Response of Tier 1, 2, and 3 Energy Storage Vendors

The fierce competition for lithium batteries has spread further into the energy storage industry. In order to ensure stable market share and cash flow, many energy storage battery companies have begun to drastically reduce prices and only seek to win bids for energy storage projects.

As the maximum price of energy storage batteries and system prices in June are close to the cost price, how will Tier 1, 2, and 3 energy storage battery manufacturers respond?

1. The scale of energy storage is rapidly expanding, but the price has repeatedly reached new lows

In June of this year, the maximum prices and quotations for energy storage cells and energy storage systems of CNPC Jichai Power Company and China Huadian Group Co., Ltd. fell to 0.33 yuan/Wh and 0.495/Wh, respectively, all of which are record lows.

As more large enterprises enter the energy storage industry, the internal volume of energy storage batteries continues to increase.

In 2023, many energy central state-owned enterprises, such as the National Energy Group, CNNC, China Energy Construction and China Power Investment Corporation, began to successfully enter the energy storage circuit and became the main force in the energy storage bidding market.

In 2023, the scale of domestic energy storage projects won the bid reached 99.78 GWh, with a year-on-year growth rate of nearly 300%. Among them, energy storage projects of energy central state-owned enterprises account for nearly 80% of the capacity.

Corresponding to the rapid expansion of the scale of energy storage projects, the winning bid prices have dropped frequently. In 2023, the minimum price for energy storage systems (4 hours) dropped sharply to 0.65 yuan/Wh year on year, and the lowest price of energy storage cells also dropped to 0.45 yuan/Wh.

In the first half of this year, the energy storage industry was still in a fierce battle for “price rolls”, and the reasons for frequent price cuts for energy storage batteries are as follows:

(1) Overcapacity, fierce competition, some manufacturers are willing to win the bid at reduced prices

Energy storage battery production capacity and production have maintained rapid growth. Under the trend of supply exceeding demand, the operating rate of major energy storage battery companies continues to decline.

At present, the planned production capacity of domestic energy storage batteries and systems has exceeded 1.5 TWh (domestic energy storage battery production capacity will only be around 200 GWh in 2023). In May of this year, China's energy storage cell production reached a record high of 25.56 Gwh, an increase of 13% month-on-month and 56% year-on-year.

However, due to the gradual overcapacity of energy storage batteries, the capacity utilization rate of major energy storage battery manufacturers did not increase but declined. The overall capacity utilization rate dropped from 87% in 2022 to 50% in 2023. Even in the era of leading Ningde, the capacity utilization rate dropped to about 70%.

Overcapacity in energy storage batteries has become the root cause of price cuts and volume grabbing.

(2) The price of raw materials for energy storage batteries has once again returned to a downward range

Battery-grade lithium carbonate, an important raw material for energy storage batteries, has returned to the price reduction cycle, and the cost has passed downstream, bringing the possibility of price reduction.

In March-May of this year, due to the low motivation of some lithium salt manufacturers to start construction after the holiday season, the supply of lithium salt declined in the short term, and battery-grade lithium carbonate ushered in a short-term rebound, returning from less than 100,000 yuan/ton to around 130,000 yuan/ton.

This also led to a rare month-on-month rebound in the bid price for energy storage projects during this period. The average price of the energy storage system surged back above 0.65 yuan/Wh for the first time to reach 0.6516 yuan/Wh, an increase of 4% over the previous month.

However, the rebound in raw material prices did not continue. In mid-June, the prices of battery-grade lithium carbonate and lithium hydroxide once again fell below the 100,000 yuan/ton mark, falling to 98,000 yuan/ton and 95,000 yuan/ton respectively. The price of raw materials fell back to an all-time low, and the winning bid price for the energy storage project naturally fell along with it. [Sishen 3]

2. The profit levels of Tier 1, 2, and 3 tier energy storage battery manufacturers vary greatly

As an important component that accounts for more than 60% of the cost of energy storage systems, there is no doubt about the importance of energy storage batteries, but they are also the most competitive part.

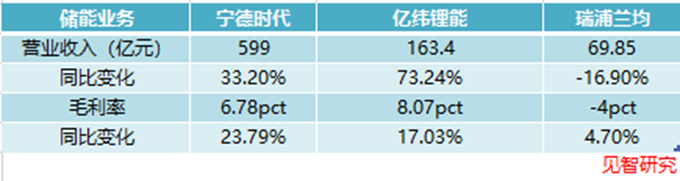

Under the current intense competitive pattern of overcapacity and the continuous decline in bid prices for energy storage projects, the profit levels among energy storage battery manufacturers also vary greatly. With Ningde Era, Everweft Lithium Energy, and Ruipu Lanjun as representatives of first-tier, second-tier, and third-tier manufacturers, the differences between the different manufacturers are obvious.

(1) Ningde era

In the Ningde era, which was the largest producer of energy storage batteries in the world (market share as high as 40%), it still maintained an absolute advantage in the energy storage field even in the context of price wars. Not only did shipments and operating income guarantee high growth, but gross margin did not decline but increased, making it the business with the highest gross margin during the Ningde era.

In 2023, the annual energy storage battery system business of Ningde Times achieved revenue of 59.901 billion yuan, an increase of 33.2% over the previous year; the gross margin level increased 6.78 percentage points year on year to 23.79%.

(2) 100 million weft lithium energy

As a leading second-tier energy storage battery company, Everweft Lithium also achieved significant growth in 2023. Shipments of energy storage batteries reached 26.3 wGH, a year-on-year increase of 121%, ranking third in the world for two consecutive years, and the market share increased by 3 percentage points to 11%.

It is worth noting that Everweft Lithium Energy did not maintain its market share at the cost of drastically sacrificing profits. Instead, it benefited from previous high-priced long orders. Against the backdrop of lower prices for raw materials, gross margin increased.

In 2023, Everweft Lithium Energy's energy storage battery revenue was 16.340 billion yuan, up 73.24% year on year; gross margin level increased 8.07 percentage points year on year to 17.03%.

(3) Ruipu Lanjun

As a third-tier energy storage battery company, Ruipu Lanjun's life wasn't that good. Because such energy storage battery companies rely more on price cuts to seize customers. Naturally, we will have to face the problem of a simultaneous decline in revenue and gross margin.

In 2023, Ruipu Lanjun's energy storage battery revenue was 6.985 billion yuan, down 16.9% year on year; gross margin level decreased by 4 percentage points to 4.7% year on year.

One important reason for this huge difference is the overseas market. The overseas revenue growth rate and gross margin of Ningde Times and Everweft Lithium Energy far surpassed the domestic business. Since they went overseas earlier, the two companies already accounted for 32.7% and 27.3% of overseas revenue, respectively.

Obviously, the future of energy storage batteries will also go overseas.