Summary

COMEX copper prices have shifted downward from the previous curve and the curve is further converging at the near end, but the monthly difference in the near end is rising again. There are only two weeks left until the start of delivery of the July contracts, but there are still no delivery notices. The position of the July contract remains high, and with the continuous elimination of COMEX copper inventories, which is currently less than 10,000 tons, the price difference in the near end is rising again, reflecting the market's concerns about the upcoming delivery. The next two weeks will be critical.

Key Takeaways

In regards to precious metals, last week, COMEX gold fell by 0.2%, and silver rose by 2.1%; SHFE gold 2408 contract rose by 2.4%, while SHFE silver 2408 contract rose by 5.7%. Among the mainstream industrial metal prices, COMEX copper and SHFE copper changed by -1.46% and -1.29% respectively. Last week, precious metals and copper prices oscillated.

Please use your Futubull account to access the feature.

Copper prices rose and fell last week. The market still assumes that the US will experience an escape recession and, under the backdrop of accepting a one-time rate cut, it is still sensitive to data that can relatively prove economic resilience. For example, initial jobless claims were better than expected in the middle of last week, and the market rebounded significantly. However, the sustainability of this indicator is insufficient, and last Friday, the market broke down this part of the premium.

Currently, the market's basic assumption is still that the US is going to undergo an escape recession. Under the backdrop of accepting a one-time rate cut, the market is still sensitive to data that can relatively prove economic resilience. For example, initial jobless claims were better than expected in the middle of last week, and the market rebounded significantly. However, the sustainability of this indicator is insufficient, and last Friday, the market broke down this part of the premium.

COMEX precious metal prices fluctuated last week, and COMEX gold and silver ran at around 2330-2370 US dollars/ounce, and around 30 US dollars/ounce respectively.

Last week, COMEX precious metal prices fluctuated in general. It was proven again last week that the current precious metal is anchored to the expectation of economic growth, and when initial jobless claims were better than expected in the middle of the week, precious metal prices rose with the US dollar. However, on Friday, the expected economic growth faded and prices fell under pressure.

Review of basic metal market.

(1) Observation of COMEX/SHFE copper markets.

Last week, COMEX copper prices rose and fell, receiving support below $4.5/pound at the beginning of the week, rebounded somewhat in the middle of the week, but fell sharply on Friday. Currently, the market's basic assumption is still that the US is going to undergo an escape recession. Under the backdrop of accepting a one-time rate cut, the market is still sensitive to data that can relatively prove economic resilience. For example, initial jobless claims were better than expected in the middle of last week, and the market rebounded significantly. However, the sustainability of this indicator is insufficient, and last Friday, the market broke down this part of the premium.

Last week, SHFE copper prices oscillated around CNY 79000/tonne without significant driving factors. Domestic demand has basically absorbed the data weakness of macro-level before, but has not acquired any new upward driving factors. It is still premature for China to start filling stocks. The consumption situation at the micro level was not optimistic in the last week. The situation of stock depletion showed signs of weakening again. If there is a lack of support from domestic physical buying, copper prices may not be able to stand on the current platform.

In terms of deadlines, COMEX copper prices have shifted downward from the previous curve and the curve is further converging at the near end, but the monthly difference in the near end is rising again. There are only two weeks left until the start of delivery of the July contracts, but there are still no delivery notices. The position of the July contract remains high, and with the continuous elimination of COMEX copper inventories, which is currently less than 10,000 tons, the price difference in the near end is rising again, reflecting the market's concerns about the upcoming delivery. The next two weeks will be critical.

In terms of SHFE copper prices, the curve has shifted upward from the previous curve, consumption weakened after the price rebounded last week, and spot discounts expanded again. At present, many funds have started to adopt the 'borrow strategy' of SHFE copper. We believe that this strategy is still in the expectation phase, so it is not appropriate to implement the strategy at the current level.

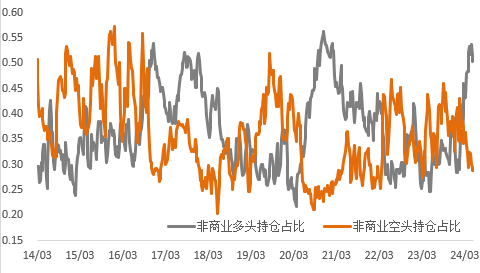

In terms of positions, from the CFTC positions, last week's non-commercial long positions peaked and fell back, and the price decline corresponded to this situation. The current proportion is at a high level, and there is still room for decline.

Figure 1: CFTC Fund Net Positions

Data Source: Wind

Last week, the prices of precious metals and copper fluctuated.

Last week, the copper concentrate index was $2.2/dry tonne, an increase of 0.1 US dollars/dry tonne from last week. The copper concentrate spot market is stable, and the mainstream transaction volume of the near-month shipping date remains at a low-single-digit figure, while the bidding and quotation of remote shipping data has edged up. The bidding of traders continues to be aggressive, but the activity of tendering has declined. The supply and demand ends are basically stable. It is expected that the TC will remain at a low level in the short term. Market participants continue to focus on the progress of the mid-year negotiations and the CSPT conference.

Figure 2: Copper Concentrate Processing Fee

Data Source: SMM

In terms of spot, copper prices have been fluctuating narrowly during the week, downstream demand for purchases still exists at low levels, but the willingness to advance replenishment is still low. Moreover, some companies have the psychology of further bearishness, and the acceptance at this price level has declined. In addition, the performance of new orders is average because of the slowdown in downstream consumer growth. In recent weeks, the Shanghai market has continued to reduce inventory, and the domestic smelter's export volume in June is still considerable, so the subsequent supply of domestic goods may be limited. Under the demand for low-end goods, inventory is expected to remain low, combined with a large premium for spot, traders will still perform demand for registration receipts on dips, so next week's premiums may stabilize and rebound.

