Fed's hawkish tone - rate hikes will be supported if inflation does not continue to improve; Canada's May CPI accelerated and obstructed the country's central bank from cutting rates in July; US stocks saw mixed performance with Dow falling nearly 300 points, its first decline in six days; Nvidia's market cap rose above $3.1 trillion and chip stocks rebounded significantly by 1.8%; positive financial results caused FedEx's stock to rise 15% after hours, and investment from Volkswagen boosted Rivian's stock by 46%. The Chinese concept stock index fell 1.3% to the lowest level in nearly ten weeks, but Xpeng turned upward by 1% and Li Auto slightly rebounded after falling more than 2%.

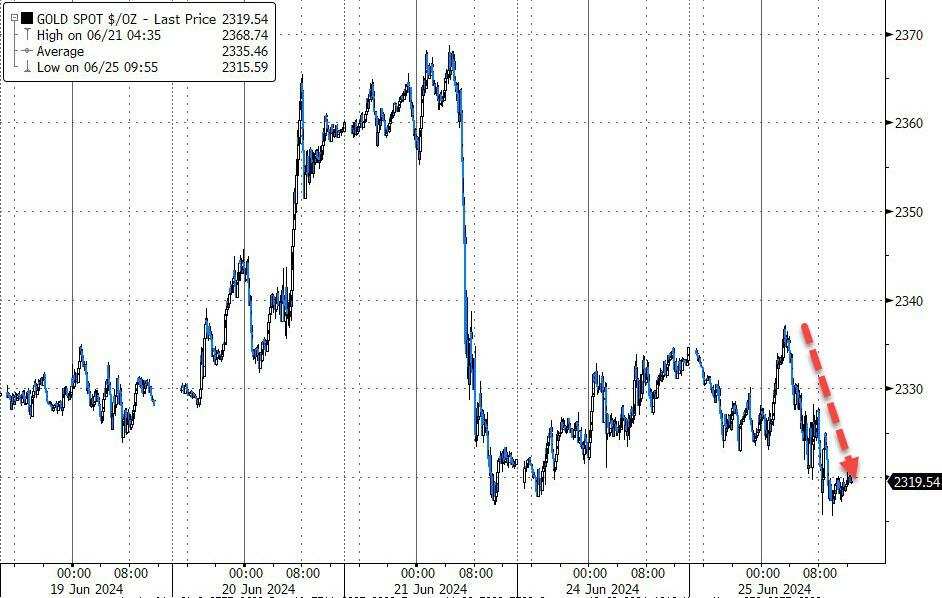

US Treasury yields erased most of the intraday gains, the US dollar rose, the Japanese yen has been pressuring 160 for several consecutive days, offshore RMB hovered at a seven-month low, and Bitcoin rose above $62,000. Oil prices fell 1%, with WTI crude oil falling below $81 and Brent crude oil dropping to $85, which is off the eight-week high. Spot gold fell below $2,320 to a one-week low, and copper on the London Metal Exchange hit a ten-week low, while New York cocoa futures fell by another 10%.

FOMC voting member and Federal Reserve Governor Bowman said that if inflation does not continue to improve, she would be willing to support raising interest rates. Now is not the right time to begin cutting interest rates. There are multiple upside risks to the inflation outlook, and there is no expectation of any rate cuts in 2024.

Some analysts say that several Fed officials have said they need to wait for "a while" and more inflation-cooling data before they can discuss easing. Daly, the president of the San Francisco Fed and a voting member this year, refused to lower rates proactively to counter deteriorating labor market conditions and economic slowdowns.

However, another voting member and Fed Governor Lael Brainard stated on Tuesday that "at some point" a rate cut would be appropriate because risks to employment and inflation targets are more balanced, and inflation is expected to slow more sharply in 2025.

In June, the US Conference Board Consumer Confidence, Present Situation and Expectations Indexes all declined, and the proportion of respondents who expected business conditions to improve in the next six months fell to the lowest level since 2011. The S&P CoreLogic Case-Shiller US National Home Price NSA Index for April has cooled from its high.

