After the Shanghai Composite Index fell below the 3,000 mark last week, the Hang Seng Index also fell below the 18,000 mark last week. With the continuous market pullback in recent weeks, investor sentiment has become increasingly depressed. The outflow of foreign capital may also increase the pressure on A-shares and Hong Kong stocks. In addition to depressed sentiment, uncertainties in the overseas environment are also increasing, mainly reflected in the prospect of interest rate cuts and the so-called "Trump Trade".

We do not worry too much about the increase of internal and external uncertainties which may continue to disturb the market in the short term, and we believe that there will be some support for the Hang Seng Index near 18,000 points. Even if it comes under pressure due to unexpected impacts, the probability of success of intervention is relatively high.

Compared with A-shares, the advantages of Hong Kong stocks are: 1) The position of foreign capital and the clearance of chips are relatively sufficient, 2) The valuation clearance is relatively sufficient, and 3) The difference in profit and benefit structure is more advantageous. Looking ahead, the market space comes from the repair of domestic fundamentals and the catalyst of policies. July 1 coincides with the 27th anniversary of Hong Kong's return to China. The market is highly concerned about whether measures such as the implementation of Hong Kong stock connect dividend tax, adjustments to the admission standards for mainland investors, and RMB counter business can be launched.

We believe that under the macro environment of not significantly increasing leverage, the possibility of index-level market trends is not high. However, under the policy intention of "stabilizing leverage", the market is not unilaterally downward as in the period of "leveraging", but presents structural trends in a volatile pattern. How to find structural opportunities? Currently, assets that can provide "active money" are becoming more and more scarce, and more wealth management and insurance funds also tend to invest in such assets to meet the needs of the liability side, which makes companies that can provide abundant and stable free cash flow more and more attractive.

Scarcity assets under current circumstances

Market trend review

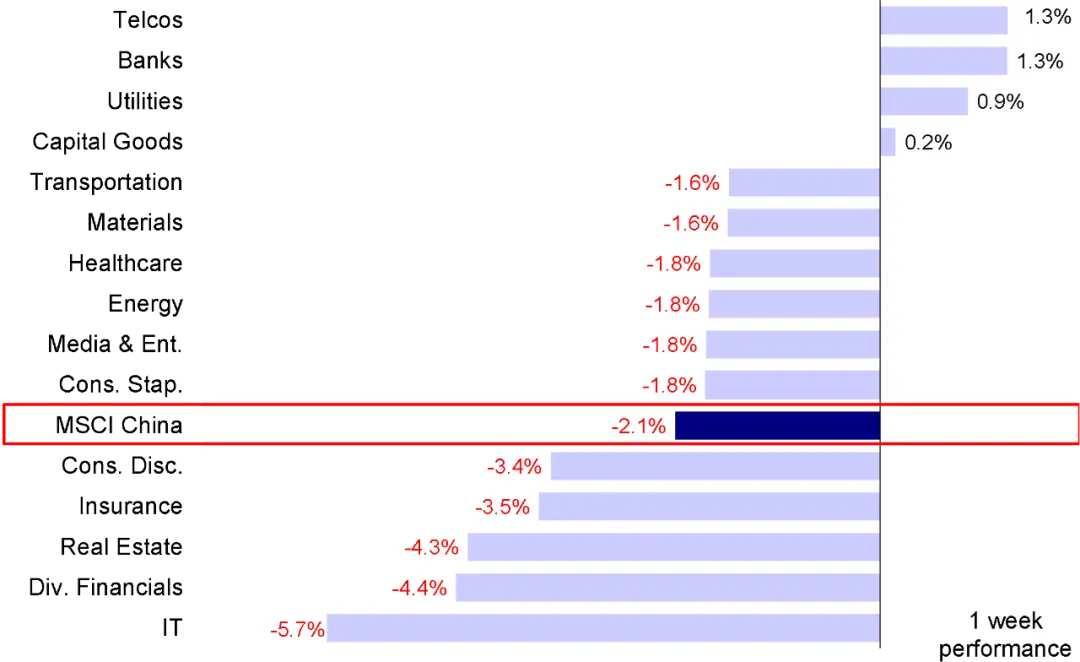

Last week, the Hong Kong stock market as a whole came under pressure, especially on Thursday, the Hang Seng Index fell below the 18,000-point mark due to worries about the depreciation of the exchange rate and the adjustment of dividend tax. Among the major indices, the Hang Seng Index and Hang Seng National Enterprise fell by 1.7%, MSCI China fell by 2.1%, and the Hang Seng Technology with a higher proportion of growth stocks came under greater pressure, falling by 4% for the week. In terms of sectors, information technology (-5.7%), diversified financials (-4.4%), and real estate (-4.3%) lagged, while communications services and banks rose by 1.3%, relatively outperforming.

