The market is waiting for the heavyweight US PCE inflation data on Friday. This year's ticket committee, and the President of the San Francisco Federal Reserve, Daly, said there was "more work to do" before interest rate cuts. The Nasdaq accelerated its decline in the late session and closed down 1%, but the Dow rose for the fifth consecutive day to a five-week high. Google and Microsoft fell from their historical highs, Nvidia's 6.7% drop was the worst in nearly two months, and it fell nearly 13% in the past three days, entering a technical correction. Its market cap evaporated by more than $400 billion and fell to the third largest in the US stock market. The Chinese concept stock index outperformed and rose 1.9% at one point, and NIO Inc. and Li Auto Inc. rose more than 3%.

US bond yields rose slightly before declining in late trading, not far from the low point since early April. The US dollar stepped back from its nearly eight-week high, and the yen once approached 160. The offshore renminbi rose above 7.28 at one point, and bitcoin's decline widened to 7%, falling below $60,000.

Oil prices rose by 1%, hovering around the eight-week high since the end of April. Brent oil closed above $86, and US natural gas rose by 4%. Spot gold rose above $2330, approaching a two-week high, and New York cocoa futures fell by 11% to a near one-month low.

The market is paying attention to the US May PCE personal consumer expenditure price index to be released on Friday. This is the inflation index that the Federal Reserve is most concerned about, and it is expected to show a year-on-year increase from 2.8% to 2.6%, which may provide clearer guidance for the timing of rate cuts.

Traders predict that the probability of the Federal Reserve starting to cut interest rates in September is as high as 67%, and the expectation of two interest rate cuts within this year is still the mainstream. David Rubenstein, co-founder of The Carlyle Group, said that it is unlikely to cut interest rates before the US presidential election in November to stay away from politics.

At least five Federal Reserve officials will speak this week, including voting directors Bowman and Cook. Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, who is due to become a voting member next year, supports interest rate cuts, saying that if inflation softens further or raises questions about interest rates being too high. However, Mary Daly, voting member and president of the San Francisco Federal Reserve said that there is "more work to be done" before rate cuts.

In addition to the final reading of the US first-quarter GDP announced during the week which is expected to show a growth of 1.6%, the US stock market will welcome the first presidential debate between Biden and Trump after trading hours on Thursday. On Sunday, the first round of French parliamentary elections will be held, which may trigger defensive pre-layout by investors.

The Nasdaq and S&P fell for three consecutive days, and the Dow rose for five consecutive days. Google and Microsoft stepped back from their highs, and Nvidia fell nearly 13% in three days, the most in nearly two months.

On Monday, June 24th, the US stock market opened high only with the Dow rising the most by 421 points or more than 1%, and Walmart hit a new high. Cyclical stocks such as energy and banks performed well, as did the Russell small-cap stocks closely related to the economy, rising by as much as 1%.

The S&P 500 index stopped falling and rose in early trading, up to 0.5% at its highest point during the day, approaching the historical high set last Tuesday, and fell back in the final trading. The Nasdaq, which is mainly composed of technology stocks, briefly rebounded before noon, but the chip stocks both fell near the end of the day to close at a daily low.

By the close, the S&P 500 index fell for three consecutive days to a new low in a week, and the Nasdaq and Nasdaq 100 fell for three consecutive days to drop from the historical high they previously set for seven consecutive days. The Nasdaq fell to its lowest level in two weeks, and the Dow rose five consecutive days to approach the highest point in nearly five weeks:

The S&P 500 index fell by 16.75 points, or 0.31%, to 5,447.87. The Dow rose by 260.88 points, or 0.67%, to 39,411.21. The Nasdaq fell by 192.54 points, or 1.09%, to 17,496.82.

The Nasdaq 100 fell by 1.2%, and the Nasdaq Technology Market Value Weighted Index (NDXTMC), which measures the performance of Nasdaq 100 technology stocks, fell by 1.8%, both falling for three consecutive days from their highs. The Russell 2000 small-cap stocks rose 0.4%, and the "panic index" VIX rose 1% and stabilized above 13.

The Nasdaq and S&P fell for three consecutive days, and the Dow rose for five consecutive days.