After four consecutive months of easing pressure, Canada's May CPI inflation rate accelerated again to a year-on-year rate of 2.9%, posing an obstacle to the Bank of Canada's rate cut in July, and short-term USD/CAD fell more than 40 points. In addition, the market still expects the Fed to cut interest rates twice this year.

FedEx's annual profit outlook exceeded expectations due to deep cost reductions, and stock prices rose 15% in after-hours trading. Some analysts say its financial report is usually a leading indicator of the US economy. "Tesla rival" Rivian received $5 billion in investment from Volkswagen in Germany, and its stock price rose 46% in after-hours trading.

The S&P and NASDAQ both closed lower for three consecutive days, while the Dow fell for the first time in six days. Google and Microsoft reached new highs, while Nvidia rebounded 6.8%.

On Tuesday, June 25, the US stock indexes continued to diverge, with the Dow opening low and falling throughout the day. At its lowest point, it fell more than 410 points or 1% and temporarily lost the integer level of 39,000 for the first time. Walmart's component stock fell 3.4% at one point, breaking away from its historical high and posting its largest two-month decline in two months. The Philadelphia Fed index fell more than 1.2%. The S&P 500 and NASDAQ indexes opened high and rose with the help of chip stocks such as Nvidia, with the NASDAQ and chip stock indexes both up more than 1%. The US tech stock index ETF and biotech stock index ETF were among the biggest gainers.

At the close, the S&P 500, NASDAQ, and NASDAQ 100 all closed lower for three consecutive days, with the S&P breaking out of its one-week low and the NASDAQ breaking out of its two-week low. The Dow stopped its five-day winning streak and fell from its recent five-week high:

The S&P 500 rose 21.43 points, or 0.39%, to 5,469.30, while the Dow fell 299.05 points, or 0.76%, to 39,112.16. The NASDAQ rose 220.84 points, or 1.26%, to 17,717.65.

The NASDAQ 100 rose 1.2%, while the Nasdaq tech market cap-weighted index (NDXTMC), which measures the performance of Nasdaq 100 tech industry stocks, rose 1.8%, both of which had been off their highs for three consecutive days. The Russell 2000 small-cap stock index fell 0.4%, while the "panic index" VIX fell more than 3% and fell below 13.

JPMorgan's chief market strategist Marko Kolanovic warned that while low inflation data is sparking hopes of rate cuts, it also suggests that economic growth is cause for concern and may be one of the major risks facing financial markets in the next stage. The strategist for Bank of New York Mellon also said that unless the economic data continued to be weak, the stock market gains would be unsustainable unless the possibility of a rate cut by the Fed in September increased.

The star technology stocks all rose. "Metaverse" Meta rose to a more than ten-week high, Google A rose 2.7% to a new all-time high, Amazon rose 0.4% and approached a six-week high, Tesla rose 2.6%, Netflix rose 0.5% to break away from a one-week low, and Apple rose 0.5% for the second consecutive day, with a market cap of $3.21 trillion, ranking second in the US stock market. Microsoft rose 0.7% to a new all-time high, with a market cap of $3.35 trillion, the largest in the US stock market.

After a significant three-day correction, chip stocks rebounded. The PHLX Semiconductor Index rose 1.8%, and the industry ETF SOXX rose 1.5%, both out of the two-week low. Nvidia rose 6.8%, ending its three-day decline to exit a three-week low. It fell 6.7% yesterday, the largest drop in two months, and its market value rose back above $3.1 trillion, ranking third in the US stock market. Its double-long ETF rose nearly 14%. However, Broadcom fell 0.7% and has fallen from its peak for five consecutive days. Qualcomm rose 0.7%, ARM rose more than 6%, Taiwan Semiconductor's US stocks and Lam Research rose 2.8%, Applied Materials rose 1.9%, and Micron Technology turned up 1.5%, all of which had previously fallen for three consecutive days from new highs. Intel rose 0.6%, and AMD was flat after falling 2.4%.

