人们的注意力预计将转向实现预期的种植面积。随着7月和8月的临近,焦点将转移到这些决定产量的关键月份的天气状况上。市场对天气模式及其对农作物产量影响的不确定性可能会维持波动。

人们的注意力预计将转向实现预期的种植面积。随着7月和8月的临近,焦点将转移到这些决定产量的关键月份的天气状况上。市场对天气模式及其对农作物产量影响的不确定性可能会维持波动。Weekly Overview

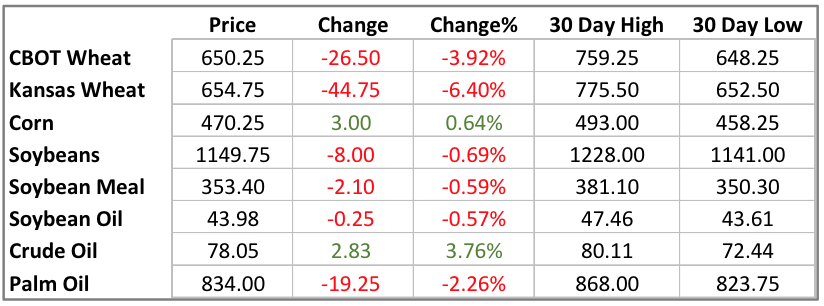

Price Changes This Week

In the past week, CBOT agricultural commodities prices declined. Wheat prices dropped due to improved prospects for HRW crops, while corn and soybean prices remained relatively stable. Looking ahead, price fluctuations are expected mainly due to adverse weather conditions and inaccuracies in the supply and demand balance sheet of each commodity.

