Even if Micron turns in a 'slightly above average' report, it still cannot meet investors' expectations. This has also caused the company's stock price to fall nearly 8% after-hours. Additionally, this financial report also shows two major growth constraints that Micron currently faces: on the one hand, HBM chip production capacity is difficult to further boost in the short term; at the same time, chip demand in traditional markets such as PCs and smart phones remains sluggish.

On June 27, Cailian Press reported (editor Liu Rui) that while global investors are watching Nvidia's shareholders' meeting, Micron, the largest storage chip manufacturer in the United States, also released its third quarter earnings report after the market close on Wednesday.

Although Micron's performance in the third quarter and guidance for the fourth quarter were better than expected, given Micron's stock price has risen by more than 67% in the year, the market expects Micron to deliver an "extremely outstanding" earnings report and guidance.

Therefore, even if Micron submitted a "slightly above average" report card, it still failed to meet investors' expectations. This also caused the company's share price to plummet nearly 8% after hours.

Micron's share price plummeted after the market close.

In addition, this report also showed that Micron is currently facing two major growth bottlenecks: on the one hand, although Micron has received a boost from the artificial intelligence computing boom, the short-term capacity of HBM chips is difficult to further boost. At the same time, in traditional markets such as PCs and smartphones, chip demand is still depressed.

Did not meet the super high market expectations.

The report showed that in the third quarter ending on May 30th,

Micron's adjusted revenue grew 82% to 6.81 billion US dollars, better than analysts' expected 6.67 billion US dollars;

Excluding certain items, Micron's earnings per share were 62 cents, also better than analysts' expected earnings of 50 cents per share.

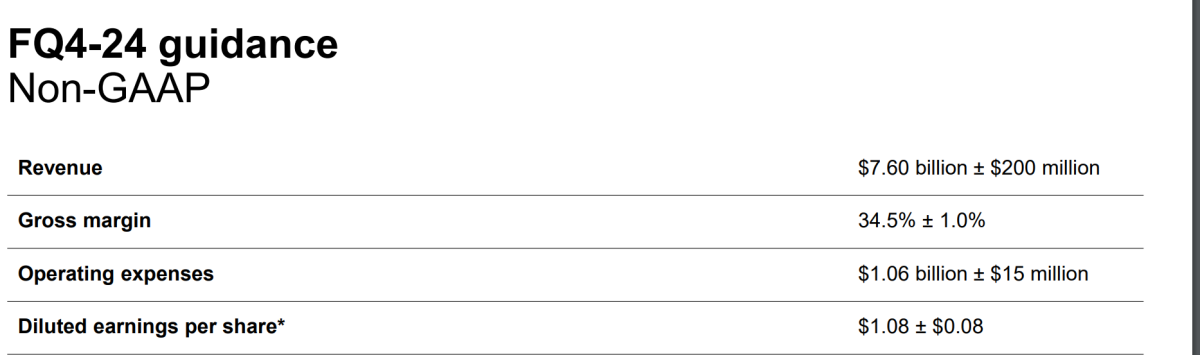

In the guidance section, Micron expects that in the fourth quarter ending in August,

The company's revenue will reach 7.4 billion to 7.8 billion US dollars. Although the median expected value of 7.6 billion US dollars is slightly better than analysts' average estimate of 7.58 billion US dollars, it still failed to meet the market's super high expectations - especially some analysts originally expected Micron to give a figure of more than 8 billion US dollars, but now this expectation has not been met.

At the same time, Micron expects earnings per share of about $1.08 in the fourth quarter, which is only slightly better than the market's expected $1.02.

As of press time, Micron's stock fell 7.98% in after-hours trading. So far this year, Micron's stock price has cumulatively increased by 67%, indicating investors' super high expected value.

Micron's stock has risen by more than 67% during the year.

HBM chip capacity has been difficult to further boost.

In the wave of artificial intelligence, Micron's HBM chip data is particularly noteworthy. The financial report showed that in the third quarter, Micron's HBM3e chip revenue reached 100 million U.S. dollars, and is expected to increase to "hundreds of millions of U.S. dollars" in the fourth quarter. Micron also expects that by the fiscal year 2025, this number will increase to "several billion U.S. dollars".

Micron also revealed that its HBM chip orders have been booked through 2025. As an HBM supplier for major clients such as Nvidia, increasing HBM production has always been the most important challenge facing Micron amid strong demand for artificial intelligence.

Manish Bhatia, Executive Vice President of Global Operations at Micron, said in an interview that due to difficulties in increasing factory output and making chips compatible with systems, HBM supply growth has actually "hit the brakes."

Given these constraints, the company expects HBM prices to steadily rise.

Micron has already planned to invest about 8 billion dollars in new factories and equipment in the 2024 fiscal year to support the construction of its factories in Idaho and New York. However, Micron disclosed that the Idaho factory will not contribute to the expansion of supply until the 2027 fiscal year, and the New York factory will not be put into use until 2028.

Traditional chip demand is still sluggish.

Compared with the hot demand for HBM chips, Micron's traditional business areas, the PC and smart phone markets, are much more sluggish.

Micron CEO Sanjay Mehrotra emphasized in the financial report that the smartphone and personal computer markets are still sluggish.

Micron stated that by 2024, PC sales are still expected to grow by low single-digit percentages (about 1% to 4%). Smartphone sales will grow by low to mid-single-digit percentages (about 1% to 7%).

However, the company expects AI functionality to help stimulate demand for smartphones and personal computers by 2025.

Micron CEO Sanjay Mehrotra reiterated that 2024 will mark the rebound of the storage chip industry, and 2025 will set a sales record.