increase to RMB 5.5 billion by 2026.

The safety and effectiveness of the FGFR inhibitors Pemigatinib and Futibatinib as second-line treatments for advanced/metastatic biliary tract cancer have been verified in early studies. In the United States and China, the pricing (cost) of Pemigatinib for a 21-day treatment cycle is US$19,759 and RMB 66,547, respectively, and the pricing (cost) of Futibatinib in the United States is US$27,492 per month.

Biliary tract cancer is just one of the many indications for Tinengotinib. In addition, there are pipeline programs for the treatment of metastatic castration-resistant prostate cancer (mCRPC), HER2-breast cancer, and cholangiocarcinoma in clinical phase II, which are expected to complete trials in Q4 2024.

If these indications can be successfully developed, they will also bring considerable product revenue to Tinengotinib.

For example, for the indication of mCRPC, Frost & Sullivan data shows that the number of new cases of mCRPC worldwide increased from 176,400 in 2018 to 203,900 in 2023. During the corresponding period, the number of mCRPC cases in China increased from 42,800 to 50,500. Moreover, about 60% of prostate cancer cases in China are diagnosed as late-stage or metastatic at the first diagnosis, seriously affecting the prognosis.

In 2022, the global prostate cancer drug market reached US$15.9 billion and is expected to reach US$23.5 billion by 2026. In 2022, the Chinese prostate cancer drug market reached RMB 8.2 billion and is expected to increase to RMB 24.2 billion by 2026.

Ignoring specific indications and looking only at the market potential of MTK inhibitors themselves, in 2022, sales revenues of two heavyweight original MTK inhibitors, Cabotinib and Lenvatinib, reached USD 1.4 billion and USD 1.84 billion, respectively.

However, Tinengotinib also faces potential competitors. As of the last feasible date, it was known that a targeted FGFR MTK inhibitor (Elutinib) approved by the FDA. In addition, at least three clinical stage FGFR-targeted and JAK, Aurora, and VEGFR-targeted MTK inhibitors, including Tinengotinib, are under development.

▌Cash flow on the books is rapidly declining.

In its IPO document, Pharma Block said it has hired CMOs and CDMOs to help with manufacturing in 2022 and 2023 because it has not yet established internal clinical production facilities. At the same time, Pharma Block plans to launch commercialization of Tinengotinib for the treatment of cholangiocarcinoma in China first and is currently preparing to establish an internal business team, considering the target patient population's easy access to Tinengotinib.

However, compared to commercializing products still in the research phase, Pharma Block's most pressing issue may be the cash flow shortage.

Without product revenue, Pharma Block has obtained some portions of milestone payments through licensing agreements and other matters, with scattered income of RMB 124,000 and RMB 1.181 million in 2022 and 2023, respectively. However, the various costs and expenses added up, resulting in losses of RMB 252 million and RMB 343 million, respectively, during the same period. R&D expenses are currently the largest cost. From 2022 to 2023, Pharma Block's R&D costs were RMB 263 million and RMB 344 million, respectively, of which R&D costs dedicated to the core product Tinengotinib were an astonishing RMB 167 million and RMB 236 million, respectively.

However, Pharma Block's cash and cash equivalents on the books have rapidly declined from RMB 984 million in 2022 to RMB 497 million in 2023. If calculated based on the growth rate of R&D expenses in 2023, Pharma Block's cash on the books could probably support only one year of R&D spending.

Pharma Block has clearly realized that with the continued development of products and the commercialization of candidate drugs, it will continue to spend a lot of money. The company admits in its IPO document that it may not be able to obtain sufficient funds or generate sufficient income and cash flows to continue to develop any other candidate drugs in the future. Therefore, Pharma Block stated that it may need to further obtain funds through public or private offerings, debt financing, cooperation and licensing arrangements, or other resources.

In fact, since its establishment in 2014, Pharma Block has completed multiple rounds of financing.

Among them, in the A-1 and A-2 rounds of financing completed in December 2016 and September 2017, a total of RMB 60 million was raised. In subsequent years, a total of RMB 760 million was raised in the B, C1-C3, and C+ financing rounds. In July 2021, Pharma Block raised the highest amount of funds in its history, reaching RMB 643 million in the D round of financing. Combined with the RMB 260 million it received in February 2023, Pharma Block's total financing amount has exceeded RMB 1.7 billion.

After completing the D+ round of financing, Pharma Block's post-investment valuation reached RMB 4.59 billion, which is 16 times that of the A-1 round post-investment valuation of RMB 263 million.

During this process, Pharma Block has introduced many important shareholders. According to the latest equity structure diagram, Pharma Block Sciences (300725.SZ) holds 5.79%, and Guotou Bay Area Fund and Guotou Entrepreneurship Ningbo Fund hold 3.03% and 2.65%, respectively.

As a preclinical innovative drug company, the composition of the company's core team is of great significance for the company's future business development and expansion in the capital markets.

According to the IPO document, Pharma Block's founder, chairman, and CEO are Yongqian Wu, who has 27 years of scientific and leadership experience in biopharmaceutical companies. Before founding the company, Yongqian Wu had over 10 years of research and leadership experience at companies such as Boehringer Ingelheim Pharmaceuticals Inc.

At the same time, Pharma Block's executive director and vice president of strategy and business development, Di Wu, has over 16 years of experience in the biopharmaceutical industries of China and the United States, and had previously worked at Boehringer Ingelheim.