Chart: Old economy sectors such as communications services and banks led the gains, but the information technology, diversified financials, and real estate sectors were clearly under pressure last week.

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that this round of rebound is mainly driven by the funding side and emotions. Therefore, with the market entering the overbought range, investors' divergences and profit-taking are not surprising. Assuming that the risk premium is fully restored to the level of the high point at the beginning of 2023, the corresponding target index level of the first stage of the Hang Seng Index is 19,000-20,000 points (see May 12th "The market is approaching our first stage target" and May 26th "not surprisingly taking profits"). In the past few weeks, overseas funds, especially value-oriented active foreign funds, have flowed out again. The outflow scale this week has increased from USD 93.24 million last week to USD 340 million. This can also provide proof ("Active Foreign Funds Maintain Weakness"). However, with the recent continuous decline of the market, especially A shares falling below 3,000 points again, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we are not so worried, although we have always believed that further upward momentum needs more catalysts to start, it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support, and looking back at this week's market performance also confirms our previous judgment ("temporary pause or end of rebound"). In addition, compared with A shares, which have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares ("The Hong Kong stock market still has a comparative advantage").

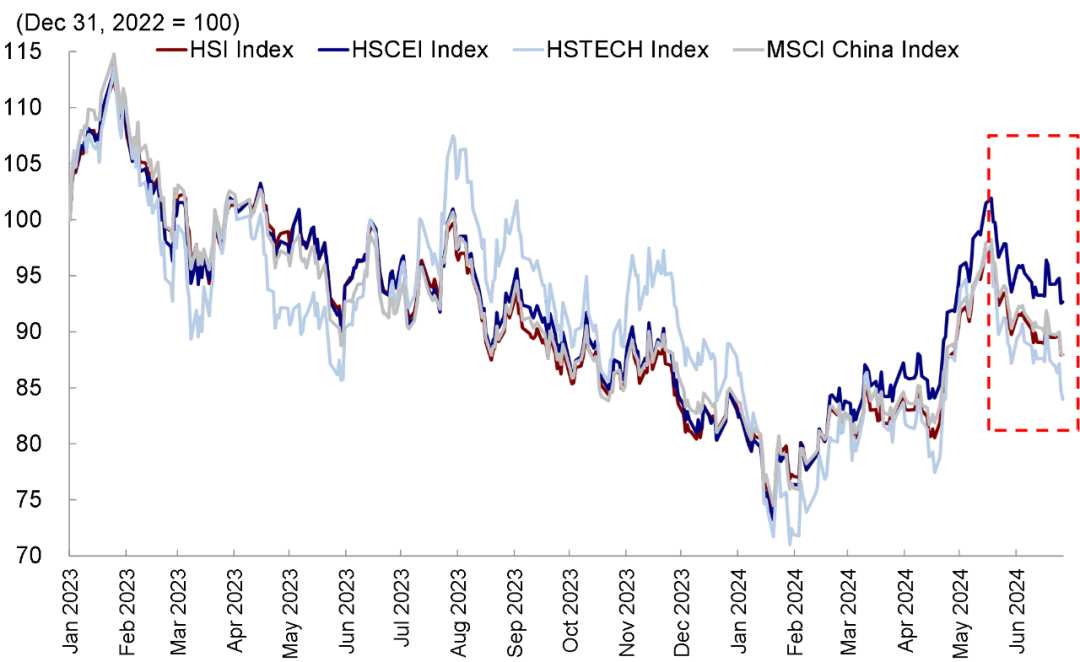

With A-shares continuing to come under pressure, Hong Kong stocks last week extended their weakness since mid-to-late May. After the Shanghai Composite Index fell below the 3,000-point mark in the previous week, the Hang Seng Index also lost the 18,000-point mark last week. Calculated since the market's high point on May 20, the Hang Seng Index has fallen by 10% in the past month, and Hang Seng technology has fallen by nearly 15% over the same period, giving up half of the rapid rebound from the end of April to late May.

