The tax authority in charge has conducted multiple ingredient tests on Ningbo Bohui Chemical Technology's "heavy aromatic hydrocarbon derivatives" regarding the controversy over the "tax supplement" incident. After the adjustment of tax policies, the company immediately optimized the process of its facilities in July last year, stirring up suspicions of tax evasion. According to the information disclosed by the company, the estimated tax amount for related products is 2105 yuan/ton, and the average price of products in the first quarter of this year is about 4700 yuan/ton.

On June 19th, Caixin reported on the huge "tax supplement" incident of Ningbo Bohui Chemical Technology Co., Ltd. (300839.SZ), which is a hot topic among A-share investors. Is "Heavy Aromatic Hydrocarbon Derivatives" the same thing as "Heavy Aromatic Hydrocarbons" that are subject to consumption tax? Was the company's process optimization in July last year a tax evasion behavior after the tax policy adjustment? What about the huge consumption tax refund that it enjoyed before? Will supplementing the tax payment lead to huge losses and force the company to stop production? In the face of these mysteries, Caixin reporters have recently conducted multiple interviews in an attempt to reveal part of the truth for you...

"Heavy Aromatic Hydrocarbon Derivatives" is one of the main points of contention in the Ningbo Bohui Chemical Technology Co., Ltd. "tax supplement" incident.

Whether "Heavy Aromatic Hydrocarbon Derivatives" is considered as "Heavy Aromatic Hydrocarbons" is the focus of the Ningbo Bohui Chemical Technology Co., Ltd. "tax supplement" incident.

"Heavy Aromatic Hydrocarbon Derivatives" is composed of multiple components and has no molecular formula. The person in charge of Ningbo Bohui Chemical Technology Co., Ltd. explained to Caixin reporters about the chemical composition of the Heavy Aromatic Hydrocarbon Derivatives produced by the company. At present, there are no national standards for both "Heavy Aromatic Hydrocarbon Derivatives" and "Heavy Aromatic Hydrocarbons". The industry generally distinguishes them based on product form, appearance, carbon number distribution, main components, and product uses. Product names are defined based on the main ingredients.

According to a national standard information public service platform, 41 national standards were retrieved under the category of aromatic hydrocarbon, while no relevant national or industry standards were found for Heavy Aromatic Hydrocarbons.

Regarding the "tax supplement" incident, the aforementioned person in charge of Ningbo Bohui Chemical Technology Co., Ltd. stressed that the "Tax and Finance Notice No. 11" is aimed at levying consumption tax on finished oil products. The essence of taxable products must conform to the characteristics of finished oil products, while the Heavy Aromatic Hydrocarbon Derivatives produced by the company are all solids at room temperature and are completely different from finished oil products. "The products of similar companies have the same characteristics as the Heavy Aromatic Hydrocarbon Derivatives produced by our company, but because they are not called Heavy Aromatic Hydrocarbons or Heavy Aromatic Hydrocarbon Derivatives, they are determined to be chemical products and do not need to pay consumption tax," the person in charge further explained.

Leng Xuefeng, the legal adviser of Ningbo Bohui Chemical Technology Co., Ltd. and a lawyer at Beijing Dacheng Law Firm, also emphasized to reporters: "If consumption tax is to be levied on Heavy Aromatic Hydrocarbon Derivatives, the key point should be whether the essential attributes of Heavy Aromatic Hydrocarbon Derivatives meet the annotation on the scope of consumption tax levied on finished oil products set by the national tax policy, and it should not be judged whether the product belongs to taxable consumer goods solely based on the product name. On the contrary, taxpayers should strictly abide by tax laws and regulations and cannot evade tax supervision by changing product names. China's tax policy has always encouraged taxpayers to innovate and develop, but the behavior of taxpayers infringing on the interests of national tax revenue through "name changing sales" is also a focus of national tax policy and regulatory authorities to crack down on."

