Analysts believe that trading volume is the key. Currently, the volume of second-tier treasury bonds in a single day is between 400 and 500 billion dollars, so if the central bank wants to influence interest rates through sales, the scale of the operation must not be too small. Even if it is less than 100 billion dollars, it will require tens of billions of dollars. If it is within 10 billion, then the expected guidance is still more significant than the actual effect.

Against the backdrop of continued decline in long-term interest rates, the central bank intervened intraday on Monday and announced that it would launch a “treasury bond loan operation.”

Treasury bond futures dived in response. The 30-issue treasury bond futures closed down 1.1%. Previously, they had risen more than 0.39% and hit a record high. Recently, 30-year treasury bonds have once again begun to test the yearly low of 2.4% downward.

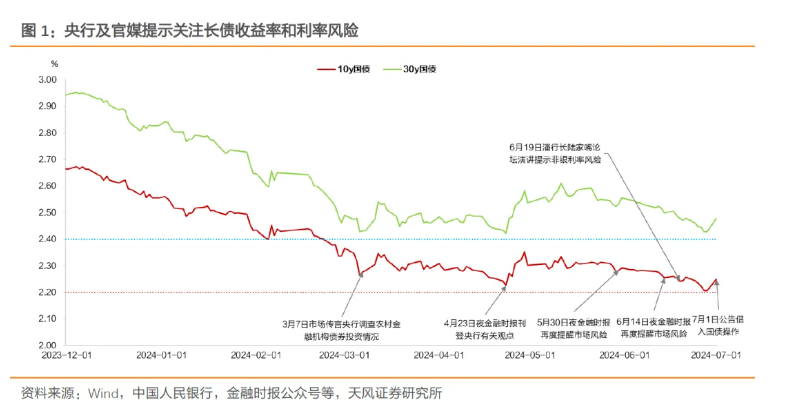

In fact, the central bank's move is no surprise. Since April, the central bank has publicly “shouted” about interest rates on long-term bonds more than ten times in a row, and the Lujiazui Forum also predicted that tools to trade treasury bonds will be launched.

So how do you understand this operation? Judging from the trading volume, how many treasury bonds can be borrowed by the central bank? Judging from history, what experiences are worth learning from?

More importantly, what impact does it have on the bond market? Will it be the end of this round of debt bulls? What will that mean for bond funds?

What details are worth noting?

Looking at the time, Minsheng Macro Tao Chuan pointed out that the central bank rarely announced a “treasury bond loan operation” during the intraday period, which reminds people of the last intraday move to stabilize the exchange rate (the foreign exchange self-regulation mechanism meeting was held at noon on September 11 last year+financial data released).

Tianfeng Fixed Income pointed out that first, the central bank made an operation announcement on July 1, which may have deliberately avoided the important point of the end of June. If the announcement is in mid-late June, the impact on the bond market may be different. Second, the central bank has yet to significantly increase liquidity, which indicates that it may still have some care for the market.

In terms of content, Huatai Securities pointed out that this announcement was published as “Open Market Business Notice [2024] No. 2” on the central bank's official website. Previously, this section published the list of Tier 1 traders. This means that treasury bond borrowing is a new tool, which is different from previous models such as positive repurchases and bill swaps.

What to do after borrowing? It's likely to sell.

Huatai Securities pointed out that the central bank has made it very clear, “to maintain the steady operation of the bond market,” so it is likely that it will be sold. Let's look at the specific operation:

Similar to a bond loan, the central bank should sell the current loan, buy and repay the securities in the forward period, and the interest for the period belongs to the lender. It is equivalent to increasing supply in the secondary market in the short term and increasing demand in the secondary market in the future, but it actually depends on the loan period and the central bank's operation after maturity.

Everbright Securities also believes that apparently, the main purpose of the central bank borrowing treasury bonds this time is to take the opportunity to sell them in the future, release monetary policy signals, promote the balance between supply and demand for long-term interest rate products, and use this to guide the upward trend in long-term treasury bond yields. Everbright Securities stated:

Some investors believe that in the future, the central bank will eventually pay back the bonds it has borrowed, so the central bank will buy them back in the market, and the operation of buying bonds at that time will once again drive the yield downward. We think this is true, but this is a long time later and is not a key factor affecting the current market trend. Moreover, the timing of buying bonds is determined by the central bank; it is likely that they will choose to buy when the yield is too high.

How many treasury bonds can the central bank borrow? What historical experiences are worth learning from?

Second, trading volume is key.

Huatai Securities stated:

Currently, the volume of second-tier treasury bonds is between 400 and 500 billion dollars in a single day, so if the central bank wants to influence interest rates through sales, the scale of the operation must not be too small. Even if it is less than 100 billion dollars, it will require tens of billions of dollars. If it is within 10 billion, then the expected guidance is still more significant than the actual effect.

According to escrow data released by China Bonds, as of May 2024, commercial banks held 20 trillion treasury bonds, mainly major banks. According to a rough estimate, after deducting requirements such as pledges, the treasury bonds that Tier 1 traders can lend are about 8 trillion dollars. However, the term of these treasury bonds is generally not too long.

Judging from historical experience, Minsheng Macro pointed out that the newly proposed “treasury bond loan operation” was not mainstream in history. In theory, there are two ways for central banks to sell treasury bonds on the open market. One is through positive repurchase, and the other is to sell cash. Most of the two appeared from 2000 to 2014. The central bank's “treasury bond loan operation” statement is different from the above two. We think there may be two institutional experiences worth referring to:

The first is the lower-end scenario of the Bank of Japan YCC. That is, when long-term bond yields hit the lower interest rate limit, the central bank can sell treasury bonds in large quantities, affecting supply and demand in the secondary bond market and boosting interest rates. However, in the context of Japan's long-term ultra-loose monetary policy, there aren't many cases that triggered the YCC to sell treasury bonds later by the Japanese central bank.

