The weather is good today The weather is good today.

Dell is receiving a large number of ai server orders, especially from second-tier cloud computing service providers.

Several weeks ago, there were rumors in the market that Musk's xAI would create a supercomputer.

This serves the datacenter for autonomous driving and the next generation of Grok models, and is another giant computing factory after Meta supercomputing center. xAI's supplier has always been highly regarded by the market.$Tesla (TSLA.US)$Last night, Musk publicly announced the rack supplier for xAI on his Twitter, and said the shares were split evenly between the two companies.

The word 'datacenter' is translated as 'datacenter', please use this translation.$Dell Technologies (DELL.US)$ and $Super Micro Computer (SMCI.US)$, and stated that each party holds half of the shares.

It should be noted that this data center has purchased 100,000 H100 computing cards, and its scale is at least four times that of the current largest AI cluster.

Subsequently, Dell rose for three consecutive days, with an increase of more than 13%. Super Micro also rose 4.5% in two days.

Why did Dell rise?

Why did Dell's increase almost double that of Super Micro?

Mainly because of the cooperation with xAI, it broke the market's low expectations for Dell.

As discussed in "AI Server Shipping Wave, Why Did Dell's Profit Unexpectedly Slip". Dell's latest quarterly report showed that its storage business and operating profit were lower than market expectations.

Due to Dell's low profit margin in the AI server field, the market is worried that Dell's profit expectations for subsequent AI servers will weaken.

However, the cooperation with xAI gave the market a shot in the arm and boosted expectations for Dell once again.

Three days ago, Goldman Sachs released a report on Dell. According to feedback from the supply chain, Dell's orders are stronger than originally expected, and it is gaining a large number of orders, especially from secondary cloud computing service providers.

Goldman Sachs further stated that the assembly of AI servers is not simple, and there are high technical barriers, and there are not many manufacturers that can mass-produce on their production lines.

At the same time, Dell has always been in a leading position in end-to-end computing solutions for enterprises. Nvidia CEO Jen-Hsun Huang has also emphasized that Dell is the first choice for any business computing needs.

In addition, facing the low profit margin of its AI server business, industry experts speculate that Dell is currently adopting a strategy of seizing market share at low rates, and in the long run, the AI business is still worth looking forward to.

Goldman Sachs pointed out that the current market demand for storage is also recovering, which will help Dell's overall positive prospects.

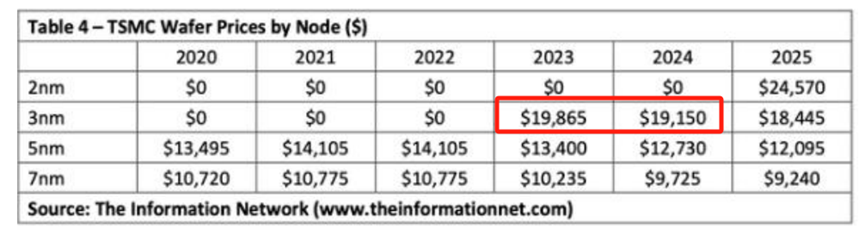

Taiwan Semiconductor’s price increase may bring 3% to 6% of revenue growth space.

1. Taiwan Semiconductor's price increase

In early June, at the COMPUTEX 2024 Taipei Computer Expo, there were rumors that Taiwan Semiconductor's 3nm process would rise.

There are mainly three reasons for the price increase.

The high chip prices are in contrast to Taiwan Semiconductor's low supply costs.

The H100 sells for 25,000 to 30,000 US dollars, while Taiwan Semiconductor's supply cost is only 666 US dollars.

Specifically, Taiwan Semiconductor's 3nm process wafer is priced at $20,000, and one wafer can produce 30 H100 chips, which means that each H100 chip sells for only $666.

After acquiring the H100, Nvidia sold it for $25,000 to $30,000.

After rumors of a price hike by Taiwan Semiconductor, Nvidia CEO Huang Renxun expressed his agreement, stating that "Taiwan Semiconductor deserves a higher quote."

Citi commented that Taiwan Semiconductor should be able to reflect its value to customers in the context of the surge in demand for AIGPU/accelerators and edge AI devices.

2) The rise in production factor costs such as materials, R&D costs, and electricity.

The rise in production factor costs such as materials, R&D costs, and electricity has prompted Taiwan Semiconductor to raise prices.

Taiwan Semiconductor management pointed out that the company is facing cost increases from some overseas wafer factories, inflation, and higher electricity bills.

And stated that it will charge higher prices for overseas wafer factories than for Taiwanese wafer factories.

Previously, there were many reports that the cost of Taiwan Semiconductor's US factory was much higher than that of its Taiwan factory, one of the main reasons being that labor costs in the US are much higher than in Taiwan.

Therefore, the price increase is reasonable on the one hand, and Taiwan Semiconductor needs to maintain the company's profitability and growth on the other hand.

Therefore, a price increase is justified.

3) Demand is greater than supply.

From an economic point of view, if demand is greater than supply, prices will rise accordingly, and high prices will prevail.

Citi pointed out that in addition to Apple, there will be a large number of N3 orders from Intel, Qualcomm, and MediaTek in the second half of 2024, and more N3 AI GPU/accelerator orders are expected in 2025.

Currently, the only foundries that can supply 3nm globally are Taiwan Semiconductor and Samsung. However, Samsung's 3nm is delayed, and Samsung's own high-end SoC can only use Taiwan Semiconductor.

Taiwan Semiconductor will be the only one in 2024-2025, and a price hike will follow the trend.

2. The impact of price increases on revenue.

On June 17th, according to Commercial Times, Taiwan Semiconductor may increase the wafer prices of N5 and N3.

As of Q1 2024, the N5 and N3 processes respectively account for 37% and 9% of TSMC revenue.

Currently, due to limited production capacity of the N3 process at TSMC, most AIGPU/accelerator is on the N7/5/4.

Citigroup predicts that as TSMC's N3 production capacity is being implemented and capacity utilization rate improves, N3's revenue proportion will increase.

In addition, with the emergence of AI PC/smartphones, advanced processes (N5/4/3) will continue to be in short supply.

Citigroup predicts that advanced nodes (N5/4/3) will account for 53%/61% of TSMC's 2024E/25E revenue, and expects the average selling price of N5 and N3 processes to increase by 5-10%, providing TSMC with about 3% to 6% of revenue upside.

Editor/tolk