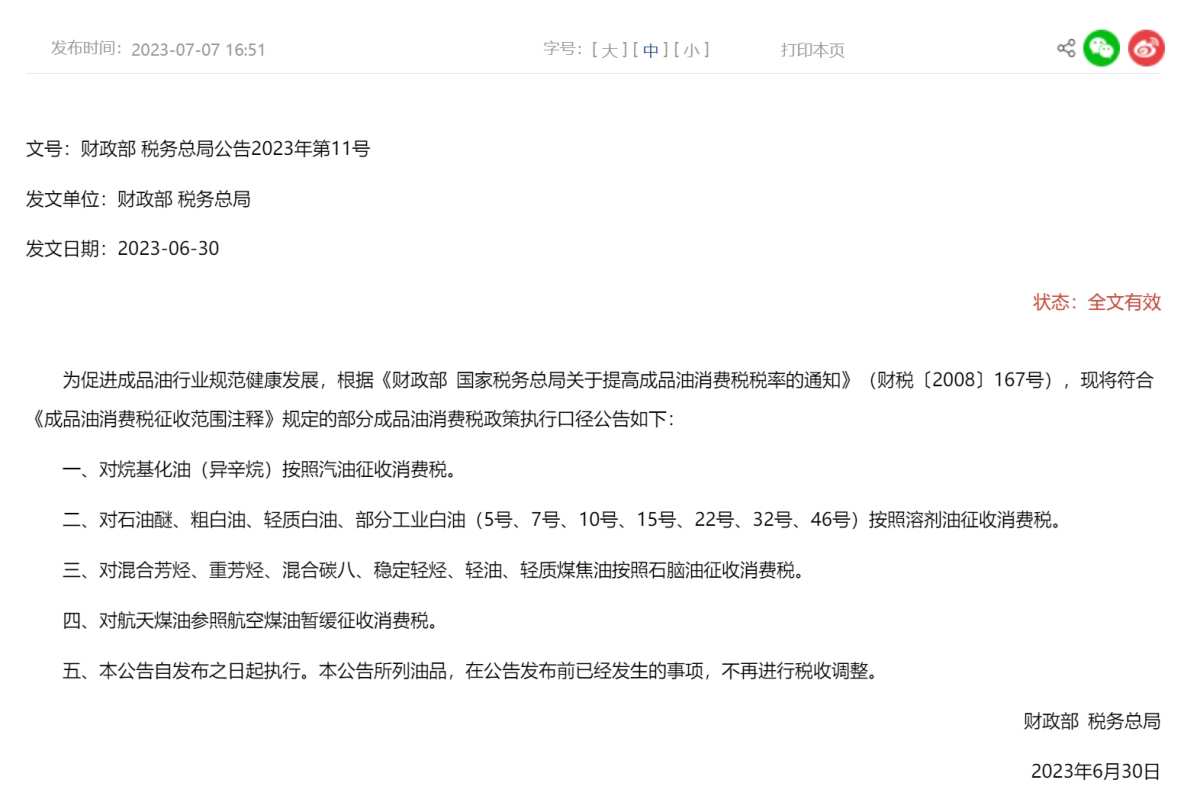

As mentioned earlier, the "Tax and Finance Notice No. 11" refers to the "Announcement of the Ministry of Finance and the State Administration of Taxation on Implementing Certain Policies on Consumption Tax on Partial Refined Oil Products" (Ministry of Finance and the State Administration of Taxation Notice No. 11 of 2023), which has been in effect since June 30th of last year. Article 3 stipulates that consumption tax shall be levied on mixed aromatic hydrocarbons, heavy aromatic hydrocarbons, mixed carbon eight, stable light hydrocarbons, light oil, and light coal tar according to the same criteria as naphtha.

In order to clarify the similarities and differences in specific components between Heavy Aromatic Hydrocarbon Derivatives and Heavy Aromatic Hydrocarbons, the competent tax authorities have conducted multiple tests on the products of Ningbo Bohui Chemical Technology Co., Ltd. According to the company's announcement in April this year, on November 14th last year, the staff of the competent tax authority went to the production site of Ningbo Bohui Chemical Technology Co., Ltd. to sample Heavy Aromatic Hydrocarbon Derivatives products, which were sealed and sent to a third-party for testing.

