Source: Wall Street See

The core PCE inflation in the US increased by 2.6% in May, hitting a three-year low. The short-term inflation outlook for US consumers fell, which once suppressed the value of the US dollar and US bond yields, while also raising market bets on a rate cut. However, the S&P 500 index and the Dow Jones Industrial Average both fell after reaching intraday highs, possibly due to Goldman Sachs and JPMorgan Chase bearish on US stocks. Amazon, Google, and Microsoft fell from their record highs, while most chip stocks rose. Nvidia rose by 3% before falling by 0.4%. The AI trend drove the NASDAQ up 18% and the S&P up 14.5% in the first half of the year. Product structure, 10-30 billion yuan products operating income of 401/1288/60 million yuan respectively.

Before the parliamentary elections, French stocks fell 2% to a five-month low, and the yield on the benchmark bond soared 74 basis points in the first half of the year. The market began to price in the possibility of Trump winning the US presidential election, and the US bond yields surged from their double-digit lows. They fell by 12 basis points in June, but rose by 50 basis points in the first half of the year. The US dollar rose for the fourth consecutive week and rose more than 3% in the first half of the year. The yen once fell below 161, hitting a 38-year low, and fell by 12% in the first half of the year, hovering around the seven-month low of 7.30 yuan for offshore RMB.

Oil prices have risen for three consecutive weeks and are approaching their highest level since the end of April. US crude oil rose more than 6% in June, and Brent oil rose more than 12% in the first half of the year. Gold plunged for the first time in four months, but rose by nearly 14% in the first half of the year. Silver rose by nearly 26% this year. In June, London nickel fell by 12%, and aluminum and copper fell by nearly 5%. T in the first half of the year, tin rose more than 29%, and copper rose more than 12%.

The core PCE price index, which is the inflation indicator that the Federal Reserve values the most, grew by 2.6% year-on-year in May, reaching a new low for more than three years since March 2021. The increase was weaker than the previous figure of 2.8%. Other indicators met the market's expectation of cooling inflation.

Traders' bets on a rate cut by the Fed in September are still around 65%, and two rate cuts are expected to occur within the year. The final reading of the University of Michigan's consumer confidence for June rebounded from the initial reading, and the one-year inflation expectation dropped to 3%, which temporarily brought down the US dollar and US bond yields.

However, Bank of America believes that the Fed will cut interest rates for the first time in December, which is in line with the outlook of most Fed officials. This year, the voting member and President of the San Francisco Fed, Daly, said that the PCE data showed that monetary policy is playing a role, and it is now impossible to determine the timing of interest rate cuts.

Morgan Stanley believes that both the Fed and the European Central Bank may cut interest rates in September because key data further indicates that US and Eurozone inflation is cooling down. In June, inflation rates in France and Spain did slow down slightly, while inflation in Italy rose slightly.

The Japanese Ministry of Finance stated that it has not intervened in the foreign exchange market over the past month. The Bank of Japan maintains the size and frequency of bond purchases in July. However, Japan replaced its highest-level official in charge of foreign exchange affairs, and the yen once fell below 161, hitting a 38-year low.

After the US stock market closed, major Wall Street banks including Bank of America, JPMorgan Chase, Morgan Stanley, Citigroup, Wells Fargo & Co, and State Street announced increased preference rewards for shareholders and share buybacks , which had previously passed the stress tests of the Fed.

After reaching intraday highs, the S&P 500 index fell and only the NASDAQ rose throughout the week. The AI trend drove the NASDAQ up by 18% and the S&P up 14.5% in the first half of the year.

Friday, June 28th is the last trading day for the US stock market for the second quarter and the first half of 2024. The US stock market opened high and fell.

During the noon break, the S&P 500 index and the NASDAQ respectively erased their gains of 0.7% and about 1% and turned down. The NASDAQ failed to stabilize above the integer mark of 18,000 and the NASDAQ 100 also rose by 1.2% and turned down after breaking through the 20,000 mark for the first time in history. The Dow Jones Industrial Average rose nearly 280 points or 0.7% at the beginning of the trading day and fell at the end. The Russell small-cap stocks outperformed other indexes.

At the close, both the S&P 500 index and the NASDAQ stopped rising for three consecutive days and fell from their one-week highs, which had approached the historical high set on Tuesday last week. The Dow Jones Industrial Average stopped rising for two consecutive days, and the Russell small-cap stocks rose for two consecutive days to refresh their two-week highs.

