Already laid flat long ago.

Since the release of the New National Nine Articles more than two months ago, the forced delisting standards have become stricter, accelerating the clearing of a large number of junk companies that have taken advantage of the concept to harvest stockholders. The number of problem stocks targeted for delisting this year has reached nearly the same level as last year.

One of the companies has claimed to be a leading player in photovoltaic cell technology before being ST'ed. Unexpectedly, it has been plunging into huge losses continuously. The company has been chased after debt everywhere, and shareholders have been questioning the fact that the actual controller of the company has been constantly reducing holdings and cashing out on stocks while publicly claiming that the company would not be ST'ed.

The company that has put 280,000 shareholders in an uproar is ST Akcome, which has recently been trending online.

The company that has put 280,000 shareholders in an uproar is ST Akcome, which has recently been trending online.

01

Delisting is a sure thing.

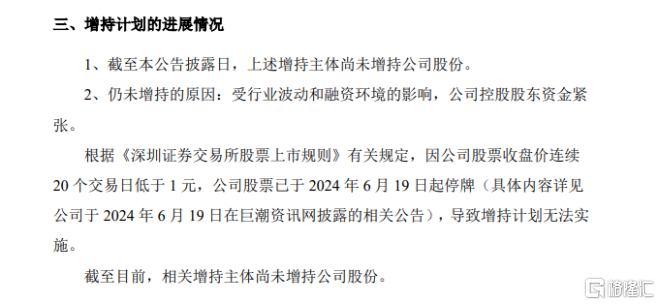

Two announcements on June 22 put Akcome New Energy Technology on the cross of delisting.

The company received a pre-disclosure letter issued by the Shenzhen Stock Exchange. The stock price fell below 1 yuan for twenty consecutive trading days from May 21, 2024 to June 18, 2024, reaching the circumstances where the stock should be terminated from listing. The Shenzhen Stock Exchange plans to terminate the stock trading of the company.

The other notice concerned the progress of the plan to increase holdings of shares by the controlling shareholder and its affiliates.

The controlling shareholder, Akcome Industrial, and its affiliated companies plan to increase their holdings of the company's shares within six months starting from February 27, 2024, with a proposed amount of 100-200 million yuan and a maximum purchase price of 3.5 yuan per share. However, half a year has passed, and the related subjects have yet to increase their holdings of any shares in the company. The reason is simple: a lack of funds.

However, the road to delisting is not easy at all.

Company announcement

Akcome New Energy Technology was established in 2006, headquartered in Hangzhou, Zhejiang Province. The company was originally engaged in PV aluminum frame and PV power station construction and operation, and was listed in 2011. In 2016, the company's business layout extended to battery components, and its production capacity began to accumulate, making it a well-known component supplier in the industry.

The turning point of the company's market capitalization started in 2020. When the Perc battery dominated the industry, the company announced the successful trial production of the N-type heterojunction battery. This is a new type of battery that is believed to be one of the leading ones among many mainstream battery routes with a higher power efficiency than Perc and TopCon.

The company claims that Akcome New Energy Technology is in the first tier of domestic heterojunction solar cell mass production efficiency and is one of the world's top three heterojunction cell leaders. The average conversion efficiency of heterojunction cells in the production base has reached 25.5%, and the double-sided rate has achieved 95%.

Relying on PV's beta and the company's own differentiated positioning, the peak market capitalization of Akcome New Energy Technology once reached as high as 27.5 billion yuan.

However, the cost of research and development, material investment and production is relatively high without scale support, especially in the current tightening financing environment, which makes it a bottomless pit of burning money. When the company started producing batteries, the photovoltaic industry was already entering a cold winter, and the comparative advantage of heterojunction cells over other routes was not significant. This completely arranged the storyline. In 2023, the company lost more than 800 million yuan, marking three consecutive years of losses and accumulated losses of more than 2 billion yuan. Therefore, it was labeled with "ST". Its first-quarter results this year have continued to deteriorate.

On the asset side, the company's asset-liability ratio has reached 80.09% in the first quarter of this year, with only 1.569 billion yuan of monetary funds, but its short-term interest-bearing debt totaled 3.405 billion yuan.

On the capacity side, the company's actual execution is much worse than planned. At the end of last year, the company had only 3.2GW HJT battery capacity, which was far lower than expected. However, according to the performance briefing on May 9th, the company claimed to have 5 billion yuan worth of orders on hand.

In June of this year, Akcome announced that three of the four production bases in Suzhou, Ganzhou, Huzhou, and Zhoushan would be temporarily halted. Earlier, journalists from several media companies visited Akcome's headquarters in Hangzhou, where almost all of Akcome's subsidiaries had moved to a single office, but only a few employees were left to remain.

Nevertheless, the process of moving towards delisting is not at all simple.

Now the place is empty and the equipment is covered in dust. The next step might be bankruptcy liquidation.

The deterioration of business happened in just one year, and 280,000 shareholders were pulled down. The total number of shareholder accounts was almost the same as at the highest point of 21 years. If you could discover the tricks behind the former major shareholder in time, is it worth wasting your time on this stock?

02

Not only the retail investors were tricked.

When the company's operating conditions started to reveal flaws, the actual controller Zou Chenghui was one of the first to withdraw. The funds withdrawn were enough to complete more than a dozen rounds of shareholding.