The eleven sectors of the S&P 500 index generally rose, but technology stocks such as Super Micro Computer, Nvidia, and Qualcomm plummeted by more than 2%, and the technology sector has fallen by 4.44% in the last three trading days. The energy sector rose 2.73%, leading the gains.

The energy sector and regional banking stocks performed the best, and large technology stocks collectively fell sharply.

Bank of America pointed out that the trend-tracking CTA (commodity trading advisor) is a large participant in the futures contract market, which may make the sell-off of technology stocks more fierce. CTA's over-holding of the long position of the Nasdaq 100 futures may trigger a collective exit from the market in the near future.

Tech stocks are mixed. Meta, the "Metaverse" concept, rose 0.8% and rebounded from its two-week low, while Google Class A fell 0.2% and rebounded from its all-time high. Amazon fell nearly 2% and rebounded from its six-week high, Tesla rose more than 3% but closed down 0.2%, Netflix fell 2.5% to a one-week low. Apple rose 2.5% and closed up 0.3%, ending its three-day losing streak, with a market cap of $3.19 trillion, ranking second in the US stock market. Microsoft fell 0.5% but also rebounded from its new high. With a market capitalization of $3.33 trillion, it is still the largest in the US stock market.

Chip stocks have fallen significantly for three consecutive days. The Philadelphia Semiconductor Index fell 3%, breaking away from its all-time high for three consecutive days, and the industry ETF SOXX fell 2.9% further away from its all-time high. Nvidia fell 6.7%, setting the largest drop in two months, breaking away from its new high for three consecutive days, with a market capitalization of less than $3 trillion, ranking third in the US stock market, and Nvidia's double long ETF fell 14%. Broadcom fell 3.7% for four consecutive days from its all-time high. ARM fell 5.8%, Qualcomm fell 5.5%, Taiwan Semiconductor Manufacturing Company fell 3.5% in the US stock market, Lam Research fell 2.5%, Applied Materials fell 2.4%, and Micron Technology fell 0.4%. All of them broke away from their new highs for three consecutive days. Intel fell 1.7% away from its four-week high, while AMD fell 0.6% in early trading.

AI concept stocks perform differently. CrowdStrike fell 0.7%, breaking away from its new high for four consecutive days, Oracle fell 1% and broke away from its new high for three consecutive days, SoundHound.ai fell 0.5%, BigBear.ai fell 1.6%, C3.ai rose 2%, Snowflake fell 2.4% to hit a 17-month low, Palantir rose more than 1%, Adobe fell 1.7% to break away from its three-month high, Dell fell more than 5%, Super Micro Computer fell 8.7%, and IBM rose 1.5%.

On the news front, Nvidia has fallen for three consecutive days and has fallen by nearly 13%, entering a technical pullback. It has dropped 16% from its historical intraday high and suffered its largest single-day decline since April, with a market capitalization evaporating by more than $400 billion in the process. Although broker Jefferies has raised its target price and claims that there is another 19% upside potential, Nvidia's stock price is 100% above its 200-day moving average, and technical support is bearish. The selling by executives such as Huang Renxun has also dealt a heavy blow to the stock price. The European Union will take action against Apple to ensure that its App Store charges to developers for acquiring new customers comply with the Digital Markets Act. Foxconn Industrial Internet Chairman Zheng Hongmeng said that the new generation of AI server GB200 is expected to be launched this year. Goldman Sachs is bullish on IBM's AI business.

Chinese concept stocks outperformed the US market. The ETF KWEB rose 0.4%, CQQQ fell 1% but approached a turnaround at one point, and the Nasdaq Golden Dragon China Index (HXC) rose 1.9% and then closed up 1.3%, once again exceeding 6,000 points, ending its five-day losing streak and breaking away from its two-month low.

Popular stocks rose across the board, with JD.com up nearly 1%, Baidu up 0.2%, and PDD Holdings down 1.6%. Alibaba rose 1.5%, Tencent ADR rose 0.5%, Bilibili fell 1.9%, NIO rose more than 3%, Xpeng rose more than 1%, and Li Auto rose 3.6%.

Among other stocks with significant changes:

Logistics giant RXO rose 23% to a record high and its best performance after going public, acquiring UPS's light asset freight brokerage business, Coyote Logistics, for over $1 billion and becoming the world's third largest freight broker.