The S&P 500 index fell by 22.39 points, or 0.41%, to 5460.48 points. The Dow Jones Industrial Average fell by 45.20 points, or 0.12%, to 39118.86 points. The NASDAQ fell by 126.08 points, or 0.71%, to 17732.60 points.

The NASDAQ 100 fell by 0.5% and rose by 17% in the first half of the year. The NASDAQ Technology Market Value-Weighted Index (NDXTMC), which measures the performance of the NASDAQ 100 technology component stocks, fell by 0.5%. The Russell 2000 small-cap stocks rose by 0.5%, and the "panic index" VIX rose by 1.6% to 12.44.

After hitting a new intraday high, the S&P and Nasdaq both closed lower for the week, with only the Nasdaq up.

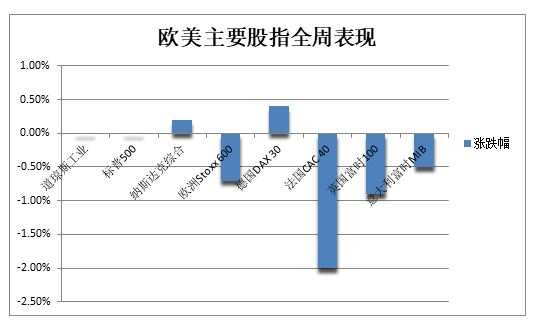

The AI boom has led the tech-heavy Nasdaq to outperform other major indices in the first half of the year, with a cumulative increase of 18%, while the S&P 500 increased by 14.5% and the Nasdaq increased by 3.8%. This is mainly due to the Dow's poor performance in Q2, down 1.7%, while the S&P and Nasdaq rose by 3.9% and 8.3%, respectively.

The AI boom has driven the performance of the S&P and Nasdaq in the first half of the year, while the Dow and small-cap stocks have performed relatively poorly.

Similarly, in June, the Nasdaq led the major stock indexes and rose nearly 6%, while the S&P and Dow Jones rose 3.5% and 1.1%, respectively. This week, the Nasdaq rose 0.2%, while the S&P 500 and Dow Jones both fell by less than 0.1%. Energy and communications services sectors were up more than 2% for the week, leading the large-cap indexes.

Technology, finance, and energy sectors performed the best in the first half of the year, while the real estate sector did not do well.

Bank of America believes that next week's US non-farm employment data is crucial for determining the Fed's policy path. JPMorgan warns that the S&P 500 could fall sharply to 4,200 points by the end of the year, accumulating headwinds, including slowing US economic growth and earnings downgrades.

Star tech stocks declined across the board, but Tesla rebounded 0.2% to its highest level in nearly four months. "Metaverse" Meta fell nearly 3% off its 11-week high, while Amazon fell 2.3% off its all-time high, still with a market capitalization close to $2 trillion. Netflix fell more than 1%, Google A fell 1.8% off its high, Apple fell 1.6% after four consecutive days of gains, with a market capitalization of $3.22 trillion, ranking second in the US stock market, and Microsoft fell 1.3% and stopped at a three-day high with a market capitalization of $3.32 trillion, the largest in the US stock market.

Most chip stocks rose, but after the midday session, the gains narrowed. The Philadelphia Semiconductor Index rose nearly 3% and closed up nearly 1%, off its two-week low, while the industry ETF SOXX closed up 1%. Nvidia rose 3% before slipping 0.4%, falling for the second day in a row. It rose 6.8% on Tuesday and fell 6.7% on Monday, its largest two-month drop, with a market capitalization of $3.1 trillion, placing it third in the US stock market, and its double bullish ETF rose nearly 6% before slipping 0.8%; Broadcom rose more than 1% off its two-week low, Qualcomm rose more than 2% off its five-week low, ARM fell about 2%, Taiwan Semiconductor and Applied Materials rose more than 1%, Lam Research rose nearly 1%, Micron Technology flipped down 0.5%, and both hit new highs last week; Intel rose more than 1%, and AMD rose 1.7%.