According to the statistics of iFind data from Hithink royalflush information network, the Zou Chenghui family, the actual controller of ST Aikang, held a total of 56.58% of the shares at the time of listing. However, the proportion of shares held after listing continued to decrease, and by the end of 2023, only 2.74% remained. Moreover, 2.72% of the remaining equity was frozen in November 2022 by the Second Intermediate People's Court of Beijing. Some netizens speculated that if this part of the equity had not been frozen, it might have been sold well before.

What is more heartless is that after precise reduction of its shares, the performance really took a turn for the worse.

Moreover, according to incomplete statistics, the Zou Chenghui family has accumulated more than CNY 2.5 billion through capital operations.

In the 2023 financial report, the top five shareholders of Aikang are Future No. 2, Aikang Industrial, Hong Kong Central Clearing Limited, Future No.1, and Future No. 3.

Coincidentally, Zou Chenghui is the actual controller of all the above-mentioned companies except Hong Kong Central Clearing Limited.

What's more, pledging and guaranteeing stocks is also played well. For many years, the Zou Chenghui family has pledged nearly all its shares. In October 2022, its pledged 122 million shares were publicly auctioned, with a total of CNY 365 million cashed out.

Among the A-share listed companies with caps, Aikang's net asset scale is not the smallest. Its net asset scale was CNY 2.313 billion last year, and the amount of guarantees was unexpectedly three times higher than net assets.

There are other intriguing aspects of Aikang's fund flows, such as the accumulated amount of non-financial institutional lending via the personal account of the capital supervisor, which amounted to CNY 410 million, with interest payments of CNY 22.63 million, and the other fees paid through the account of nearly CNY 30.67 million.

In recent years, local governments have played an important role in the large-scale production expansion plans of the photovoltaic industry.

The capital operation system of Aikang is also involved in a state-owned capital investment platform - Yuhang Guotou, which helped it get out of its troubles during its most difficult times, even indirectly becoming its largest single shareholder.

All the four aforementioned companies have contributed funds. However, the equity proportion continued to concentrate on this platform, as a means to offset the bond as priority partner. However, the company will have to bear the loss or profit of the corresponding share price of the public listed company, and it will seek no control within 36 months.

As a result, the money is estimated to have not yet been paid off, and the stock value is about to become a worthless piece of paper.

The production bases of the company are not just invested by Aikang alone, but also by state-owned enterprises and investment platforms under local governments.

On May 15, Aikang announced that its wholly-owned subsidiaries, Suzhou Aikang Optoelectronics Technology and Ganzhou Aikang Optoelectronics, signed a "share cooperation agreement" with Ganzhou Nankang Urban Construction Development Group.

yes

yes

Nankang Jianfa plans to invest no more than 350 million yuan to increase its stake in Ganzhou Aikang Optoelectronics or acquire the equity of Ganzhou Aikang Optoelectronics held by Suzhou Aikang Optoelectronics. The proportion of equity held in Ganzhou Aikang Optoelectronics shall not be less than 51%.

This Nankang Jianfa is another local state-owned capital; the investment Ganzhou Aikang announced at the end of last year that it would invest in the construction of a 4.6GW HJT battery project with a total fixed asset investment of 2.1 billion yuan.

Some of the company's projects are still funded by the government for construction and are operated by Aikang after construction. Now, most of the production projects are stagnant. Compared with individual investors, the local governments that have been deceived by Aikang should be more headache. The projects are rotten in their hands, and they have to queue up to ask for money.

More surprisingly, on April 15, Zou Chenghui, who personally serves as the company's secretary, publicly lied on the interactive platform, swearing that the company did not exist. The risk of ST, and the company was ST before a month, since then bearish repeatedly, and never opened the limit since May 6th.

The announcement on June 13 showed that Aikang and the actual controller Zou Chenghui have been investigated by the China Securities Regulatory Commission for suspected violations of disclosure rules.

Source: Stock bar

03

Epilogue

In this year's public research, Aikang still insists that it is one of the top three leading enterprises in the world for heterojunction HJT.

Looking ahead, the annual production capacity will reach 3.2GW of heterojunction batteries and 6.4GW of component capacity, with support and frame capacity of 10GW and 5GW respectively. At full capacity, it will achieve sales revenue of 8 billion yuan tax-free.

During the period when the company's share price was continuously down limit, it was still listed on the list of outstanding enterprises screened by foreign new energy financial media. Compared with the current situation, isn't this the biggest irony?

Source: BNEF

This is a typical case after the new 9 regulations were promulgated and the industry pattern faces reshaping.

At the photovoltaic symposium a while ago, it was mentioned that the investment promotion policies of local governments should be standardized and managed, and the requirements for key technical indicators should be optimized and improved.

In terms of HJT progress, Dongfang Risheng had achieved a component shipment of about 2GW as early as 2023, and the breakthrough of silver-coated copper technology last year gave HJT the ability to resist the rise in silver prices and gradually approach TOPCon costs, with pricing ability.

Now, with the tightening of financing under the current environment, there is no way to expand production at will. The hype of HJT, perovskite and other new concepts is no longer sexy.

Even the giants with a market value of tens of billions have to tighten their belts and live a frugal life, so how can swindlers run rampant? Some companies will eventually be eliminated.

Aikang's example is worth pondering. (End of article)