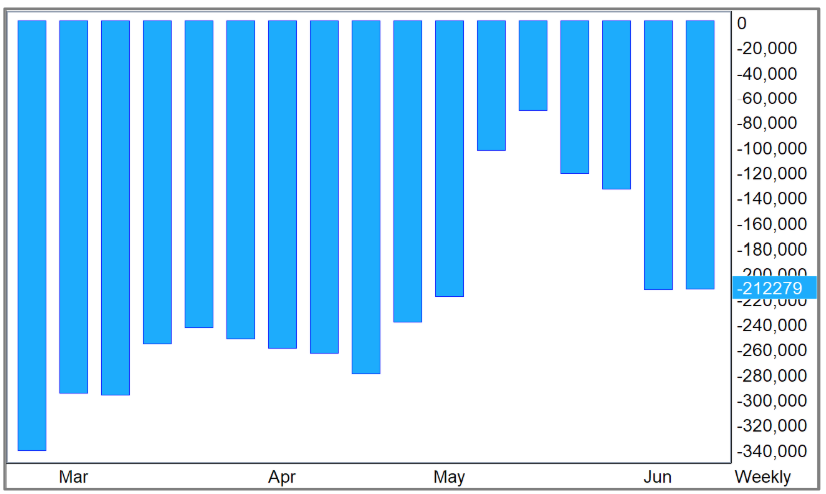

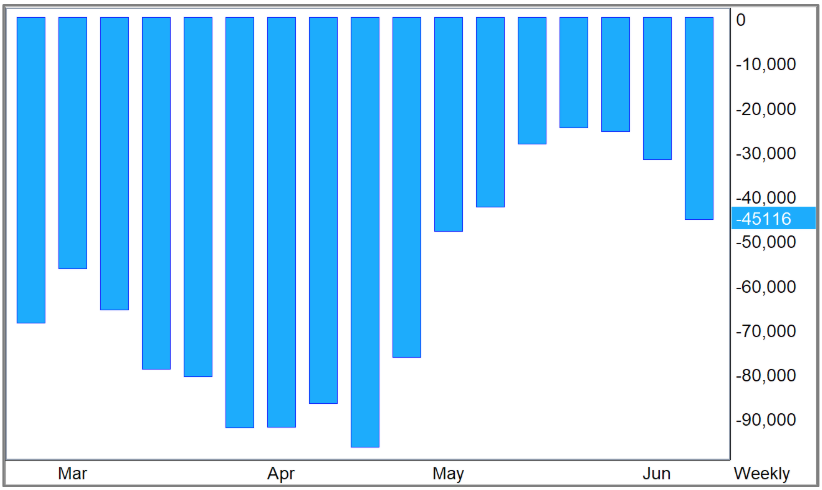

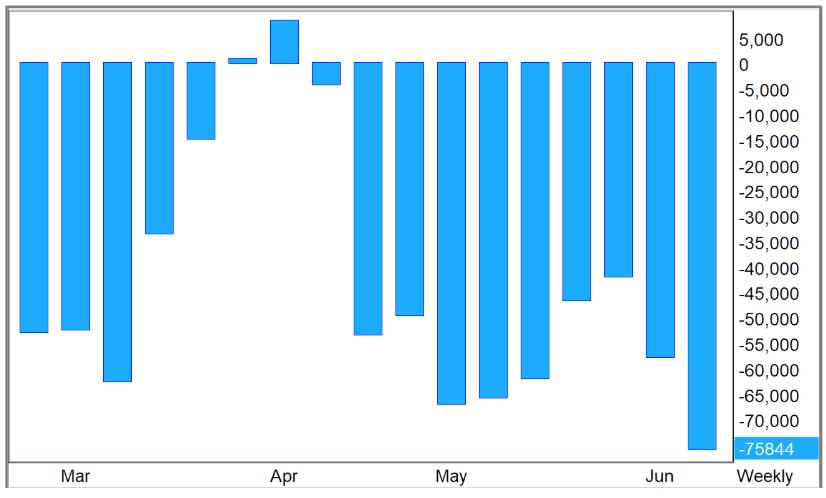

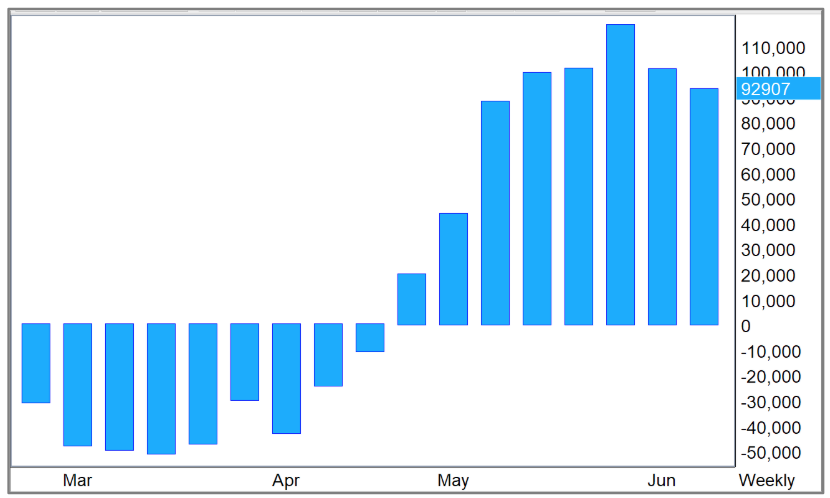

The latest Commitment of Traders (CoT) report showed a bearish stance, with funds increasing their short positions in corn and soybeans. Controlled funds also began liquidating soybean meal long positions contracts, reducing their bullish position to 92,000 contracts. Weather continues to play an important role in price volatility.

Wheat prices are particularly sensitive to weather conditions in the Black Sea region, while the next few months are critical in determining corn and soybean prices.

Net Fund Positions (Contracts) for Soybean

Net Fund Positions (Contracts) for Corn

Attention is expected to turn to achieving expected planting areas. As July and August approach, the focus will shift to weather conditions in these critical months that determine yield. The market's uncertainty about weather patterns and their impact on crop yields may continue to cause volatility.

Attention is expected to turn to achieving expected planting areas. As July and August approach, the focus will shift to weather conditions in these critical months that determine yield. The market's uncertainty about weather patterns and their impact on crop yields may continue to cause volatility.