Among the seven sisters of the US stock market, Nvidia's semiconductor industry once again led the stock market in the first half of the year, with VanEck Semiconductor ETF SMH up 49%. In the top four holdings, Nvidia soared 149% in the first half of the year, TSMC rose 67%, Broadcom rose nearly 44%, and Qualcomm rose nearly 38%. KLA Corp, ASML Holding, and Lam Research, semiconductor equipment manufacturers, all rose by about 40% in the first half of the year, outperforming the S&P 500.

AI concept stocks are also rising more than falling. CrowdStrike fell more than 1%, Oracle rose 0.7%, both are not far from their new highs. SoundHound.ai fell 1%, BigBear.ai rose 1.7%, C3.ai rose 1.4%, Snowflake rose 0.9% further away from its 17-month low, Palantir rose 0.4%, Adobe rose 1.6%, Dell fell 1%, Super Micro Computer fell about 8%, and IBM rose more than 1%.

In terms of market performance, the semiconductor industry led by Nvidia has once again outperformed the stock market in the first half of the year, with VanEck Semiconductor ETF SMH up 49%. In the top four holdings, Nvidia soared 149% in the first half of the year, TSMC rose 67%, Broadcom rose nearly 44%, and Qualcomm rose nearly 38%. KLA Corp, ASML Holding, and Lam Research, semiconductor equipment manufacturers, all rose by about 40% in the first half of the year, outperforming the S&P 500.

In terms of stock market performance, the semiconductor industry led by Nvidia once again outperformed the stock market in the first half of the year. The VanEck Semiconductor ETF SMH has risen by 49%. Among the top four holdings, Nvidia soared by 149% in the first half of the year, Taiwan Semiconductor rose by 67%, Broadcom rose nearly 44%, and Qualcomm rose nearly 38%. KLA Corp, ASML Holding, Lam Research and other semiconductor equipment manufacturers also rose by about 40% in the first half of the year, outpacing the S&P 500 index.

Among the Dow components, software giant Salesforce fell a cumulative 14.6% in the second quarter, Disney fell more than 18%, Caterpillar fell 9%, and Intel had the worst quarter with a nearly 30% decline. Apple had the best quarter with a nearly 23% increase, while Boeing fell 5.6% in the quarter and 30% in the first half of the year.

In addition, Supermicro Computer rose 188% in the first half of the year, performing the best among the S&P 500 components, followed closely by Nvidia. Micron Technology rose 54% in the first half of the year, and Eli Lilly and Co., which is expected to soon receive approval for an Alzheimer's drug, rose 55%. Walgreens fell nearly 54% and was the worst performer.

Chinese concept stocks continued to sell off. The KraneShares CSI China Internet ETF (KWEB) fell 0.7%, the KraneShares China Technology ETF (CQQQ) erased its 0.5% gain and fell slightly, and the Nasdaq Golden Dragon China Index (HXC) fell 1%, breaking through the 5800 point mark and falling for the eighth of the past ten trading days to the lowest level in nearly five months. For the week, it fell 2.8%, for June, over 9%, for the second quarter, over 6%, and for the first half of the year, 11.3%.

Among the popular stocks, JD.com fell 1.6%, Baidu fell 0.6%, and PDD Holdings rose 0.8%. Alibaba and Tencent ADRs fell 0.5%, Bilibili fell more than 3%, and Nio Inc. and XPeng Inc. fell 5.4%, Li Auto Inc. fell 2.5%, and Kanzhun Ltd. fell 6.6%.

Other stocks with significant changes include:

Sportswear and apparel giant Nike fell nearly 20%, the largest drop since 2001 and the lowest in over four years. Its year-to-date decline exceeded 30%, and its fourth-quarter revenue was lower than expected, prompting mainstream investment banks to withdraw their buy ratings.

Trump Media & Technology Group (DJT) opened 8.7% higher, then fell nearly 11% as Biden stuttered, was confused in his thinking, and made repeated mistakes in the presidential debate with Trump. Analysts doubt him, and Trump is said to have lied during the debate.

In the debate, the issue of medical prices was raised, and most U.S. healthcare stocks rose on Friday. The S&P 500 managed healthcare index rose 3.6% at one point, its largest one-month increase in a month. UnitedHealth Group rose 4.7%, and Humana Inc. rose more than 7%. Some institutions said that the healthcare industry may be entering a more friendly regulatory environment.