With the continuous market pullback in recent weeks, investor sentiment has become increasingly depressed. The daily turnover of the main board of the Hong Kong stock market (5-day moving average) has fallen from a high of HKD 170 billion in late May to less than HKD 100 billion. The ratio of short selling turnover has also risen from a low of 12.9% to 16.7%. In addition, with the continuous strong performance of the US dollar and the offshore renminbi falling below 7.3, the pressure of foreign capital outflow may also increase the pressure on A-shares and Hong Kong stocks. Northbound capital flowed out more than 10 billion on Thursday, and EPFR data showed that active foreign capital accelerated its outflow last week by USD 380 million compared to the previous week.

Chart: The Hang Seng Index fell below the 18,000-point mark and has given up more than half of its gains from the rapid rebound process before.

The recent outflow of overseas capital and the market pullback also confirmed our previous judgment that the main force behind promoting market rebound in the previous period was mainly trading-type funds and some regional rebalancing funds, and the expected long-term value-oriented fund has not yet formed a trend of return. At the same time, the Hang Seng Index has also begun to pull back after reaching our first stage target of 19,000-20,000 points.

In addition to depressed sentiment, uncertainties in the overseas environment are also increasing, mainly reflected in the prospect of interest rate cuts and the so-called "Trump Trade". Some Federal Reserve officials last week said that they did not expect interest rate cuts in 2024, which sparked concerns. At the same time, on the morning of June 28th, Beijing time, Biden and Trump held the first-round debate in the US presidential election.

Judging from the polls and market feedback, Trump's lead expanded after this round of debates. We sorted out the similarities and differences in the policy proposals of the two parties in various aspects and found that most of them are inflationary, especially in Trump's trade tariffs, investment, immigration, and taxation, which may also constrain the subsequent downward space of interest rates. The yield on 10-year US Treasuries soared to 4.4% on Friday, which may be brewing the "Trump Trade".

Therefore, the increase in internal and external uncertainties cannot be ruled out in the short term to bring disturbance to the market, or even greater pressure. But compared with the growing concerns in the recent market correction, we are not too worried. The Hang Seng Index will have some support near 18,000 points, and even if it is short-term pressure due to unexpected impact, the probability of intervention is relatively high. Moreover, the Hong Kong stock market still has structural opportunities and is probably better than the A-share market. Compared with A-shares, the advantages of Hong Kong stocks are:

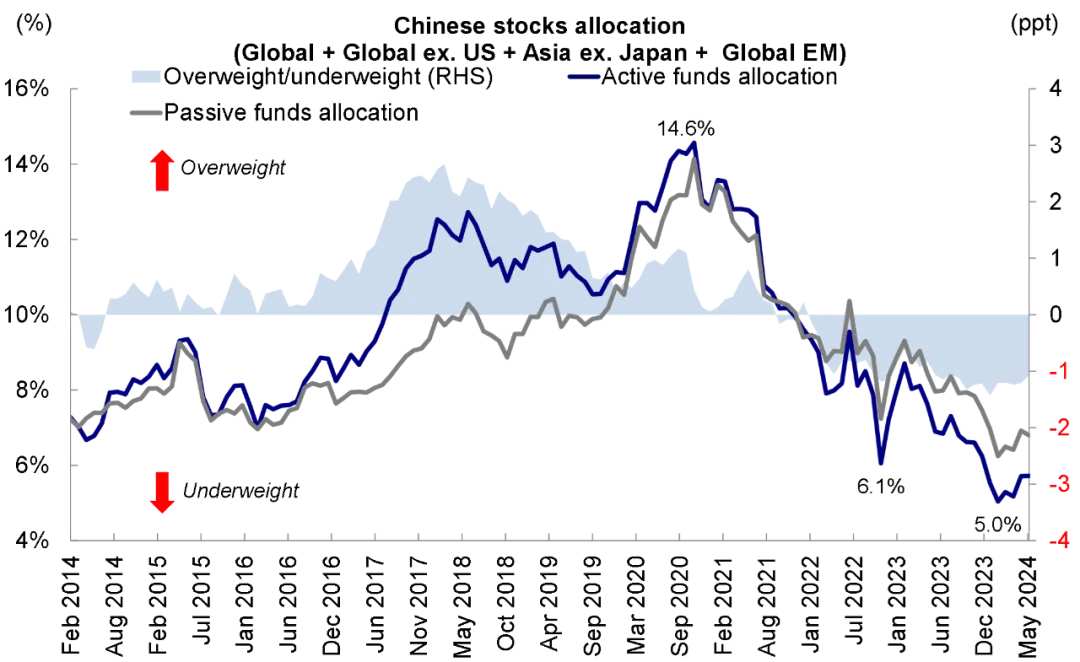

1) Foreign positions and chip clearance are relatively sufficient. The allocation ratio of various types of active funds in EPFR to Chinese stocks has dropped from the peak of 14.6% in October 2020 to the low of 5% at the beginning of the year (slightly increased to 5.7% at the end of May). Although this low level cannot serve as a basis for large-scale foreign capital inflows, the impact and pressure from this level are much smaller than the impact from the high point of 14.6% to 5%.

Chart: The proportion of Chinese stocks in various types of active funds' global allocation has dropped from 14.6% in 20 to the current 5.7%, and is underallocated by 1.1ppt.

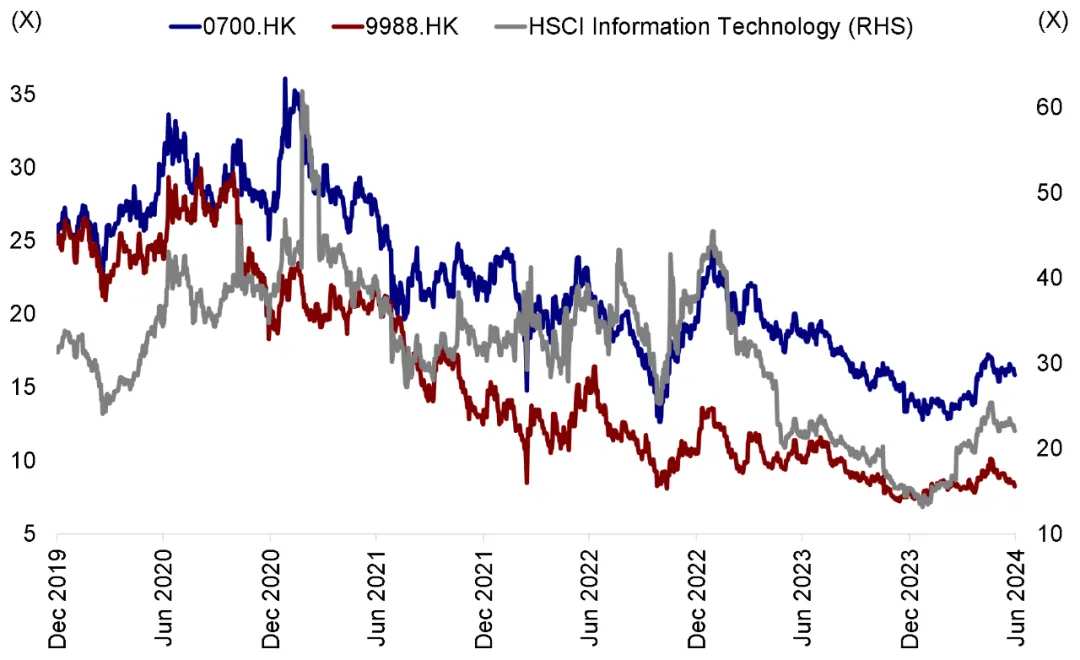

2) Valuation clearance is relatively sufficient. Hong Kong stock valuations are still lower than the average of the past ten years' 1.7 standard deviations, and the Internet, as the "core asset" of Hong Kong stocks, has been relatively sufficient after three years of adjustment, with comparative advantages. The dynamic price-earnings ratio of the technology industry in the Hang Seng Index has dropped from the high point of 61.9x at the beginning of 2021 to the current 22.1x, a drop of nearly 70%.

Some key individual stocks, such as Tencent and Alibaba, have also fallen by more than 55% in dynamic P/E ratio compared with their highs at the end of 2020 and beginning of 2021. By comparison, A-share "core assets" such as the consumer sector have seen relatively shallow valuations. Taking a consumer sector "core asset" in A-share as an example, the current dynamic P/E ratio is 21.0x, and the callback from the high point of 32.2x at the beginning of 2021 is about 34.8%.