Grains

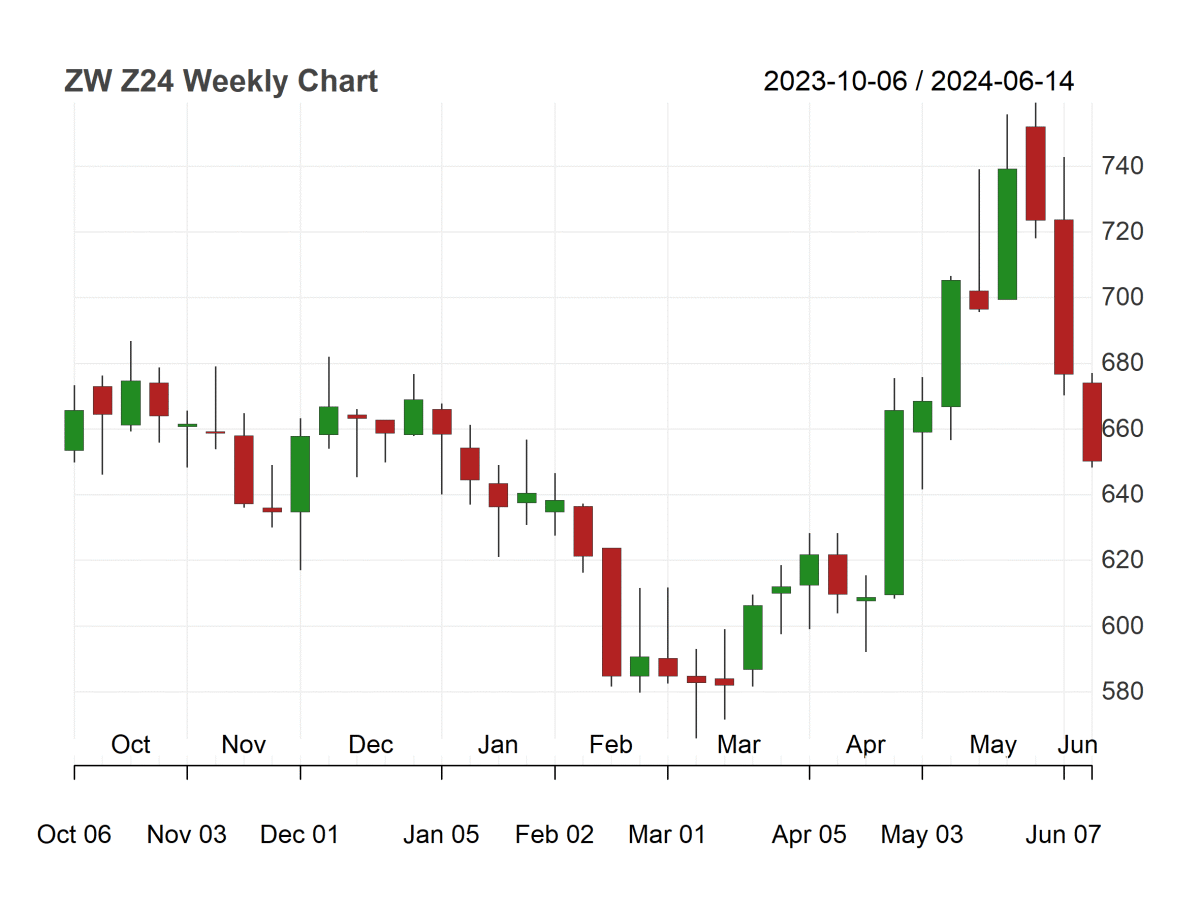

U.S. wheat futures fell for the third consecutive week. Various factors have impacted this trend, including frost and winter weather risks in Russia, as well as improved weather conditions for HRW crops in the United States. As harvest pressure begins to outweigh concerns over weather conditions, prices are expected to continue to fluctuate.

Crop surveys in Kansas suggest that final yields may exceed the estimates in the USDA's May report, although the risk persists if hot and dry conditions impact HRW crops as the growing season nears its end. In Russia, freeze damage seems widespread, while abnormal dryness in the Black Sea region exacerbates market uncertainty about export potential.

Net Fund Positions (Contracts) for CBOT Wheat

Wheat harvesting is expected to be largely completed next month, with similar progress anticipated for Ukraine and Russia. Recent price competitiveness of European wheat has satisfied import demands, and a large amount of old stocks in the EU has had a significant impact on base price.

Demand may shift from Russia and Ukraine to other export countries over time, causing historic tightening in supply and demand balances for the EU, Australia and Canada. Whether wheat prices will rebound after harvest will depend largely on whether global demand shifts from other wheat producing areas to the United States.

