Summary

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that as the market enters the overbought range, investors' divergences and profit-taking are not surprising. However, with the recent continuous decline of the market, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we believe that it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support. Looking back at this week's market performance also confirms our previous judgment. In addition, compared with A shares that have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares.

The recent market correction is mainly due to the continued weakness of the underlying fundamentals of the domestic market, and the continued contraction of private credit is also a major reason. In addition to generally weak financial data, economic data in May also showed that the underlying fundamentals are not stable and the differentiation is significant. The production side is still weak, and consumption is recovering faster. Fixed asset investment is further declining. Recent high-frequency data also shows this, and the production and consumption sides are still weak, and the price index is weaker than last week.

The main reason for the current weak growth is still the contraction of private sector credit. The key to solving this problem is to use external fiscal expansion to offset private sector credit contraction on the one hand, and to reduce the financing costs of the private sector to partially boost investment willingness on the other hand. For the former, the broad fiscal deficit impulse still needs to be released in a timely manner. If the progress of the subsequent issuance and storage of ultra-long-term bonds can be accelerated, it may be reflected in the boost to third-quarter growth. For the latter, the weak May financial data once prompted expectations of interest rate cuts, but it has not been realized. President Pan's speech at this Lujiazui meeting also shows that the operational space of monetary policy is still subject to many internal and external constraints.

The Hong Kong stock market still has comparative advantages over A shares, mainly reflected in: 1) the valuation clearance is more thorough; 2) the warehouse clearance is more comprehensive; 3) profits benefit from structural differences better than A shares. In terms of allocation, it is recommended to pay more attention to structural opportunities, mainly in three directions: overall return downside, partial leverage and partial price increase.

Will the market face greater pressure? A review of market trends.

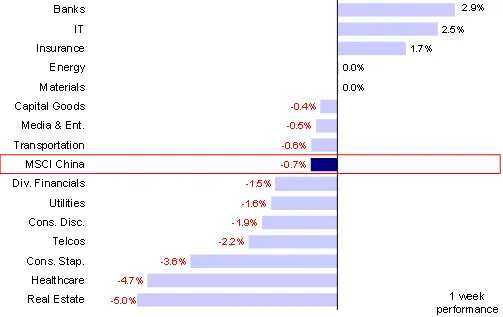

The Hong Kong stock market continued its volatile trend this week. It rose sharply on Wednesday and outperformed A shares, but then immediately gave back almost all gains in the next two days. Throughout the week, among the main indexes, the Hang Seng Index and the Hang Seng State-owned Enterprises Index slightly rose, up 0.5% and 1.0% respectively last week. The Hang Seng Tech Index and MSCI China Index fell slightly by 0.2% and 0.7% respectively. In terms of sectors, banks, information technology and insurance increased by 2.9%, 2.5% and 1.7% respectively, while other sectors fell to varying degrees. Among them, real estate and medical care were the most lagging, falling by 5.0% and 4.7% respectively.

Chart: Except for banks, information technology and insurance that achieved increases, other sectors all fell to varying degrees.

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that this round of rebound is mainly driven by the funding side and emotions. Therefore, with the market entering the overbought range, investors' divergences and profit-taking are not surprising. Assuming that the risk premium is fully restored to the level of the high point at the beginning of 2023, the corresponding target index level of the first stage of the Hang Seng Index is 19,000-20,000 points (see May 12th "The market is approaching our first stage target" and May 26th "not surprisingly taking profits"). In the past few weeks, overseas funds, especially value-oriented active foreign funds, have flowed out again. The outflow scale this week has increased from USD 93.24 million last week to USD 340 million. This can also provide proof ("Active Foreign Funds Maintain Weakness"). However, with the recent continuous decline of the market, especially A shares falling below 3,000 points again, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we are not so worried, although we have always believed that further upward momentum needs more catalysts to start, it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support, and looking back at this week's market performance also confirms our previous judgment ("temporary pause or end of rebound"). In addition, compared with A shares, which have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares ("The Hong Kong stock market still has a comparative advantage").

Since the peak at the end of May, the Hong Kong stock market has fallen nearly 10%. Since mid-May, we have been reminding investors that as the market enters the overbought range, investors' divergences and profit-taking are not surprising. However, with the recent continuous decline of the market, concerns about the Hong Kong stock market falling to the previous low are also increasing. In this regard, we believe that it will not completely give up all the gains, and the Hang Seng Index around 18,000 points can get some support. Looking back at this week's market performance also confirms our previous judgment. In addition, compared with A shares that have returned all gains since March, the Hong Kong stock market has shown obvious resilience, which is consistent with our judgment that the Hong Kong stock market is better than A shares.