Chart: Valuations of Hong Kong Internet sector and some key individual stocks have significantly dropped in the past three years

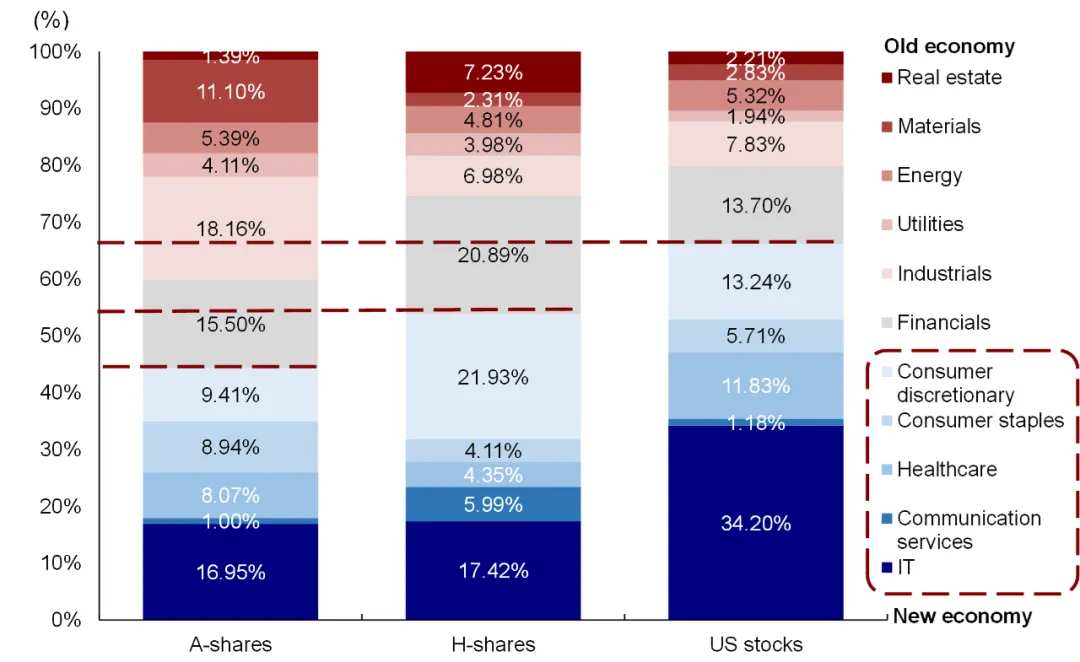

3) Differences in profit benefit structure are more advantageous. Since this year, the upstream cycle and Internet sectors have performed well, which is also the sector with greater weight in Hong Kong stocks. The real estate chain and midstream manufacturing, which account for a large proportion of A shares, generally suffer from profit pressure. This is also reflected in the latest sub-items of industrial enterprise profit over 1-5 months, where the profit growth rate from January to May this year increased by 3.4% year-on-year, down 0.9 percentage points from the previous four months. Among them, upstream industry profits continue to recover, with a year-on-year increase of 6.1%, while downstream profit growth rate has slowed down from April's 13.9% to 4.5%, and midstream manufacturing profit growth rate has changed from April's 13.5% to -1.5%.

Chart: Compared with A-shares, Hong Kong new economic stocks have higher proportion and more comparative advantages in terms of profits