Most AI concept stocks rose and few fell. CrowdStrike rose 2.3%, having previously fallen from a new high for four days. Oracle fell 0.5%, having continuously fallen from a new high for four days. SoundHound.ai fell 1.5%, and BigBear.ai rose more than 6%. C3.ai fell more than 1%, and Snowflake fell 0.5%, hitting a 17-month low again. Palantir rose 1.7%, Adobe rose 0.5%, Dell rose 2%, Super Micro Computer rose about 2%, IBM fell 1.4%.

Recent selling that caused Nvidia's market value to evaporate by $430 billion has temporarily paused, and traders are looking for a bottom on the chart. Ari Wald, head of technical analysis at Oppenheimer, said that the long-term trend remains strong, with the stock price far above the 50-day moving average of $101 and the 100-day moving average of $92. Bank of America reiterated a 'buy' rating for Nvidia and included it on its best stocks list. The EU accused Microsoft of 'abusing' its dominant position by bundling popular productivity applications in Teams and Office 365, violating antitrust rules. Goldman Sachs reiterated its 'buy' rating for Microsoft and is bullish on the excellent returns produced by investment-generated AI. Evercore ISI reiterated its 'buy' rating for Apple and is optimistic about the potential increase in iPhone revenue. Wells Fargo reiterated its 'reduce' rating for Tesla and expects the quarterly deliveries to be lower than 400,000 electric vehicles. Royal Bank of Canada lowered its second-quarter delivery expectations for Tesla by 23% to 410,000. Eli Lilly and Co.'s stock price hit a new high after reaching a collaboration with OpenAI.

Chinese concept stocks fell back. The ETF KWEB fell 1.4%, CQQQ fell 1.9%, and the Nasdaq Golden Dragon China Index (HXC) fell 1.3%, coming close to 5,900 points, falling for the sixth day in seven trading days, and returned to a nearly ten-week low.

Most of the popular stocks fell, with Bilibili down nearly 3%, JD.com down 2.8%, Baidu down 0.2%, PDD down 1%. Alibaba fell 1.3%, Tencent ADR fell 0.8%, B Station fell by about 3%, NIO fell 1.6%, Xpeng turned upward 1%, Li Auto slightly rebounded after falling more than 2%, and Faraday Future fell 19% to a new six-week low after a 33% decline. The board of directors approved a reverse stock split. BYD ADR fell nearly 1%.

On the news side, Baidu's Wenxin flagship model is now free for the first time, and Tongyi Qianwen has announced an OpenAI user migration plan. Berkshire Hathaway once again reduced its holdings of BYD, and its position dropped to 5.99%.

Other stocks with significant changes include:

Carnival Cruises rose 8.7% to a nearly six-month high. It unexpectedly turned a profit in the second quarter and revenue exceeded expectations. It raised its annual profit forecast and stated that leisure demand in 2025 will be stronger than this year, and travel prices will rise.

Photovoltaic module power optimizer company SolarEdge Technologies fell more than 20% to a seven-year low and will privately place $300 million in convertible preferred bonds with a maturity date of 2029. A customer who owes the company $11.4 million has filed for bankruptcy.

European stock Novo Nordisk rose 4%, hitting an all-time high with its US shares. Its semaglutide was approved in China for long-term weight management, achieving an average weight loss of 17%. Weight-loss drug concept Zealand rose 9.5%, driving the Danish stock index up 2.7% to a new high.

European stock Airbus fell more than 12% and then more than 9%. Its US stocks fell more than 6% and then 1.8%, hitting the lowest level in seven months. It lowered its EBIT profit target and commercial aircraft delivery volume expectations for 2024, facing a continuous supply chain problem and an additional cost of 900 million euros in the space systems sector.

European stocks fell, led by German stocks. The pan-European Stoxx 600 Index fell 0.23%, the third day in seven days, with technology and industrial sectors falling more than 1%, leading the decline. The Stoxx Europe Aerospace and Defense Index fell by as much as 5%, the biggest drop since November 2021.