According to the aforementioned person in charge of Ningbo Bohui Chemical Technology Co., Ltd., the competent tax authorities have conducted at least two more tests afterwards: on April 14th of this year, at the coordination of the local department, Ningbo Customs Technology Center, a third-party, conducted the testing on the Heavy Aromatic Hydrocarbon Derivatives products of the company, and the relevant appraisal report was submitted to the competent tax authorities on April 24th. The latest test was conducted on June 14th after the company announced the shutdown of the equipment, by the competent tax authorities.

In its public statement, Ningbo Bohui Chemical Technology Co., Ltd. firmly stated that the two are not the same substance. For example, at an investor briefing in early April this year, Ningbo Bohui Chemical Technology Co., Ltd. said: there are differences between the two in terms of chemical and physical properties. In addition, the regulations of the tax authorities do not mention that the Heavy Aromatic Hydrocarbon Derivatives belong to the Heavy Aromatic Hydrocarbon category. According to tax and finance regulations, benzene, Heavy Aromatic Hydrocarbons, mixed aromatic hydrocarbons, and their derivatives are regarded as different products and are listed separately.

Regarding the claim of Ningbo Bohui Chemical Technology Co., Ltd. that the two have differences in terms of chemical and physical properties, several industry insiders interviewed recently by Caixin reporters expressed their support.

Regarding the form of Heavy Aromatic Hydrocarbons and Heavy Aromatic Hydrocarbon Derivatives, according to the recent announcements by Ningbo Bohui Chemical Technology Co., Ltd., its two types of products are both solids at normal temperature and pressure. The former contains more than 50% of aromatics, while the sum of aromatics and resins in the latter is between 60% and 90%.

According to the prospectus disclosed by Ningbo Bohui Chemical Technology in 2020, the company's main product heavy aromatics is solid at room temperature and mainly used as an additive. The liquid form is more plastic and easier for customers to use and transport, causing less loss. Therefore, the pipelines in the tanks and production equipment need to be continuously steam heated to keep the heavy aromatics in liquid form.

Reporters learned from industry insiders that heavy aromatics are a class of large molecular weight aromatic hydrocarbons mainly derived from petroleum refining processes, such as reforming heavy aromatics, cracking gasoline heavy aromatics, and coal tar, usually with C9 hydrocarbons as the main component, but may also contain heavier C10 and above aromatic hydrocarbons. In addition, heavy aromatics have a higher overlap with gasoline and diesel components, which means they are similar to these fuels in some properties.

Heavy aromatics derivatives are products that are further extracted or modified from heavy aromatics through chemical reactions or physical processing. The physical and chemical properties and uses of these derivatives are often completely different from the original heavy aromatics, and can be specific chemicals, resins, plasticizers, solvents, etc., with more specialized application areas. Due to additional processing steps, the purity of heavy aromatics derivatives is higher and the function is more specific, so their market value is usually higher than that of unprocessed heavy aromatics as raw materials.

Tax Refund? Tax Avoidance? Or Tax Payment? The "Tax Puzzle" of Ningbo Bohui Chemical Technology

One of the main points of controversy in this "tax refund" event is that the equipment of Ningbo Bohui Chemical Technology was originally used to produce heavy aromatics, and its upgrade to heavy aromatics derivatives production capacity was carried out after the technology optimization of the equipment last July, at the time of the implementation of Document Caishui 11 [2016], which has led to speculations of tax avoidance. At an investor communication meeting in April this year, a shareholder directly asked if (the company's) technological upgrading in July last year to produce heavy aromatics derivatives was to evade the consumption tax on heavy aromatics.

Ningbo Bohui Chemical Technology also disclosed in its April 15 reply announcement to the Shenzhen Stock Exchange inquiry letter that its main product from January to June last year was heavy aromatics, and its product was upgraded to heavy aromatics derivatives through equipment optimization from July.

One detail here is that the decision and implementation of the upgrade of the 400,000 tons/year heavy aromatics unit to heavy aromatics derivatives production through technical optimization was not formally disclosed by Ningbo Bohui Chemical Technology at that time. The explanation given by the relevant person in charge of Ningbo Bohui Chemical Technology is that because investment in the transformation did not fall within the approved authority of the board of directors, it fell within the company chairman's scope of authority and was therefore not a significant event.

