R&D expense ratio is lower than the average of comparable companies in the same industry.

According to Gelun Hui, recently, Jiangsu Youli Intelligent Equipment Co., Ltd. (hereinafter referred to as "Youli Intelligent") submitted a prospectus (declaration draft) to the BSE. The company's sponsoring institution is Huatai United Securities Co., Ltd.

Youli Intelligent is an enterprise focused on the research and development, production, and sales of core components of photovoltaic brackets. As for the equity structure, as of the signing date of the prospectus, Juzhou Machinery directly holds 21 million shares of the company, accounting for 68.19% of the total number of shares, and is the controlling shareholder of the company.

The actual controller of Youli Intelligent is Li Tao, Li Kailin, and Zhu Hong. The three of them together control 81.49% of the voting rights of the company. Li Tao is the chairman of Youli Intelligent, Li Kailin is Li Tao's father, and Zhu Hong is Li Tao's mother.

According to the prospectus, Li Tao was born in 1988 and has a bachelor's degree. From June 2012 to April 2016, he worked as a supervisor at Wujiang Juzhou Machinery Co., Ltd., and also served as the manager of the marketing department and the general manager of the general office. From April 2016 to January 2024, he served as a director and general manager of Juzhou Machinery. From April 2023 to present, he has been the chairman of Youli Intelligent.

According to the prospectus, Youli Intelligent plans to raise approximately RMB 358 million this time for the construction of a production base for core components of photovoltaic brackets; the construction of a research and development center; intelligent transformation and expansion projects; and supplementary working capital.

R&D expense ratio is lower than the average of comparable companies in the same industry.

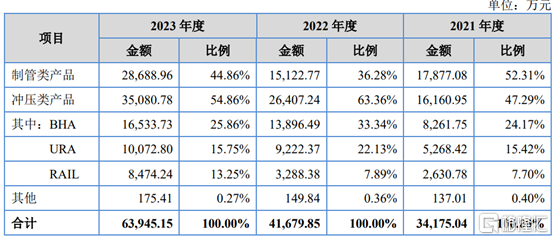

Youli Intelligent's main products are core components of photovoltaic brackets. According to the main production processes, they can be divided into pipe making products and stamping products. Among them, pipe making products are TTU products, and stamping products are BHA, URA and RAIL products.

In 2021, 2022, and 2023, sales revenue of pipe making products and stamping products of Youli Intelligent accounted for over 99% of the company's main operating revenue.

Composition of main business income, source of prospectus.

In terms of financial data, in 2021, 2022, and 2023, Youli Intelligent's operating income was approximately RMB 384 million, RMB 433 million, and RMB 658 million, respectively; the company's net income attributable to shareholders of the parent company over the same period was approximately RMB 14.78 million, RMB 42.19 million, and RMB 78.17 million, respectively.

From January to March 2024, the company achieved operating income of approximately RMB 185 million, an increase of 54.19% year-on-year. During the same period, the net profit attributable to shareholders of the parent company was RMB 28.28 million, an increase of 178.62% year-on-year.

The company's main financial indicators, according to the prospectus

In terms of gross profit margin, in 2021, 2022, and 2023, the company's comprehensive gross profit margin was 7.75%, 18.96%, and 18.49%, respectively. The gross profit margin in 2022 increased compared to 2021, and remained stable between 2022 and 2023. Among them, the gross profit margin in 2021 was lower than the average level of comparable companies; the gross profit margin in 2022 and 2023 was higher than the average level of comparable companies.

It is worth noting that the company's gross profit margin in 2022 rose sharply. Regarding this, the company stated that the main reason was that, after negotiating with the customer NEXTracker, the company adjusted the prices of its products, and the selling prices of the products increased; the prices of raw materials fell during the same period, and the product cost decreased. In addition, the USD-RMB exchange rate rose in 2022, and the proportion of stamping parts with higher gross profit margin increased, which resulted in a significant increase in gross profit margin in 2022.