Figure 3: Shanghai copper premiums

Data source: SMM

Domestic market electrolytic copper spot inventory was 396,100 tons, down by 31,900 tons from the 13th and 7,700 tons from the 17th. This week, the Shanghai market's inventory continued to show a slight decrease, mainly due to the narrow fluctuation of copper prices, and downstream demand for purchases still exists. Moreover, some imported copper flowed into the market, and the inventory also decreased but not significantly. Inventory in Guangdong market decreased significantly, mainly due to the reduction in arrivals, with fewer warehouses entering, so the inventory continued to decrease. This week, the cumulative inventory of electrolytic copper spot in Shanghai and Guangdong bonded areas was 94,300 tons, which was a decrease of 4,500 tons from the 13th and 1,000 tons from the 17th. Bonded area inventory showed a slight decrease, with some sources clearing customs and imports, and there are still sources exported to LME warehouses, so inventory decreased slightly.

Figure 4: Global refined copper inventory (including bonded areas)

Data source: Wind

This week, the processing fees of 8mm copper rods were all significantly lowered, with the most significant drops in the East and South China markets; the weekly orders for copper rods in the market decreased, and downstream acceptance of prices significantly decreased. The sentiment of copper scrap traders holding out for higher prices has increased, and the difficulty of copper rod companies to purchase has increased. The difference in price between refined and waste copper rods and the extent of backwardation of copper futures ran steadily during the week. Looking ahead, due to the current advantage of refined copper rods, the purchase preference in the market has also begun to change, but with the gradual increase in the activity of refined copper rod trading and the advancement of trading processes, downstream acceptance of refined copper rod prices has also been significantly reduced, and the mainstream trading mentality in the future will still be cautious and focused on replenishing on dips, and it will take some time for order growth to react.

Figure 5: Refined copper-scrap copper price differential

Data source: SMM

Precious metals market review

(1) Precious Metals Market Monitor

Last week, the prices of precious metals on the COMEX fluctuated, and COMEX gold and silver were traded within the range of US$2,330-2,370/ounce and US$30/ounce. It once again proved that what precious metals are anchored to is economic growth expectations. In the middle of the week, the initial claims for unemployment benefits were better than expected, and precious metal prices rose with the dollar, but on Friday, economic growth expectations faded, and prices fell under pressure.

(2) Ratio and Volatility

Last week, gold outperformed silver, and gold-silver ratio rebounded; copper price was weak compared with gold, and gold-copper ratio fluctuated upward; crude oil prices were relatively strong, and gold-oil ratio went down with it.

Figure 6: COMEX gold/COMEX silver

Data source: Wind

Figure 7: COMEX gold/LME copper

Data source: Wind

Figure 8: COMEX gold/WTI crude oil

Data source: Wind

Recently, the gold VIX has fallen, and the concentration of long funds boosted by the safe-haven demand for gold, which intensified with the geopolitical conflict, is gradually withdrawing.

Figure 9: Gold Volatility

Data Source: Wind

The recent impact of the RMB exchange rate has weakened compared to the previous period, and the spread between gold and silver inside and outside has fallen last week. The ratio of gold and silver inside and outside has also declined.

Figure 10: Precious Metal Inside and Outside Spread

0

Data source: Wind

Figure 11: Gold Inside and Outside Ratio

1

Data Source: Wind

(III) Inventory and Holding Positions

In terms of inventory, COMEX gold inventory last week was 17.644 million ounces, a decrease of about 20,000 ounces from the previous period. COMEX silver inventory was about 296.399 million ounces, an increase of about 7.627 million ounces from the previous period. SHFE gold inventory was about 8.04 tons, basically flat from the previous period, and SHFE silver inventory was about 686.6 tons, a decrease of about 3.5 tons from the previous period.

Figure 12: COMEX Precious Metal Inventory

2

Data source: Wind

Figure 13: SHFE Precious Metal Inventory

3

Data source: Wind

In terms of holding positions, the SPDR Gold ETF holding positions decreased by 1.7 tons to 830 tons on a month-on-month basis, and the SLV Silver ETF holding positions decreased by 145 tons to 13,190 tons on a month-on-month basis. Last week, COMEX non-commercial total gold holdings were 353,000 lots, of which non-commercial net long positions decreased by 685 lots to 279,000 lots, and short positions decreased by 2,004 lots to 75,000 lots; non-commercial long positions accounted for a larger proportion, falling to around 53.6% from last week, while non-commercial short positions fell to around 14.4%.

Figure 14: COMEX Gold Holdings

4

Data source: Wind

Figure 15: COMEX Gold Holding Ratio

5

Data source: Wind

Figure 16: COMEX Silver Holding Positions

6

Data source: Wind

Figure 17: COMEX silver holding ratio

7

Data source: Wind

Market outlook

Currently, the domestic market has basically digested the previous weakness in macro data, but has not received new upward drivers. It is too early to say that domestic replenishment has started. The consumption situation at the micro level was not optimistic last week, and there were signs of weakening of destocking last week. Without the support of domestic entity bids, the copper price may not be able to stand firm at the current platform.

There are few macro data this week, and there is a lack of guidance of new incremental information. It is expected that the gold price may still run according to the previous logic, and it is difficult to break through the platform support of $2300/oz in the short term.

Focus and risk warning

US GDP, initial jobless claims, right-wing trend in Europe, etc.