In the late afternoon, US bond yields basically wiped out small gains during the day, and short-term Eurozone bond yields rose relatively more.

Waiting for the heavyweight inflation data on Friday, US bond yields rose slightly and then fell again.

During trading, the US Treasury Department issued $69 billion in two-year Treasury bonds, with a winning yield of 4.706% (down from 4.917% on May 28th) and a bid-to-cover ratio of 2.75 (up from 2.41 in the previous auction). At the time, the US bond yield was still hovering near a daily high, and some analysts believe that Wednesday's $70 billion five-year US bond auction will further illustrate potential demand trends.

The two-year US Treasury bond yield, which is more sensitive to monetary policy, briefly rose 2 basis points and approached 4.76%, erasing most of its gains in the US stock market in the closing bell. The 10-year Treasury bond yield rose by more than 1 basis point to 4.26%, and the US stocks closed down to 4.24%. More than a week ago, the US bond yield had fallen to the lowest level in ten weeks since early April.

The benchmark 10-year German bond yield in the Eurozone fell slightly to 2.41%, while the two-year yield rose slightly. The yield on 10-year UK bonds fell slightly, while the yield on two-year bonds rose more than 2 basis points, following data showing unexpected acceleration in Canadian inflation.

Oil prices fell by 1%, with WTI crude oil falling below $81 and Brent crude oil falling below $85, down from the eight-week high.

Oil prices rose and then fell. WTI crude oil futures for August fell $0.80, or more than 0.99%, to $80.83 per barrel, after hitting their highest level since the end of April last week. Brent crude oil futures for August fell $1, or more than 1.16%, to $85.01 per barrel, down from the eight-week high it hit yesterday when it rose above $86 for the first time since April 30th.

WTI crude oil, the more active contract, fell the deepest, down $0.91 or more than 1%, breaching the $81 integer level. Last week, it posted three consecutive trading sessions of seven-week highs. Trading of the more active international Brent September futures contract fell more than $1 or 1.2%, breached $85 and approached $84.

With the tension escalating between Israel and Lebanon on the border, and mainstream investment banks such as Goldman Sachs, JPMorgan, and Citigroup bullish on the fuel demand brought by the peak summer season and indoor cooling, US crude oil and Brent crude oil have respectively accumulated gains of 4.9% and 4.1% in June. This reverses the weakness just after OPEC+ announced its decision to increase production at the end of the year.

Some analysts believe that the combination of geopolitical risks and bullish fundamentals may bring further upward pressure if Brent crude oil breaks through $85 per barrel. However, some warn that if US crude oil falls below $81 per barrel, the momentum may fade and funds may start to clear their long positions.

European benchmark TTF Dutch natural gas futures rose nearly 3% at one point, leaving a two-week low, and ICE British futures rose more than 2% in the closing bell. The August contract for US natural gas fell by 3% and fell back to a two-week low, up about 11% for the year. US gasoline futures have risen 19% year to date.