Fintech company Affirm rose nearly 13%, recovering from its decline since June 13, and Goldman Sachs upgraded it to a buy rating, predicting a further 40% increase. Affirm's buy-now-pay-later loan service will be integrated into Apple Pay later this year. PayPal, which was downgraded to neutral by Goldman Sachs, fell nearly 2%.

Nasdaq Biotechnology Index up more than 2%, Alnylam, a concept stock of heart disease treatment, with breakthrough drug data, rose more than 34%, achieving the largest increase in nearly two years.

ResMed, a medical device company that produces ventilators, fell more than 11% to a two-month low. Inspire Medical Systems, a company specialising in the treatment of obstructive sleep apnea, fell 16% to a seven-month low. Competitor Eli Lilly and Co. once rose more than 2% and approached a historic high. Lilly's weight-loss drug tirzepatide can reduce the severity of obstructive sleep apnea.

Bitcoin fell below the psychological integer levels of $59,000 and $60,000, and blockchain technology stocks fell. The world's largest cryptocurrency mining machine firm, Canaan, fell more than 7%, and the first US crypto trading platform, Coinbase, fell 6%.

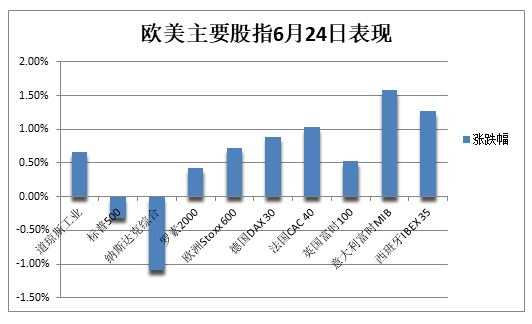

European stocks generally rose, with the Italian and French stock indices leading major countries by rising more than 1%. The German stock index also rose nearly 1%. Despite the poor performance of the technology sector, the pan-European Stoxx 600 rose 0.73%, approaching a two-week high. The Italian bank index rose more than 3%. Danish weight-loss drug maker Zealand continued to hit a historical high, rising by about 5.7%. ASM International fell 2.7%, while ASML Holding closed down more than 1.5%.

US Treasury yields rose slightly before ending the session lower, remaining close to their lows since early April. French bond prices rose.

Waiting for Friday's heavyweight inflation data, US Treasury yields rose slightly before ending the session lower. The two-year US treasury bond yield, which is more sensitive to monetary policy, rose by nearly 2 basis points and approached 4.75%, while US stocks closed down to 4.72%. The 10-year Treasury bond yield rose briefly by 2 basis points, approaching 4.28%, before falling by 2 basis points to 4.23% at the end of the session. Several weeks ago, US Treasury yields hit a ten-week low since early April.

The benchmark 10-year German bond yield rose slightly at the end of the session, up less than 1 basis point, while the two-year yield rose by nearly 2 basis points. The 10-year French government bond yield fell by more than 2 basis points. The debt-ridden peripheral countries such as Italy, Spain and Greece also saw downward pressure on their bond yields. The two-year UK bond yield rose by about 2 basis points, and the mid-to-long-term UK bond yield fell slightly by less than 1 basis point.

Oil prices rose across the board by 1%, hovering around eight-week highs since the end of April. Brent crude oil closed above $86, and US natural gas rose by 4%.

After rising and falling on Friday, oil prices rose again at the beginning of the final week of the first half of the year.

WTI August crude oil futures rose by $0.90, or more than 1.1%, to $81.63 per barrel, approaching a seven-week high. Brent August crude oil futures rose by $0.77, or more than 0.9%, to $86.01 per barrel, the highest level in eight weeks since April 30.

US crude oil WTI rose more than $1 or 1.3% at its highest point, surpassing $81 per barrel and approaching its seven-week high. The more active international Brent September futures also rose by about $1 or 1.1%, breaking through the integer level of $85.

Major investment banks such as Goldman Sachs, JPMorgan, and Citigroup are bullish on the peak summer travel season in the northern hemisphere and the demand for fuel brought about by indoor cooling, and expect that this will boost oil prices and substantially reduce inventories in the third quarter. According to TD Securities, with the intensification of the tension between Israel and Lebanon border, the supply risk in the Middle East has once again become the focus. The monthly increase in WTI and Brent crude oil prices may be 6% and 5.4%, respectively.