Comparable companies' gross profit margin comparative analysis, source from the prospectus

In 2021, 2022, and 2023, the company's research and development expenses were RMB 3.92 million, RMB 5.07 million, and RMB 5.83 million, respectively, accounting for 1.02%, 1.17%, and 0.89% of the operating income for the period.

In 2021, 2022, and 2023, the company's research and development expenses were lower than the average level of comparable companies, and were close to Yihua New Energy. The company stated that this was mainly because the sample products developed and produced by the company can be sold after meeting the sales standards, and the related product investment is adjusted from research and development expenses to cost of goods sold.

Meiya Technology stated that compared with Ctrip Group and Tongcheng Travel, the company's R&D cost ratio is lower, mainly because these two comparable companies are both online travel agencies and typical Internet companies, and their investment in technology research and development is higher. In addition, the financial report preparation basis applied by the two comparable companies is different from that of the company, and the collection and accounting standards of the "product research and development expenses" item and the "service development expenses" item disclosed by them may have some differences from the R&D expenses of the company.

Regarding the industry competition pattern, Youli Intelligent stated that the competition in the photovoltaic bracket industry is relatively sufficient, and the competitive pattern is relatively stable. In the field of photovoltaic bracket components, the company's main direct competitors are Yihua New Energy, Suzhou Bojia New Energy Technology Co., Ltd., etc. The company's development history is relatively short, and it has not yet built production bases overseas. There is still a certain gap between the company and the above-mentioned competitors in terms of production scale, product types, and financial strength.

If the company cannot implement effective market development measures, expand market influence, continuously improve its core technology strength and competitiveness, and meet downstream customer requirements in terms of product research and development design capabilities, the company will face risks such as weakened competitiveness caused by intensified market competition, may miss market development opportunities, and may affect the company's development.

High concentration of customers

In 2021, 2022 and 2023, Youli Intelligence's sales to the top five customers accounted for more than 94% of its revenue. Among them, the company's revenue from its largest customer, NEXTracker, accounted for 74.75%, 80.69% and 61.67% of its revenue respectively, indicating high customer concentration.

According to Wood Mackenzie data, NEXTracker's PV tracking bracket shipments ranked first in the world for eight consecutive years from 2015 to 2022. The high customer concentration of the company is reasonable given the current market structure of the PV tracking bracket industry and the company's current product structure. However, there is still a risk of high customer concentration and dependence on a single large customer in the future.

The concentration of the company's customers, as well as comparable companies, is based on the prospectus.

The company also has a relatively high proportion of overseas income. In 2021, 2022 and 2023, the proportion of the company's foreign sales revenue to its main business revenue was 86.15%, 88.19% and 73.06%, respectively. The major regions for foreign exports include Brazil, Chile, Australia, Canada, Europe, the Middle East and other countries and regions.

The company stated that overseas markets are an important growth point for the company's income. If the country of export adopts trade protection policies such as imposing tariffs on products from China, it will directly affect the company's sales to overseas customers.

In addition, the accounts receivable of the company in 2021, 2022 and 2023 were approximately 32.7691 million yuan, 99.508 million yuan and 186 million yuan, respectively, accounting for 15.00%, 40.04% and 39.70% of the total assets.

The company explained that due to the increase in domestic bank credit lines and low loan interest rates, the company borrows from banks to supplement its working capital in order to reduce or defer the discounting of accounts receivable, leading to a certain increase in the amount and proportion of accounts receivable.

It should be noted that the cash flow from the company's operating activities fluctuates greatly. In 2021, 2022 and 2023, the net cash flow from the company's operating activities was 15.9716 million yuan, 21.8899 million yuan and -5.3158 million yuan, respectively.

The company stated that if there are situations such as a decrease in order acquisition, intensified industry competition, and changes in international trade policies in the future, the company may face the risk of fluctuations in operating cash flow.

Epilogue

There are some challenges facing the development of Youli Intelligence, including high customer concentration and risks associated with dependence on a single large customer. Additionally, while overseas markets bring important revenue growth for the company, they also expose the company to potential risks associated with changes in international trade policies.