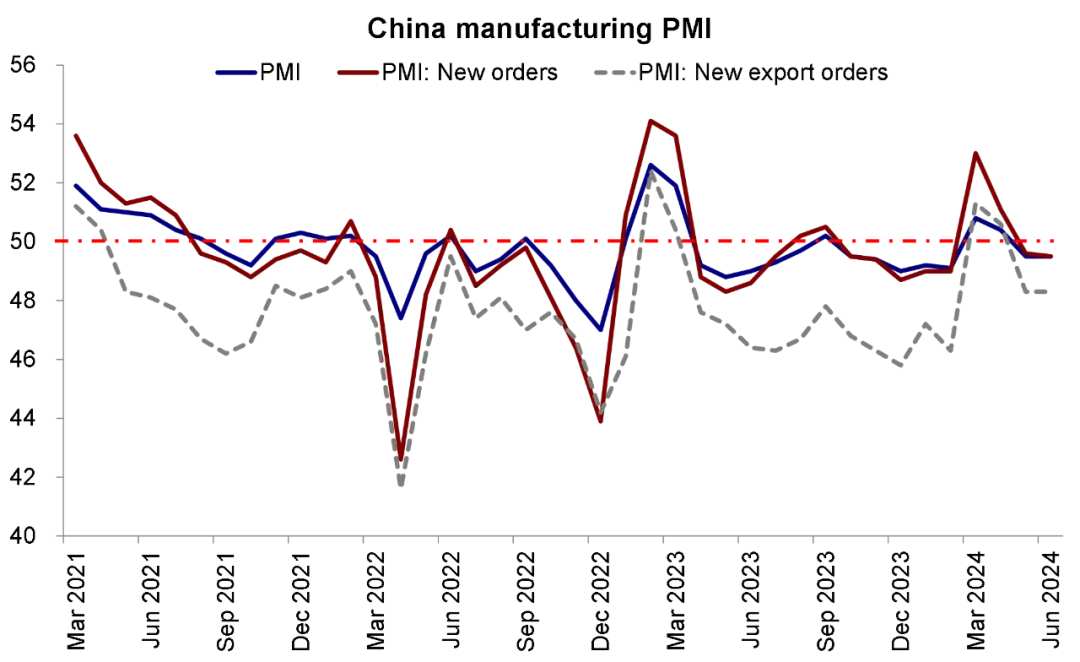

Looking ahead, the market space comes from the restoration of domestic fundamentals and policy catalysts. High-frequency data shows that the production side such as blast furnace operating rate has been repaired, but the consumption side is still weak, and some price indices such as coking coal and rebar steel also weakened last week. At the same time, China's manufacturing PMI in June was 49.5, continuing to be in the contraction zone, while the non-manufacturing PMI fell 0.6 from the previous month to 50.5. Against this background, the important policy window at home and abroad in July is worth paying close attention to.

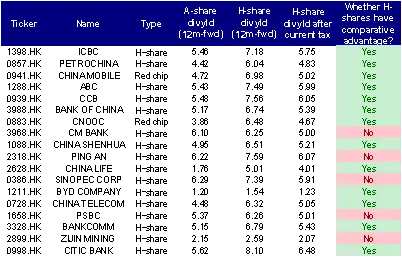

Chart: If the Hong Kong stock market's dividend tax for Southbound Stock Connect is adjusted, it is expected to further boost related dividend sectors and targets in Hong Kong stocks

In summary, we believe that in the macro environment where there is no significant "leveraging", the possibility of a exponential market is not high. However, under the policy intention of "stabilizing leverage", the market will not fall unilaterally like in the "deleveraging" period, but rather show a structural market under a shaking pattern, similar to those in 2012-2014 and 2019. In fact, if we look back at the performance of the Hong Kong stock market in the first half of this year, it can be found that there were bright spots in the structure under the pattern of overall index shaking, which is much better than the market's unilateral decline last year.

So, how to find structural opportunities? Recent financial data from a macro perspective can provide us with an idea. Current M1 and M2 have both fallen substantially, indicating that corporate "live money" has decreased, and at the same time, residents have also moved their deposits to wealth management products and insurance. This makes assets that can provide "active money" increasingly scarce and attractive on the one hand.

On the other hand, more wealth management and insurance funds will also tend to invest in assets of this kind to meet the demand of the liability side. From the perspective of financial indicators, this corresponds to companies that can provide sufficient and stable free cash flow (FCF). We found that the best-performing targets in the Hong Kong stock market since the beginning of the year are often characterized by a fast-growing FCF or relatively abundant market capitalization (free cash flow yield).

Chart: Among the targets with a market value of more than HKD 30 billion since the beginning of the year, the best-performing targets often have the characteristic of sufficient free cash flow.

Regarding the configuration, we suggest focusing on three directions in the second half of the year: overall downside return (stable return with high dividends and high repurchases, i.e. cash cows with ample cash flow), partial leverage (policy support and technology growth with still strong potential), and partial price increase (monopoly sectors, upstream and utilities).

First, we remain bullish on stable cash cows such as traditional telecommunication, energy, utilities, and some internet consumer products to capture long-term value in the context of declining overall return on investment. If the dividend tax for Hong Kong shares is actually adjusted in the future, these sectors are expected to be further boosted. The CICC's Hong Kong high dividend portfolio has risen by 28.0% since the beginning of the year, proving the effectiveness of this strategy.

Second, some policy-supported or market-propelled sectors are still expected to have greater elasticity. The Third Plenary Session of the 18th CPC Central Committee is expected to introduce further policies to support the development of emerging strategic industries. Therefore, we are bullish on some market-propelled sectors, such as electrical equipment, technology hardware, semiconductors, software and services, which still have potential for leverage and growth.