The European benchmark TTF Dutch natural gas futures and ICE UK futures rose by about 1% at the end of the session, after previously trading near two-week lows. US natural gas for August delivery rebounded nearly 4% and moved away from its two-week low, with a year-to-date increase of 9%.

The US dollar has retreated from its nearly eight-week high, with the yen falling below the 160 mark at one point, and offshore renminbi once rising above 7.28. Bitcoin fell below $60,000.

The DXY basket, which measures the US dollar against six major currencies, fell the most by 0.4%, breaking the 105.40 level at one point. It had reached a seven-week high last Friday, climbing above 105.90, and accumulated a 0.2% increase and three consecutive weeks of gains throughout the week.

The euro rose 0.4% against the US dollar and returned to above 1.07, breaking away from seven-week lows since the end of April, but fell by about 1% in June. The British pound rose 0.3% and attempted to approach 1.27, breaking away from its lowest level in five weeks since mid-May. The finance ministerial candidate for the far-right alliance party in France, who won in the recent election, said that they will comply with EU financial regulations, easing the trend of France's stock and bond sell-off and the euro's decline due to risk aversion.

The USD/JPY fell to 159.93 once, approaching the key psychological level of 160, and the US stock market stopped falling and rose during the day, still hovering near the lows of the past eight weeks since April 29 and is at a low point in 34 years. The market speculates that 160 may be the warning line for Japanese government intervention in the foreign exchange market. The huge interest rate difference between Japan and the United States caused the yen to fall by 1.5% in June and over 10% against the US dollar this year.

The offshore renminbi rose to a daily high at the beginning of the US stock market and rose the highest of 130 points or 0.2%, once broke through 7.28 yuan, and then narrowed its gains. It still remained above 7.29 yuan, slightly withdrawing from the seven-month low.

Mainstream cryptocurrencies have been falling for several days. The largest by market cap, Bitcoin, fell by 7% and fell below $60,000, also below $59,000, hitting the lowest point in nearly eight weeks since May 1st. The second-largest Ethereum fell 4% and fell below $3,300 to the lowest in five weeks since mid-May.

Bitcoin fell by about 10% in June, and last week it fell more than 8%, the second-worst weekly performance this year, but it still rose by more than 40% this year. Some analysts believe that only a Fed rate cut can truly benefit cryptocurrencies, which are also risky assets. The Bitcoin fund saw the largest outflow of funds for two weeks this year since the ETF approval in the United States in January. $1.2 billion was withdrawn during this period, especially after the Fed FOMC meeting.

Spot gold returned to near the two-week high of $2,330, and New York cocoa futures fell 11% to the lowest level in nearly a month.

The decline in the US dollar supports metal prices. COMEX August gold futures rose 0.7% to $2,346.40 per ounce, and COMEX July silver futures fell slightly to $29.60 per ounce.

Spot gold rose more than $12 or 0.5%, returning to above $2,330, and almost reached $2,370, the two-week high last week, but it fell sharply during the day on Friday and turned negative for the week. Spot silver oscillated and rose, still hovering at lows for the week. Analysts pointed out that the cooling of economic data supports the US to cut interest rates as soon as possible, which will benefit precious metals that do not provide fixed income. The uncertainty of elections in many parts of the world and the escalation of conflicts in the Middle East all provide support for safe-haven assets. Bank of America and Citigroup respectively released reports forecasting the long-term price of gold to reach $3,000 per ounce, and gold rose to a historic high of $2,450 on May 20.

Spot gold returned to near the two-week high of $2,330.

London industrial metals rose and fell, and the changes were not significant. The economic barometer copper doctor fell by $22 or 0.2%, still less than the integer level of $9,700, approaching the low of two months. London aluminum also fell slightly and lingered at its lowest level in two months. London zinc rose slightly, London lead fell slightly, London nickel rose 0.6%, but still not far from the low since early April. London tin closed slightly higher.

New York cocoa futures fell more than 11% and fell below $7,900 per ton, the lowest in almost a month. Some analysts are worried that the record-high prices will damage demand when the global report for the second quarter is released next month. Cocoa prices have risen 88% this year and are expected to achieve the best performance since 1980. Cocoa futures fell more than 11.6% last week.

Edited by Jeffrey