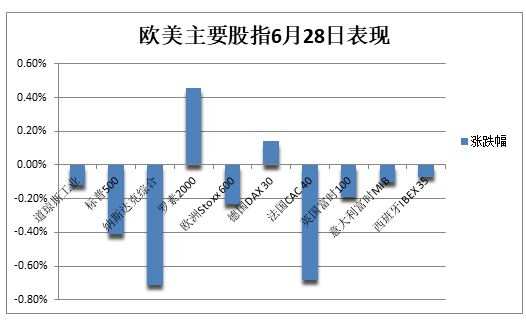

European stocks fell for a second consecutive day, with only the German stock index rising, while the French stock index fell by about 2% to a five-month low for the week. The pan-European Stoxx 600 Index fell 0.23%, falling for four consecutive days to a two-week low, falling 0.7% for the week, accumulating a 1.3% decline in June and a 6.77% increase in the first half of the year. The EuroSTOXX 50 index fell more than 1.8% in June and rose more than 8.24% in the first half of the year.

European and American bond yields rebounded in a V-shape on Friday after a double-digit percentage increase in the first half of the year. The yield on U.S. bonds fell 12 basis points in June.

Short-term U.S. bond yields fell to a daily low after PCE inflation cooled, then rebounded and rose during U.S. post-market trading amid speculation that the bond market may be pricing in the possibility of Trump winning the U.S. presidential election.

The two-year U.S. bond yield, which is more sensitive to monetary policy, fell the deepest, down 5 basis points to 4.66%, before rebounding to above 4.75% after turning higher from the daily low by more than 9 basis points. The 10-year benchmark bond yield briefly fell nearly 3 basis points to 4.26%, then rebounded to rise above 4.40%, hitting a new high for over two weeks, and rebounding by more than 14 basis points from the daily low, after falling to a 10-week low since early April a little more than a week ago.

In June, the yields on both the two-year and 10-year U.S. Treasuries fell by about 12 basis points, as soft economic data boosted expectations of a rate cut and U.S. Treasuries posted their largest monthly gain since 2024. However, some analysts believe that due to the worsening problem of U.S. Treasury supply and fiscal deficits, U.S. Treasury yields may rise again in the second half of this year. The yields on two-year and 10-year U.S. Treasuries both rose by about 50 basis points in the first half of the year.

The yield on Germany's 10-year benchmark bond rose 5 basis points in Friday's close to 2.5%, falling 14 basis points in June and rising nearly 48 basis points in the first half of the year. The yield on France's 10-year bond rose 3 basis points on Friday, rising more than 17 basis points in June and nearly 74 basis points in the first half of the year. The yield on Britain's 10-year bond rose 4 basis points on Friday, falling more than 17 basis points in June and rising more than 63 basis points in the first half of the year.

The first round of voting for the French parliamentary elections will be held on Sunday. Investors expect a new government led by an alliance of far-right or far-left parties to increase fiscal spending and require the risk premium demanded by holders of French bonds, that is, the spread between French and German bond yields, to rise to 84 basis points, the highest since 2012. Some analysts say that if President Macron resigns, the spread could rapidly expand to 135 basis points.

Oil prices have hovered at their highest level since the end of April and have risen for three consecutive weeks, with an average increase of over 12% in the first half of the year. In terms of product structure, the operating income of products worth 10-30 billion yuan is 4.01/12.88/0.06 billion yuan respectively.

Oil prices are still hovering at their nine-week high since the end of April. WTI August crude oil futures fell 0.20 USD, down more than 0.24%, to 81.54 USD/barrel. Brent August futures, which expire on Friday, rose 0.02 USD, up more than 0.02%, to 86.41 USD/barrel.

American WTI crude oil rose by about 1 USD or 1.2% during regular trading hours and reached its highest level since April 30 at 82.72 USD/barrel. The more active international Brent September futures rose 0.92 USD or 1.1% at one point, briefly breaking through the 86 USD integer mark, but fell in the end-of-day trading session.

Both oil prices have risen for three consecutive weeks this week, with US oil up 1% and Brent up 1.4%. US oil rose 6.3% in June and 13.7% in the first half of the year, while Brent rose 4.8% in June and over 12% in the first half of the year.

The main reason for the rise in oil prices this week is the market's concern that military conflict between Israel and Lebanon will break out, thus causing confrontation with Iran and disrupting the supply of crude oil in the Middle East. Barclays predicts that Brent oil will remain around $90 a barrel in the coming months.