Regarding the communication process with the competent tax authorities, according to Ningbo Bohui Chemical Technology's response announcement: the company officially submitted written documents such as heavy aromatics derivatives product analysis report and product appraisal report to the competent tax authorities in September last year, while filing the company's official sales invoices.

Subsequently, the competent tax authorities held multiple communications with the company on the process and classification of its products. On November 2nd last year, the company received a risk warning from the competent tax authorities, indicating that the company had issued heavy aromatics derivatives invoices and that heavy aromatics needed to be taxed as required, and that the company had risks of not paying the full amount of consumption tax. After the company responded with feedback, the competent tax authorities conducted sample testing of the company's heavy aromatics derivatives in the same month (as mentioned above).

On March 27th this year, the company received a "Notice of Taxation Matters" from the Shangpu Taxation Office of Zhenshan Taxation Bureau of the State Administration of Taxation, requiring the company to pay consumption tax on "heavy aromatics derivatives" as "heavy aromatics".

Regarding the testing of Ningbo Bohui Chemical Technology's heavy aromatics derivatives and the determination of taxation on heavy aromatics, after the announcement of the suspension of production by Ningbo Bohui Chemical Technology on the evening of the 13th, the Caixin reporter called the Zhenshan Taxation Bureau for an interview on the following day, and the operator responded: "We are not explaining anything to the public now."

On the same night, the WeChat public account of the Shangpu Taxation Office of Ningbo City Taxation Bureau published a "Situation Notice" from Zhenshan District Taxation Bureau, which stated: "If the enterprise does not actively cooperate to eliminate tax risks, according to relevant policies and regulations, we issued a "Notice of Taxation Matters" to it on March 27, 2024, requiring the enterprise to lawfully pay taxes on the relevant taxable products. So far, the company has not paid in full. In the next step, we will further strengthen communication with the enterprise, continue to strive for cooperation, and carry out policy guidance and compliance management in accordance with the law."

Regarding the specific supporting points of the competent tax authorities' "lawful compliance", a senior finance and accounting expert analyzed to reporters that according to the Provisional Regulations on Consumption Tax, self-produced taxable consumer goods also fall within the scope of consumption tax.

According to Article 4 of the Provisional Regulations on Consumption Tax, taxable consumer goods produced and used by taxpayers continuously to produce taxable consumer goods are not subject to tax; when used for other purposes, they are subject to tax when they are transferred for use.

In contrast, if Ningbo Bohui Chemical Technology's "heavy aromatics derivatives" are transformed from its upstream "heavy aromatics" products in the production process, then because "heavy aromatics" has already been included in the consumption tax payment range, its "heavy aromatics derivatives" are products continuously produced by taxable consumer goods and should therefore also be subject to consumption tax.

For the specific production process of Ningbo Bohui Chemical Technology's "heavy aryl derivatives," whether it is derived from "heavy aryl" products, Caixin journalist contacted the company secretary You Danhong for confirmation, but no response has been received as of press time.

A senior financial expert pointed out that if Bohui Chemical Technology's case involves taxable consumer products for self-use, the company should not evade and avoid discussing it, and the approach of stopping production to cope with it is also unacceptable.

On the other hand, lawyer Wu Sihua from Zhejiang Junan Century Law Firm and independent director of Zhejiang Jinsheng New Materials (300849.SZ) analyzed to Caixin journalists: If the competent tax authority determines that Bohui Chemical Technology's heavy aryl derivative products also need to pay consumption tax, the company may also involve late payment penalties. "According to relevant laws and regulations, if a taxpayer fails to pay taxes within the prescribed time limit or the withholding obligor fails to remit the taxes within the prescribed time limit, the tax authority shall, in addition to ordering the payment within a time limit, collect a late payment penalty at a rate of 0.05% per day from the date of the delay in payment."

One aspect of the Bohui Chemical Technology's tax supplement event that cannot be ignored is that the company had previously enjoyed tax refund preferential treatment for a long time. According to the financial report since its listing, from 2020 to 2023, the top five other receivables with debtors' balance at the end of each period collected by the company were all from the Taxation Bureau of Zhenhai District of Ningbo City of the State Administration of Taxation, with the consumption tax refund amounts of about 231 million yuan, 255 million yuan, 222 million yuan, and 126 million yuan, totaling 834 million yuan in four years.