Third, compared to some industries with lower prices hurting profit margins, sectors with price increases, such as natural gas, nonferrous metals, utilities, and even some necessary consumer goods, can protect enterprise profit margins and enjoy greater bargaining power.

Specifically, the main logic that supports our above views and the changes that needed to be noted last week mainly include:

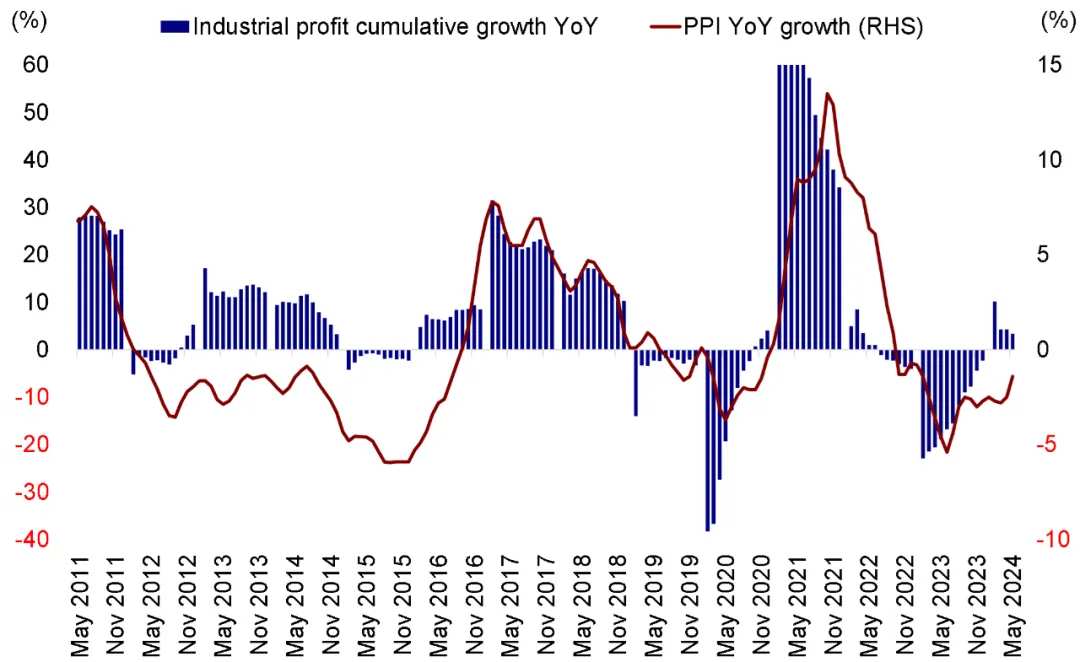

1) From January to May of this year, the growth rate of profits of industrial enterprises above designated size fell. From January to May 2024, the profits of industrial enterprises above designated size increased by 3.4% year-on-year, down 0.9 percentage points from the growth rate in January to April. For a single month, in May 2024, the profits of industrial enterprises above designated size increased by 0.7% year-on-year, down 3.3 percentage points from the growth rate in April this year. In terms of profit structure, the decline in mining industry profits has narrowed, and the growth rate of profits from manufacturing and utilities has declined.

In May, the profits of the mining industry fell by 6.4% year-on-year, a decrease of 12.5 percentage points from the decline in April this year; the profits of the manufacturing industry increased by 1.5% year-on-year, a decrease of 6.7 percentage points from the previous month; the profits of utilities increased by 6.6% year-on-year, a decrease of 22.0 percentage points from the growth rate in April. Among them, in the manufacturing industry, upstream profits continue to recover, and the growth rate of mid- to downstream profits has slowed down.

Chart: National Industrial Enterprises' Profits Above Designated Size Decline Again in May

2) In June, China's manufacturing PMI was the same as the previous month, at 49.5%. China's manufacturing PMI was 49.5% in June 2024, the same as the previous month, indicating that the manufacturing industry is still weak. Among them, the production index is still above the critical point, but it dropped by 0.2 percentage points from the previous month to 50.6%. The new order index fell by 0.1 percentage points from the previous month to 49.5%, indicating a slight decrease in demand for the manufacturing industry.

At the same time, the non-manufacturing PMI fell by 0.6 percentage points from the previous month to 50.5%, but it is still above the critical point.