Chart: The Hong Kong stock market is currently approaching the oversold area.

Recently, the market has experienced a correction. In addition to profit-taking from overbought positions, the weak domestic fundamentals and continuing private credit contraction are the main reasons. Apart from weak financial data, May's economic data also shows that the fundamentals are not stable and there is obvious differentiation. The production side is still weak. The industrial added value of above-scale enterprises grew by 5.6% YoY, a significant drop from last month's 6.7%. On a month-on-month basis, it grew by 0.3%, lower than the five-year average. Consumption is recovering faster. Due to the impact of the holiday, the total retail sales of consumer goods increased by 3.7% YoY in May, expanding from the growth rate of 2.3% in the previous month. Optional consumption, such as cosmetics, household appliances, and audio equipment, performed well, but auto retail sales have declined for three consecutive months and fell by 4.4% YoY in May, significantly dragging down the total retail sales of consumer goods. Fixed-asset investment continued to decline, with the growth rates of infrastructure investment and real estate investment both descending. Recent high-frequency data also shows that the production and consumption sides are still weak, and price indices are weakening compared to the previous week.

Chart: China's industrial added value for May is lower than expected.

The main reason for the current weak growth is still the credit contraction of the private sector. May's financial data further reflected this point. In fact, due to the slowdown in fiscal stimulus since February and continued contraction of resident and corporate credit in the second quarter, the overall macroeconomic leverage has not yet broken free from the tight situation. To solve this problem, on the one hand, it is necessary to use external fiscal expansion to offset private credit contraction, and on the other hand, it is possible to reduce the financing cost of the private sector to partially boost investment willingness ("Outlook for HKEX in the second half of 2024: The path is always muddy when you set out on it"). As for the former, measured from the perspective of the general government deficit impulse, it accelerated after Q4 2023 but slowed down in February and only began to accelerate again in May, but the speed and extent still need to be strengthened. Although government financing increased in May's social financing data, fiscal deposits increased by 526.4 billion yuan YoY, indicating that fiscal stimulus still needs to be released in a timely manner. If the progress of ultra-long bond issuance and acquisition can be accelerated subsequently, it may boost the growth in Q3. For the latter, May's financial data, which was lower than expected, at one point fueled expectations of a rate cut, but this expectation was not fulfilled. At the Lujiazui Forum, Pan Gongsheng, the governor of the People's Bank of China, delivered a speech, saying that the monetary policy stance still maintained its supportive nature and emphasized that the high interest rate monetary policy stance of developed economies put great pressure on the RMB for further depreciation. This once again shows that the current monetary policy operation space is still subject to many internal and external constraints. At the same time, the delayed Fed rate cut expectation has further delayed and suppressed the downward space of interest rates, which is basically consistent with our judgment that it is unrealistic to expect policy to "strongly stimulate" in the benchmark scenario in the second half of the year.

Chart: May's urban fixed-asset investment is lower than expected.

Externally, the upward revision of the U.S. fiscal deficit forecast by the CBO and the better-than-expected U.S. PMI this week have both had some impact on expectations of a rate cut. The first round of the U.S. election debate will also take place next week, and the divergent policy views of Trump and Biden may cause short-term market volatility, further suppressing the space for rate cuts. Overall, we believe that the market will still maintain a volatile pattern in the short term until fundamental margin changes in the above policies bring new catalysts. Looking to the future, profits are still the key to opening up greater market space. Among the three main drivers of the market, short-term risk premiums have been repaired for the most part, and there is very limited short-term room for risk-free rates to move. We calculate that if earnings can achieve 10% growth in 2024, the Hang Seng Index is expected to climb to 22,000 points or higher. However, under the benchmark scenario, we believe it is still difficult to achieve this until we see fundamental and substantial margin changes in policy.

Nevertheless, compared to A shares, Hong Kong stocks still have a relative advantage, mainly reflected in the following aspects: 1) Valuation has been more thoroughly cleared out, and the Hong Kong stock valuation is still lower than the historical mean 1.6 standard deviations. After the valuation of internet companies and other core assets of Hong Kong stocks lowered for three years, the pullback has been quite sufficient; 2) Clearance of positions is more comprehensive. The active funds tracked by EPFR globally have reduced the proportion of Chinese stocks from a high point of 14.6% in October 2020 to 5.7% at the end of April; 3) Profits benefit from structural differences better than in A shares. The upstream cycle and the internet have performed well, which are also the sectors with a large weighting in Hong Kong stocks, while real estate and middle-end manufacturing, which account for a large proportion of A shares, are generally under pressure.