Second, China's central bank's previous “stable exchange rate” operation. Historically, China's central bank has borrowed US dollars in the forward market and sold US dollars in the spot market to release foreign currency liquidity and hedge against depreciation pressure on the RMB. The operation logic of “borrowing first and then selling” may be similar to this “treasury bond loan.”

Is the significance of this signal greater than the substance?

Minsheng Macro points out that as far as this is concerned, the significance of the signal may be greater than the substance:

Taking Japan as an example, the central bank needs to go through large-scale treasury bond transactions to regulate market interest rates. At the end of 2023, the central bank accounted for 48% of the treasury bond holder structure, while the central bank of China was only 5%. The impact of selling treasury bonds on market supply and demand is limited. We believe that it is unlikely that the central bank will follow the path of “Japanized” deficit expansion and massive debt purchases in the future. Instead, it is moving closer to the previous “intrusive” exchange rate stabilization operation, so there are more signal intentions to correct the market.

Historical experience tells us that if the market's reaction to expected guidance is too lackluster, the central bank is more likely to step up its efforts to guide expectations and begin to use other policy tools to ultimately confirm and collaborate between central bank policy operations and external communication, and maintain the “consistency of words and actions” of maintaining expected guidance.

Everbright Securities believes that compared to the scale of operations, the attitude of regulators is more critical:

The size of a single treasury bond loan is limited, and even if sold entirely, the impact on the market is limited. We need to restate the basic idea that “the attitude of regulators is more critical than the use of specific tools”.

Furthermore, the central bank has not made it clear that it will only carry out a treasury bond loan operation once. If the trend in the bond market does not satisfy the monetary authorities for some time to come, then it makes sense to start borrowing and selling treasury bonds again and use the rest of the policy tools.

What impact does it have on the bond market? Will it be the end of this round of debt bulls?

Huatai Securities stated:

Phased adjustments are unavoidable. First, the central bank's borrowing of treasury bonds shows its determination to regulate long-term interest rates. Phased adjustments are inevitable, and the bottom of interest rates is clear for the time being.

However, as far as debt is concerned, the downward logic of long-term interest rates has not fundamentally changed. The central bank clearly needs to control the risk of interest rates falling too fast and stabilizing the spread between China and the US.

This is similar to the opinion of Tianfeng Gushou Sun Binbin's team:

We judge that currently we are still in the macroeconomic logic of steady growth and monetary broadening, so there is no simple reversal in the bond market, there is still a possibility of interest rate cuts, and the overall trend of declining interest rates has not changed. So full defense isn't enough.

However, from a phased perspective, the short term may still be biased towards range-bound fluctuations, with interest rates in the bond market peaking and bottoming. Since the central bank's behavior still requires further observation, no adjustments will be considered for the time being, and will be bought.

Huatai Securities further stated:

The 2016 debt boom ended with financial deleveraging. The early period was a rise in fundamentals (real estate+external demand). The original purpose of this round of the central bank's debt sale was not to crack down on financial leverage; it was more to “cool down” the bond market. Moreover, the central bank's intention is not to allow major adjustments in the long term, because once it triggers a feedback cycle or affects fiscal debt issuance, it is not conducive to economic recovery and monetary policy transmission.

From the perspective of the curve pattern, this operation can also be understood as a yield curve control tool. Judging from the June cross-season investment, the central bank does not want to cause short-term capital fluctuations, and short-term interest rates are generally stable. The long term may be the focus of regulation. If long-term bonds are sold later, the curve pattern will tend to steeper.

Overall, 30-year treasury bonds have not escaped the 2.4%-2.6% fluctuation range we previously predicted. The odds are declining near the lower limit, and we need to pay attention to central bank movements. Obviously, adjustments are still an opportunity. After all, the fundamental logic (financing demand, real estate, production is stronger than demand) is unwavering. For large amounts of long-term underallocated capital, as long as the point is high enough, the fluctuations in the middle are only short-term disturbances.

What is the impact on bond-like assets?

Everbright Securities advises that we also need to pay attention to price fluctuations for bond-like assets:

The round of rising yields in the fourth quarter of 2022 triggered a decline in the net value of asset management products such as bank wealth management and public funds. Along with the decline in the fund's net worth, fund shares have shrunk. At the end of the fourth quarter of 2022, the shares of short-term pure debt funds, medium- and long-term pure debt funds, hybrid bond tier 1 funds, and hybrid bond tier 2 funds decreased by 35.2%, 5.7%, 15.8%, and 9.7%, respectively, compared to the end of the third quarter of that year.

Moreover, the decline in net value and share of asset management products such as funds during that period also had a mutually reinforcing effect. Although the current bond market is not entirely consistent with the situation before the fourth quarter of 2022 adjustments, there are also many similarities. In fact, there are quite a few negative factors currently, but investors have either intentionally or unintentionally overlooked them. At this point, investors need to start dealing with price fluctuations in bond-like assets in advance in order to protect the “money bag”.

This article is excerpted from Huatai Fixed Income's “Central Bank Treasury Bond Borrowing Operations: New Tools and Policy Fundamentals”, Minsheng Macro Tao Chuan's “The “Mystery” of Central Bank Borrowing”, and Everbright Securities's Fixed Income Research “How to Understand the Central Bank's Treasury Bond Borrowing?” As well as Tianfeng Gusu Sun Binbin's team “The Central Bank Borrowed Treasury Bonds, and the Bond Market Turned Defensive? 》