Analyst Mosesmann said that Nvidia's stock price still has nearly 48% upside potential. He raised Nvidia's target stock price to $200 per share, citing Nvidia's strong profit potential. He said, "The real story is the perfecting of software for all hardware."

Even though NVIDIA's stock price has risen by nearly 210% within a year and recently topped the US market cap rankings, some analysts are still bullish on its prospects and have raised the target price to the historical high of $200 per share.

Hans Mosesmann, an analyst at Rosenblatt Securities, recently released his latest view and upgraded NVIDIA's rating from "neutral" to "buy", raising the target price from the previous $140 to $200. He has always been a loyal fan of NVIDIA.

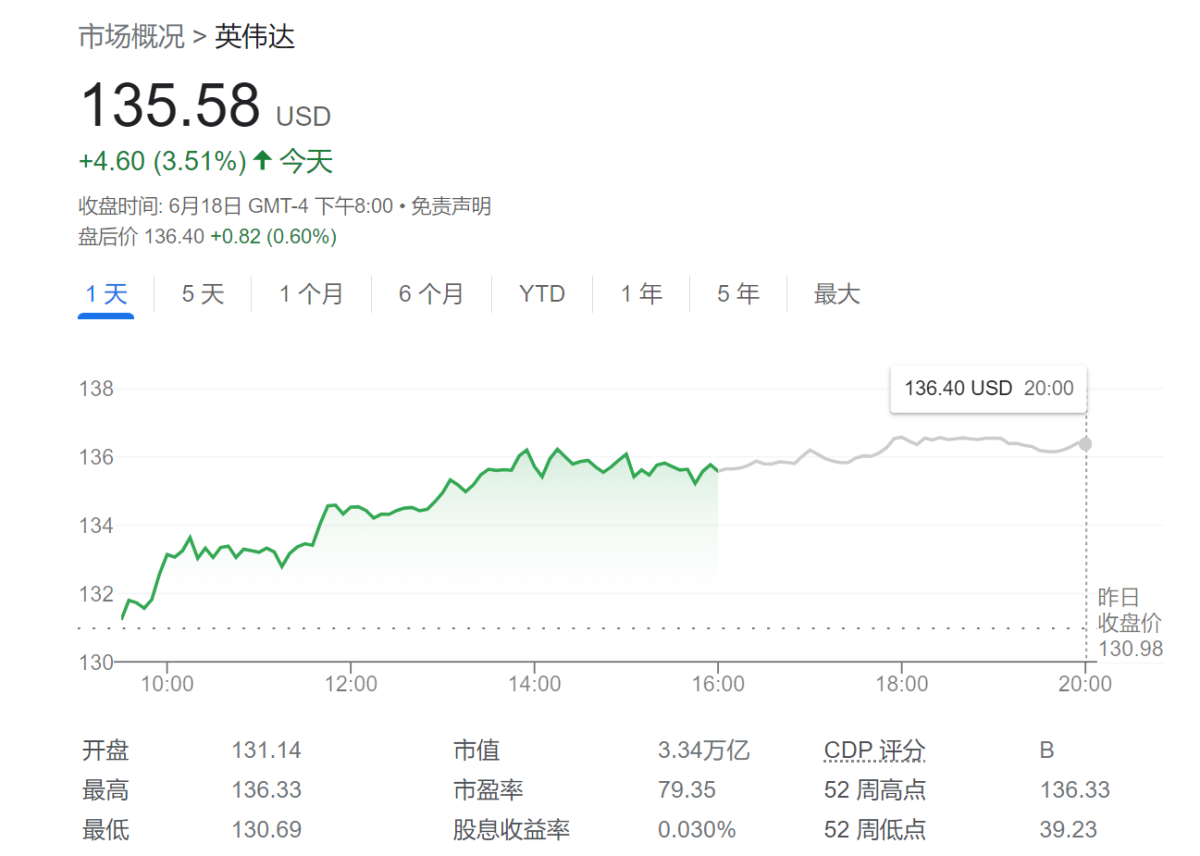

As of Wednesday's close, NVIDIA rose 3.51% to $135.58. "$200" means the stock can rise nearly 48% above its current level. This call prediction will also make NVIDIA's market cap reach a record $5 trillion.

But Mosesmann believes that the chipmaker deserves such a stock price.

"We've seen NVIDIA's Hopper, Blackwell, and Rubin series drive 'value' market share in the cycle," he added.

Bullish on Software Business

Looking to the future, he believes that NVIDIA's real profit driver is not its GPU business, but its software business, led by NVIDIA's popular CUDA platform.

Mosesmann noted that millions of developers are using NVIDIA's CUDA to build large language models and other programs on the company's AI-supporting GPU chips.

"The real story is the software's improvement upon all hardware. We expect the software business to grow significantly over the next decade, relative to the overall sales portfolio, and tend to value it upwards due to sustainability," he said.

Mosesmann also said that if NVIDIA can get substantial recurring revenue from its software business, it will make the company's income more predictable, which reduces the risk the company faces.

It is understood that NVIDIA has historically relied on hardware sales to drive revenue growth, and hardware sales are usually cyclical and go through very unstable periods of "boom and bust". Currently, NVIDIA's hardware business is in an unprecedented boom.

But Mosesmann said that NVIDIA's software business could help push the company's profit to $5 per share adjusted for a 1:10 split by 2026. Based on a PE ratio of 40, NVIDIA's target stock price is $200.

Beth Kindig, an analyst at I/O Fund Tech, has a similar view.

"The CUDA software platform is the platform that developers learn from. So, this is similar to iOS: the reason why people are locked into the iPhone is because developers are developing apps for the iPhone. The same thing is happening to NVIDIA, AI engineers are learning the CUDA platform to program for GPUs, so it helps to lock them together. Now, I call it an invincible moat," he said.

Kindig believes that by the end of 2030, NVIDIA's valuation could ultimately reach $10 trillion, an increase of 205% from the current valuation level.