In terms of allocation, under the environment where overall growth is weak, and the market is in a consolidation stage, it is recommended to pay more attention to structural opportunities, mainly in three directions: overall return decline (stable high dividends and high buybacks), partial leverage (policy support and growth of technology), and partial price increase (natural monopoly sectors, such as upstream and public utilities). Firstly, we still like high dividends (traditional telecoms, energy, public utilities, and some internet consumption that is stable cash cows) as the "dumbbell" end for long-term allocation value under the background of declining overall return. This week, China New subscribed to the Hong Kong Stock Connect Central State-owned Enterprises Dividend ETF, which once again conveyed a bullish signal for the long-term allocation value of Hong Kong stocks' central state-owned enterprise dividend shares. CICC's Hong Kong stock high-dividend combination has risen by 34.1% since the beginning of the year, proving that this strategy has been effective. Secondly, some sectors that are expected to benefit from policy support or improve in their business environment are still expected to be boosted by favorable news and show greater elasticity. This week's Lujiazui Forum saw the new chairman of the China Securities Regulatory Commission, Yi Huiman, pointing out that the CSRC will issue a set of eight measures to deepen the reform of the STAR Market, and the Third Plenum also has expectations for policy support aimed at boosting productivity in new directions. Based on this, we are optimistic about some sectors with better business environment, such as electrical equipment, technology hardware, semiconductors, software, and services. These areas still have room for leverage increases. Thirdly, compared to some industries where falling prices hurt profit margins, sectors with rising prices such as natural gas, nonferrous metals, and public utilities, and even some essential consumer goods, can protect business profit margins and enjoy greater bargaining power.

Specifically, the main logic that supports our above views and the changes that needed to be noted last week mainly include:

In May, the year-on-year growth rate of industrial value added above designated size was lower than expected. In May 2024, the industrial value added above designated size increased by 5.6% year-on-year, which was a decrease of 6.7% compared with the same period last month, and was lower than the Bloomberg consensus forecast of 6.2%. From a month-on-month perspective, it increased by 0.3%. In terms of industry, the year-on-year growth rate of automobile production has slowed significantly, while computer electronics, rail transportation, and ships have maintained strong resilience, but food processing and cement production are still weakening.

In May, the year-on-year growth rate of urban fixed asset investment was lower than expected. The year-on-year growth rate of urban fixed asset investment in May was 4.0%, which was lower than the year-on-year growth rate of 4.2% in the previous month and the consensus forecast of 4.2%, and decreased by 0.04% month-on-month. Among them, the year-on-year decline in real estate investment expanded slightly from 10.5% in April to 11%, the year-on-year growth rate of infrastructure investment fell from 5.9% in April to 3.8%, and manufacturing investment continued to expand, rising slightly from 9.3% in April to 9.4%.

In May, the total retail sales of consumer goods in China were higher than expected. The nominal year-on-year growth rate of social consumer goods retail sales in May was 3.7%, higher than 2.3% in April and the consensus forecast of 3.0%. Among them, the year-on-year growth rate of catering and automobiles in May decreased compared to the first quarter, while cosmetics and daily necessities increased significantly compared to the first quarter. At the same time, in May, the national production index of the service industry increased by 4.8% year-on-year, up from 3.5% last month, and higher than the year-on-year growth rate of social consumer goods.

In June, both the manufacturing and service PMI in the United States exceeded expectations. The Markit Manufacturing PMI in the United States in June rose again to 51.7 month-on-month, higher than the market expectation of 51 and the previous value of 51.3; among them, the forward-looking new order sub-index strengthened month-on-month, while the new export weakened. The Markit Services PMI in June rose to 55.1 month-on-month, higher than the market expectation of 53.7 and the previous value of 54.8, reaching a 13-month high; from a sub-item perspective, cost prices and service prices weakened, while new orders increased significantly month-on-month.

Liquidity: The strong inflow of southbound funds continued last week, and overseas funds remained outflowed. Specifically, data from EPFR shows that last week, overseas active funds flowed out of the overseas China stock market, with an outflow scale of approximately US$34 million, which was slightly higher than the outflow scale of US$93.24 million the previous week, and have been outflowing for 51 consecutive weeks. Passive overseas funds turned into inflows of US$270 million. Southbound funds maintained a strong inflow trend last week, with a cumulative inflow of HK$24.12 billion, which was slightly lower than the previous week's inflow of HK$26.96 billion.

Figure: Overseas active funds continued to flow out of the overseas China stock market, while the inflow trend of southbound funds remained unchanged.

Edited by Jeffrey