The European benchmark TTF Dutch natural gas futures and ICE UK futures both fell more than 1% in the end-of-day trading session, hovering at a two-week low for two weeks. The US natural gas contract for August fell more than 3% and once fell below $2.60, the lowest level this month, and turned negative for the year. US gasoline futures have risen 20% this year.

The USD has risen for four consecutive weeks and more than 3% in the first half of the year. The yen once fell below 161, the lowest level in 38 years, and fell by 12% in the first half of the year.

The DXY, which measures the USD against six major currencies, fell the deepest on Friday, down 0.2%, and remained below the 106 mark, further away from the eight-week high since May 1. It rose slightly for the whole week and rose for four consecutive weeks. It rose 1.2% in June, 1.3% in the second quarter, and 3.4% in the first half of the year.

The euro rose 0.2% against the USD on Friday and remained above 1.07, further away from the lowest level since May 1. However, it fell more than 1% in June, the largest monthly decline since January, dragged down by political turmoil in France's early parliamentary elections, and fell 0.7% in the second quarter.

Sterling rose slightly against the USD on Friday, continuing to move away from its six-week low since mid-May, and was flat this week after three consecutive weeks of decline. The offshore RMB rose slightly during regular trading hours and rose above 7.30 yuan, but still hovered at its lowest level in seven months, falling 0.5% in June and 1.8% in the first half of the year.

The yen against the USD fell through the 161 mark in the Asian market on Friday, refreshing a new low since 1986 for the thirty-eighth year. The fall in US stocks narrowed and rebounded to the 160.80 line, down nearly 2% in June and nearly 6% in the second quarter, the worst performing currency among major currencies. Yen against the euro also hit a new low on Friday, with Tokyo's core inflation accelerating in June, but having little support for the yen.

Mainstream cryptocurrencies have fallen back. The market's largest market capitalization leader, Bitcoin, fell more than 1% and fell below $61,000, breaking through the psychological integer mark of $60,000 for the first time since May 3 on Monday, and once fell below $59,000, the lowest level in nearly eight weeks since May 1. The second-largest Ethereum fell 2% and lost $3,400, approaching a five-week low since mid-May.

Gold had the first cumulative monthly decline in four months, with London nickel falling 12% and aluminum falling nearly 5%, while tin rose more than 29% and copper rose more than 12% in the first half of the year.

COMEX August gold futures rose 0.1% to $2,337.70/ounce at the end of Friday's session, while COMEX July silver futures rose 0.8% to $29.475/ounce. Spot silver rose back above $29 this week, falling more than 1% and 4% in June, and rising nearly 26% in the first half of the year.

Spot gold rose 0.5% before pre-market trading in the United States and approached the integer position of $2340. At the end of the US stock market, the gains were wiped out and fell slightly to less than $2330. It fell below $2300 on Wednesday to a three-week low. It rose 0.3% this week, the second week of rising in three weeks. It fell slightly in June, the first monthly decline in four months. It rose more than 4% in the second quarter and has risen for three consecutive quarters. It rose 13.7% in the first half of the year.

London industrial metals rose together on Friday due to the weakening of the US dollar. Dr. Copper, the economic bellwether, increased $84 or 0.9% to nearly $9600, breaking away from the ten-week low since mid-April. London aluminum rose 1.3%, back above $2500 and out of the two-month low. London zinc rose slightly, London lead rose 2%, London nickel rose 1%, and London tin rose 1.6%, breaking away from the lowest level since early April.

London copper fell 4.7% in June, but rose more than 12% in the first half of the year. London aluminum fell nearly 5% in June and rose 5.7% in the first half of the year. London zinc fell 1.6% in June and rose more than 10% in the first half of the year. London lead rose 2.2% in June and rose 7.6% in the first half of the year. London nickel fell by about 12% in June and rose 4% in the first half of the year. London tin rose 0.4% in June and rose for the seventh consecutive month, rising more than 29% in the first half of the year.

US corn futures fell more than 2.8% on Friday, and fell 9.7% in June. The expected corn planting area of the US Department of Agriculture (USDA) exceeded market expectations. The Bloomberg Commodity Grains Index fell below a three-and-a-half-year low and fell more than 11% in June. Chicago SRW wheat fell more than 18% in June, and soybean fell by about 7%.

Editor / jayden