Chart: China's Manufacturing PMI Was Again in the Shrinking Zone in June

3) The first presidential debate of the 2024 US presidential election was held, and Trump's advantage has expanded. On the morning of June 28th, Beijing time, Biden and Trump held the first round of presidential debates in the United States. From the polls and market feedback, Trump performed better in this debate and took the lead in expanding his advantage. According to a CNN survey, 67% of the public believed that Trump won the first debate.

However, there are still more than four months before the general election, and the final result is still subject to major changes. Investors are advised to closely monitor this situation.

4) The US PCE index cooled down, but some Federal Reserve officials expressed a hawkish stance. In May, the core PCE price index in the United States rose by 2.6% year-on-year, which is in line with market expectations and has cooled down from 2.8% in the previous month, and the month-on-month growth of 0.1% is also in line with expectations. In May, commodity prices fell by 0.4% month-on-month, with energy prices down 2.1%, offsetting the impact of a 0.2% increase in service prices.

The market believes that the PCE data meeting expectations is expected to boost the possibility of a Fed rate cut in September. However, some Federal Reserve officials expressed a hawkish stance last week. For example, Fed Governor Bowman even said that he did not expect any rate cuts this year and changed the expected rate cut time to 2025. Therefore, the uncertainty of whether the Fed will cut interest rates this year is still high.

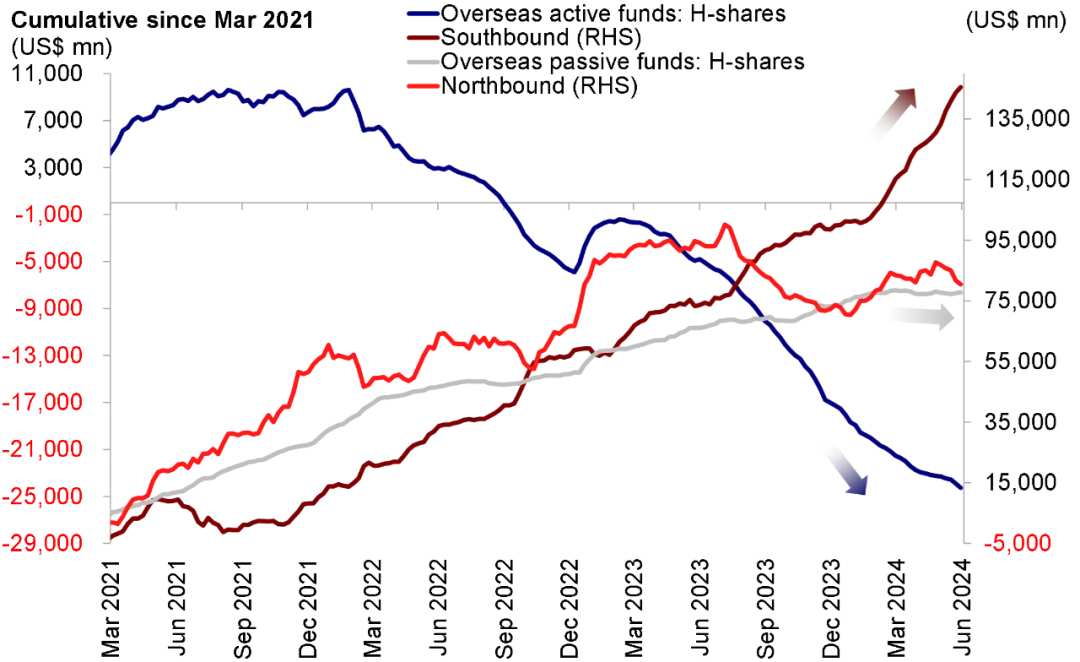

5) Last week, southbound funds continued to flow in, and overseas active funds maintained outflows. Specifically, according to data from EPFR, last week, active overseas funds flowed out of overseas Chinese stock markets, with an outflow scale of about $380 million, which is an expansion from the outflow of $340 million the previous week, and the outflow has continued for 52 consecutive weeks. Passive overseas funds continued to flow in, with a scale of US$260 million. Southbound funds maintained the trend of inflow last week, with a cumulative inflow of HK$9.33 billion, but it slowed down from HK$24.12 billion inflow the previous week.

Chart: Active Overseas Funds Continue to Flow Out of Overseas Chinese Stock Markets Last Week

Edited by Jeffrey