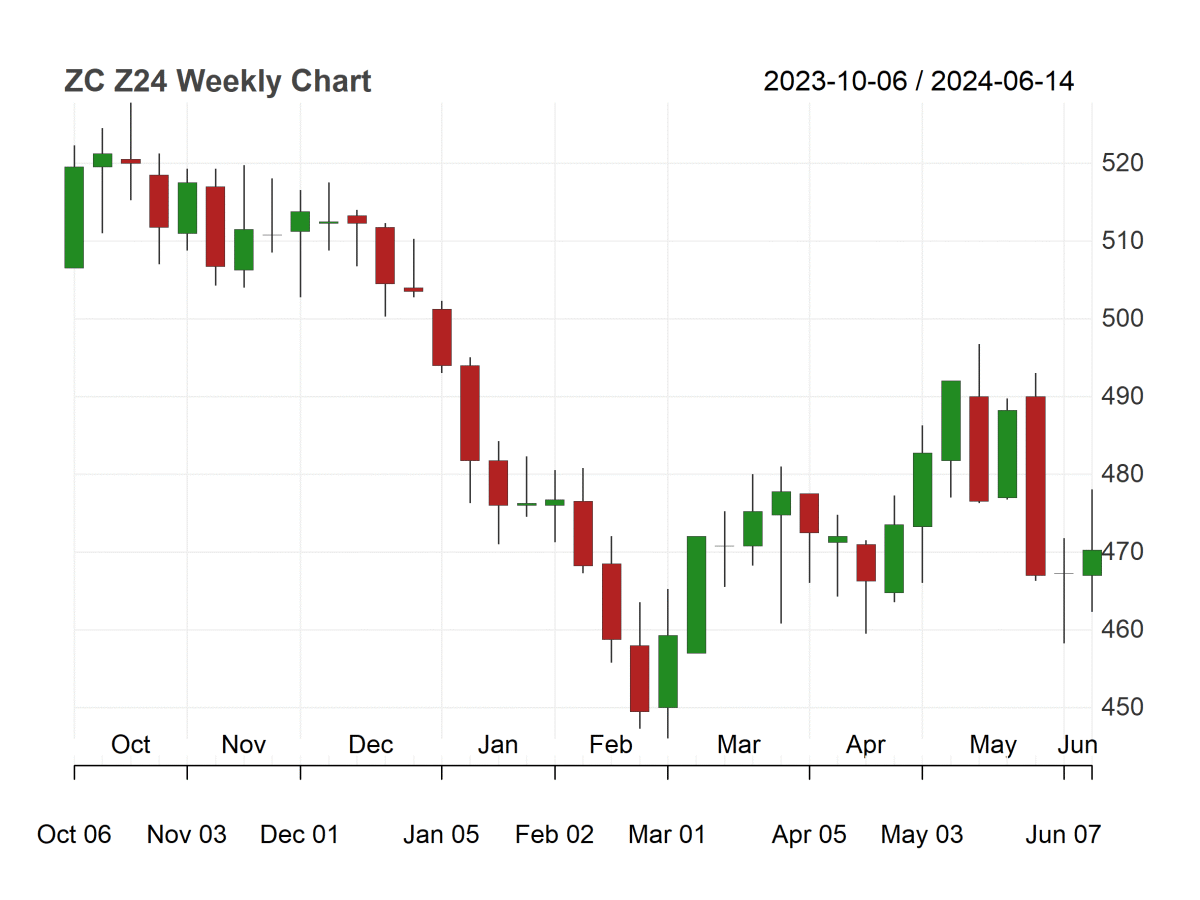

CBOT corn spot prices were supported last week by strong early summer export demand and growing concerns about weather in the Midwest. As corn enters the most sensitive period for yields, traders should prepare for significant volatility in the coming 6-8 weeks, with long-term weather forecasts becoming increasingly concerning.

Concerns about production abound due to the droughts occurring or intensifying in key regions such as Mexico, Ukraine and China. Nonetheless, the coverage of dryness in the U.S. Midwest is the smallest since 2022, with initial crop ratings relatively high compared to the five-year historical range. The long-term outlook for corn is positive, with total output from Argentina, Brazil and Ukraine expected to decrease significantly in 2024.

However, some competition for summer and early fall import demand may emerge in July.

To maintain inventories around 2 billion bushels, the United States needs record-breaking production, with 182 bushels or more per acre, but favorable weather conditions are necessary. Controlled funds increased their net short positions, currently at 212,000 contract positions.

The key will be the duration of high temperatures and dryness throughout July, with the significant likelihood that soil moisture will quickly vanish in the next 10 days as a result of sustained high temperatures. U.S. weather will play a critical role in weekly corn price movements, especially in July, when corn yields are most sensitive to weather fluctuations.