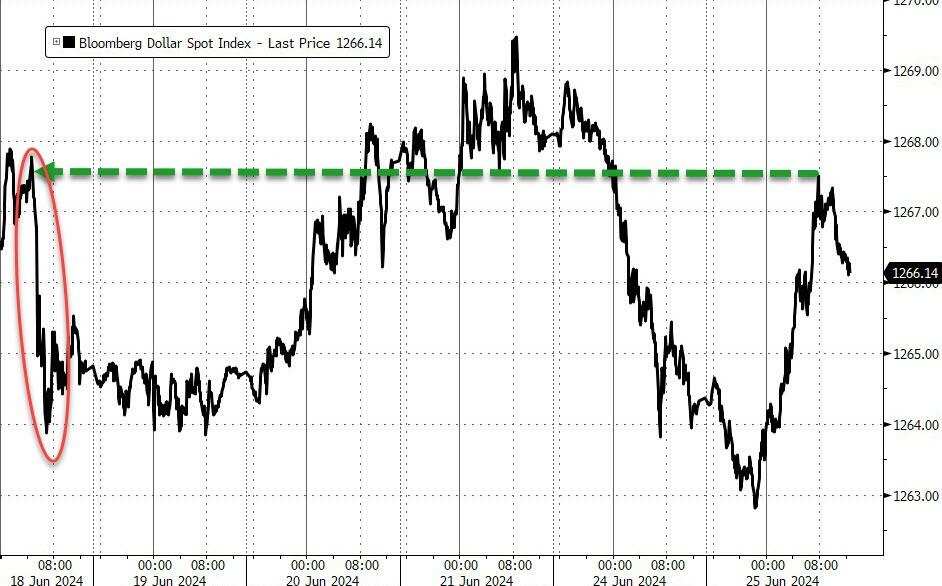

The dollar rose, and the yen approached 160 for many days, while the offshore RMB hovered at a seven-month low, and bitcoin rose above $62,000.

The DXY, which measures the dollar against six major currencies, rose as high as 0.3% and approached 105.80, rising above 105.90 last Friday to a seven-week high since May 1st, and rose for three consecutive weeks, accumulating 0.2% for the entire week.

The euro fell 0.2% against the dollar and briefly lost 1.07, approaching a seven-week low since the end of April, and fell 1% in June. The British pound rose slightly but was still below 1.27, and slightly bounced back to the lowest level in five weeks since mid-May. The offshore RMB against the dollar fell to a daily low in the initial stage of US stocks, briefly losing 7.29 yuan, and then narrowed its decline, still hovering at a seven-month low.

The yen against the dollar briefly fell to 159.79 and attempted to approach the psychological integer of 160 for many days, and the US stock market fluctuated at 159.70 in the afternoon, still hovering at the lowest level in nearly eight weeks since April 29th, which is the lowest level in 34 years.

Market speculation is that 160 is the warning line for the Japanese government to intervene in the foreign exchange market. The huge interest rate gap between Japan and the United States has caused the yen to fall by 1.5% in June and more than 10% against the US dollar this year. On Monday, the yen against the euro hit a record low of 171.49, and against the pound, it hovered at a 16-year low of 202.33.

Mainstream cryptocurrencies rebounded collectively, ending multiple days of declines. The largest market capitalization of bitcoin rose by 3% and rose above $62,000. Yesterday, it fell 7% in the closing bell, falling below the psychological integer of $60,000, and even fell below $59,000, hitting the lowest level in nearly eight weeks since May 1st. The second largest Ethereum rose more than 1% on Tuesday and rose above $3,400, leaving a five-week low since mid-May.

Spot gold fell below $2,320 to a one-week low, London copper hit a 10-week low, and New York cocoa futures fell by another 10%.

The rise in the US dollar and US bond yields has put pressure on the prices of precious metals. COMEX August gold futures fell 0.6% to $2330.90/ounce at the end of the session, while COMEX July silver futures fell 2.1% to $28.905/ounce at the close.

Spot gold fell by nearly $19 or 0.8% during the day, breaking through the integer level of $2320 and hit a one-week low. Last week, it almost hit a two-week high of $2370, but it fell sharply during Friday's trading and turned negative for the week. The gold price has fallen more than 5% from the record high of around $2450 set on May 20. Spot silver fell the most during the interday, down 2.5% and breaking through $29 to a six-week low.

The rise in the US dollar led to a majority of London's industrial metals falling. The Copper Doctor, an economic benchmark, fell $90 or 0.9%, breaking through the integer level of $9600 and hitting a ten-week low since mid-April. London aluminium fell slightly below $2500, still hovering at a two-month low. London zinc rose 0.9%, and London lead rose over 1%. London nickel fell 0.9%, hitting a twelve-week low since early April. London tin fell 1.5%.

New York cocoa futures fell another 10%, hitting a one-month low. Some analysts are concerned that the record high prices will damage demand, as next month's global report for the second quarter is released. Cocoa prices have risen by 88% this year and are expected to have the best performance since 1980.

Edited by Jeffrey