In the 2023 annual report, Bohui Chemical Technology admitted, "The company is an enterprise that uses purchased taxed fuel oil for the production of aryl chemical products. According to the state's consumption tax revenue policy, the company can calculate the refund of the included consumption tax based on the actual consumption of fuel oil. If the state no longer extends the above refund policy in the future, or adjusts the refund standards and conditions, the impact on product prices will be passed on to downstream enterprises, which will have the same impact on companies producing aryl and heavy aryl as the company, but will still have a negative impact on the company's production, operation and performance."

Will there be losses if the production is not stopped? How much is the cost of stopping and starting the 400,000-ton unit?

The "tax supplement" event has been widely discussed by investors due to Bohui Chemical Technology's production suspension announcement on the evening of June 13. The company said that due to financial difficulties, it suspended the 400,000-ton/year aryl extraction unit, the 400,000-ton/year environmentally friendly aryl oil production unit and related supporting units from June 12. And to control operating costs, the company will adopt various measures to save money, including but not limited to arranging employees to take vacations gradually, reduce salaries, layoffs and other methods.

"The company originally planned to stop production from late May, but why was the announcement not issued until June 13? The 'game' in this process was very big." The person in charge of Bohui Chemical Technology revealed to Caixin journalists, "Before May 20 (this year), the company's plants were basically running at full capacity. From the 'Notice on Tax Matters' issued by the supervisory tax authority in March, the company has been actively communicating with relevant departments, but no substantive progress has been made in the past few months, and the company decided to stop production afterwards."

How is the prosperity of the aryl industry this year? Will the shutting down of Bohui Chemical Technology's production have a significant impact on the market supply and demand? A relevant person in charge of a subsidiary of a major petrochemical company in the southeast region told Caixin journalists that since the beginning of this year, prices of aryl-related products have been high, and companies along the industrial chain have performed well. The person also believes that Bohui Chemical Technology's 400,000-ton production capacity is not large in the industry, and its suspension is not expected to have a significant impact on the industry.

However, for Bohui Chemical Technology, the size of the tax supplement amount disclosed in the announcement did bring considerable pressure. According to the "Reply Announcement" on April 15, the company needs to declare a payable consumption tax amount of 296 million yuan and 187 million yuan during the tax period of 2023 and the first quarter of 2024, respectively. Its estimate is based on the consumption tax unit tax amount of RMB 2,105.20/ton.

The announcement also revealed that Bohui Chemical Technology's sales volume of "heavy aryl derivatives" in 2023 and the first quarter of 2024 were 140,000 tons and 88,800 tons, respectively (including internal sales), corresponding to revenue of about 631 million yuan and 420 million yuan, and a rough estimate of unit prices of about 4,500 yuan/ton and 4,700 yuan/ton, which does reflect the trend of price increases.

In terms of performance, Bohui Chemical Technology achieved revenue of 793 million yuan in the first quarter of this year, a year-on-year increase of 90.69%; the net loss attributable to its parent company was 99.43 million yuan, a year-on-year loss, and the net profit attributable to its parent company in the same period last year was 53.87 million yuan.

The aforementioned person in charge of Bohui Chemical Technology said, "The main reason for the company's loss in the first quarter is that it handled relevant accounting according to the 'Notice on Tax Matters,' excluding this part of the impact, the company actually made a profit of several million yuan. If we don't stop production, comply with the tax department's request to pay taxes, and continue production for the whole year, we are expected to lose about 800 million yuan."

Compared with this, the cost of stopping and starting the unit in the short term may not be much. A chemical industry insider estimated to Caixin journalists: If the 400,000-ton/year aryl extraction unit stops working without returning materials (raw oil), and then starts working directly (equipment is not overhauled, no need to load materials, and the pipeline process does not need to be pressure tested), there are only labor, fuel consumption, raw material consumption, equipment operation and maintenance, etc. The estimated cost is around 600,000 yuan.

(Caixin journalist Zhang Chenjing also contributed to this article.)