The new royalty model will bring ARM's overall growth, and these are the points you need to know.

With the launch of Qualcomm's first AI PC, edge AI has once again reached a new high.

Recently, Bank of America released a report stating that$Arm Holdings (ARM.US)$ and $Micron Technology (MU.US)$will be the two biggest beneficiaries of AI PCs and AI smartphones.

Benefits to ARM -

1) The shift from x86 to ARM increases ARM's market share. (This was previously analyzed in the article "ARM once again makes ambitious statements, aiming for 50% of the windows market share")2) ARM architecture upgrades from ARM v8 to ARM v9. This new architecture can obtain a higher royalty rate, from ARM v8's 1-2% to ARM v9's 2-4.5%, and supports overall computing solutions with higher royalty rates CSS (8-10% royalty rate) (details are analyzed in the following text).

Benefits to MU -

1) The increasing need for high-bandwidth memory in AI servers for cloud computing;

2) The annual growth rate of memory needs for AI PCs and AI smartphones will reach 12-15%;

I. ARM

Bank of America believes that ARM will benefit from the AI wave from three perspectives: ARM v9 architecture, overall computing solutions CSS, and increased licensing revenue.

1) ARM v9 architecture.

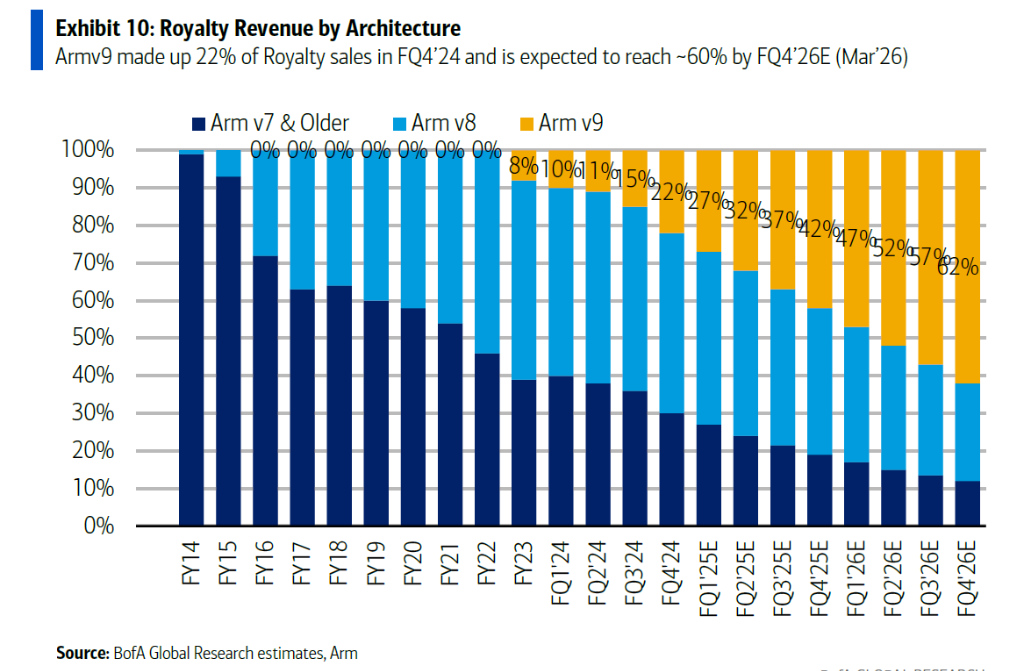

AI is the catalyst for ARM architecture from v8 to v9. Bank of America predicts that in 2026, ARM v9 architecture will contribute to 60%-70% of revenue (currently only 22%). The biggest highlight is that the cost of v9 is higher than v8, from 2% to 4.5%. An increase in the proportion of v9 means an increase in revenue.

Compared to the v8 architecture, ARM v9 architecture improves the overall performance and power efficiency of the chip. In addition, this architecture enhances critical security functions for large models.

In terms of performance, ARM v9 architecture introduces X-level processor cores, which can achieve PC-level performance on smartphones.

Currently, all mainstream high-end Android phones (priced at $600 or above) use processors based on the v9 architecture, such as Qualcomm's Snapdragon 8/7 Gen 3, Mediatek's Tianji and Samsung's Exynos, which have been using ARM v9 architecture for 1-2 years.

As of now, Apple has been the only major company designing its processors based on the older v8 architecture. However, this will change with the launch of Apple Intelligence.

The new M4 processor for iPad and Mac (expected to be released in 2024) will be based on the v9 architecture. Similarly, the A18 Pro processor planned for the iPhone 16 Pro series, which is expected to be launched in 2024, will also use the v9 architecture.

According to the company's financial report, the royalty revenue of ARM v9 architecture in Q1 2024 accounted for about 22% of the total royalty revenue. Bank of America predicts that this number will rise to 60%-70% by Q4 2026.

2) The overall solution of CSS increases the blended royalty rate.

Through ARM's overall solution of CSS, ARM may double its royalty rate on the basis of v9 architecture to reach 8-10%.

CSS is a pre-packaged processor building block component launched by ARM, pre-validated, integrated and tested by ARM. This saves customers, especially chip designers (AP suppliers), a lot of time and resources because they don't have to build everything from scratch.

This is especially useful for AP suppliers who are trying to compete with old manufacturers like Qualcomm, as they can quickly develop competitive chips using CSS.

Currently, chip manufacturer MediaTek has successfully used CSS to grab market share from Qualcomm.

Bank of America said that the royalty rate of CSS is very high, which can reach twice that of the v9 architecture, driving up the overall royalty rate of ARM.

3) ARM -- Increased revenue from licensing.

ARM has a dual model of licensing royalties + device usage royalties, similar to Qualcomm's royalties. This means that as the volume of terminal devices increases, the royalties received based on the number of devices will increase.

In the past 1-2 years, ARM has signed new device quantity royalty agreements with new customers, and existing customers are also undergoing expansion agreements. The licensed royalty has already been reflected in patent licensing revenue, but has not yet been reflected in device usage licensing royalties.

This will be one of the important sources of growth for ARM.

II. Micron (MU) -- AI drives memory demand

Bank of America pointed out that due to the popularity of artificial intelligence, the demand for DRAM in edge AI devices is increasing significantly, and this trend is expected to bring huge profits to memory suppliers in the next few years.

AI PC memory demand: In 2023, the average memory of personal computers is 13.5GB, while the minimum memory requirement for AI PCs is 16GB. It is expected that this number will continue to increase, exceeding 19GB by 2026 (compound annual growth rate of 12%).

AI mobile phone memory demand: In 2023, the average DRAM capacity of AI mobile phones is about 7GB, and it is expected to reach about 11GB by 2026 (compound annual growth rate of 15%).

Specifically, in the iOS ecosystem, Apple's AI function is only available on models with 8GB or more of memory. Currently, only about 61 million iPhones (7.6%) have enough memory to support this feature, and most iPhones (92.4%) are equipped with 2GB-6GB of memory and cannot use Apple Intelligence.

This means that the replacement wave driven by AI will push the average memory of Apple phones to 8GB, twice the current average level.

In the Android ecosystem, Qualcomm's Snapdragon 7/8 Gen 3 processor supports AI functions, requiring at least 8GB of memory. And 12GB is also becoming more and more common, such as the Samsung Galaxy S24+/Ultra.

This trend, coupled with the wider adoption of artificial intelligence processors, is expected to drive the average memory capacity of smart phones to more than 7GB.

Editor/Somer