Oilseed Complex

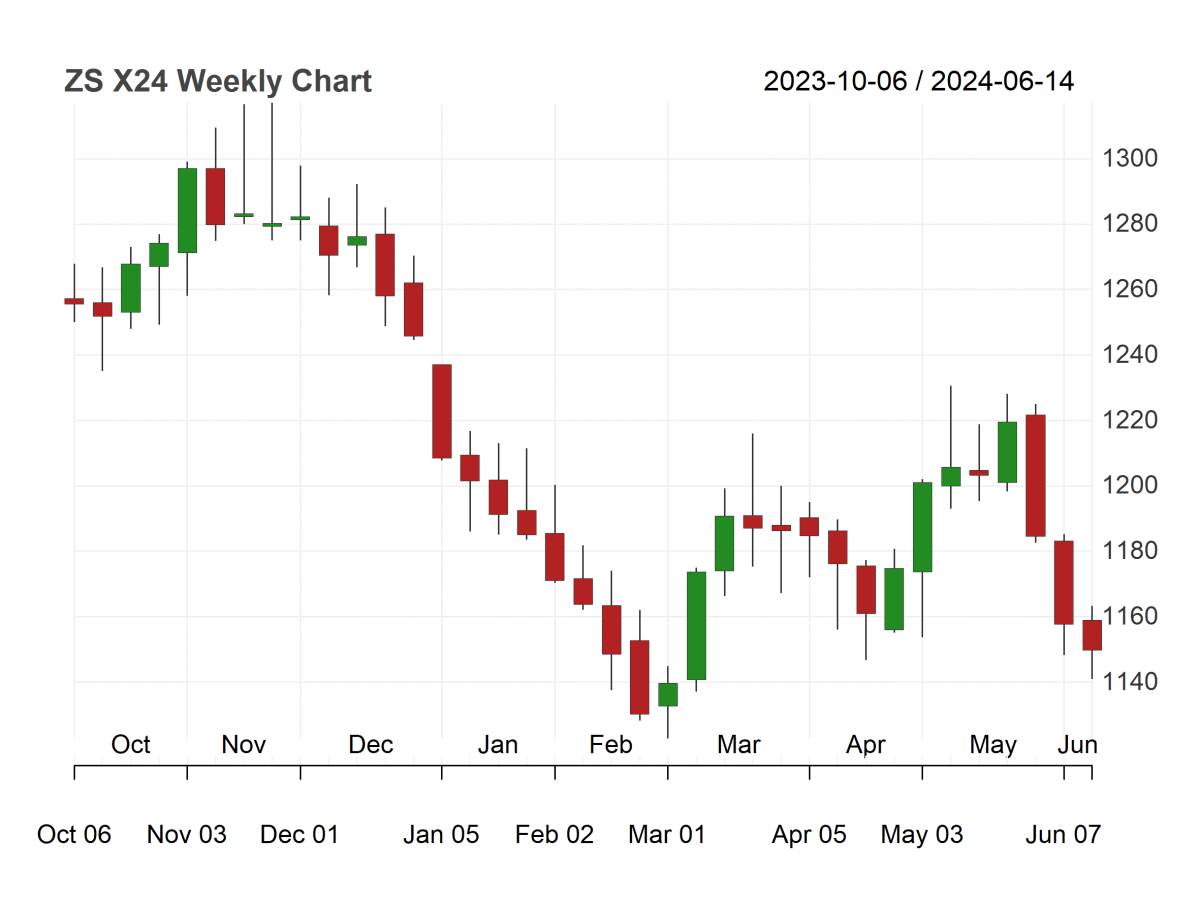

Soybean futures remained stable at the end of the relatively quiet trading week. The market initially rebounded due to warmer and drier weather forecasted in the Midwest, but then fell back after the release of the June WASDE report, which did not bring any major surprises. The U.S. Department of Agriculture slightly lowered its forecast for old crop crush by 10 million bushels and increased stocks by the same amount.

According to reports, the U.S. GD/EX crop rating for soybeans is 72%, reflecting the current state of the crop. Market news is limited, and planting progress remains in line with historical averages. Funds have turned bearish on soybeans, with a current short position of 59,000 contracts. Limited rainfall and rising temperatures in the eastern and southern planting regions are expected to have a negative impact on crop ratings in the next week, while crops in the western and northern regions are expected to receive abundant rainfall.

Net positions (contracts) for soybean oil regulated funds.

Net positions (contracts) for soybean meal regulated funds.

China has not yet obtained any important new crop soybeans from the United States, but summer purchases are expected to increase. This may ultimately lead to downward revisions in new crop export data. The market's main focus remains on planting progress and weather conditions during the growing season.

As we enter the peak planting season, volatility is expected to increase, and weather conditions will play a crucial role in determining market trends.

Disclaimer and Important Disclosures

The information in this report is for reference only and should not be construed as a recommendation to buy, sell, or trade any particular investment. The purpose of this document is only to assist you in discussing PRETB. Please note that there may be multiple authors of this report, and the views reflected in this report may have varied over the past 12 months or even been opposite. A large number of views are being generated and changed immediately. Any valuation or fundamental assumptions are based on the author's market knowledge and experience. In addition, the information in this report has not been prepared in accordance with legal requirements aimed at promoting the independence of investment research. While we believe the information relied upon is reliable, we do not guarantee its accuracy or completeness. PRETB believes that the information in this report has been disclosed to the public on the Internet. This material is not intended to be used as a general guide to investing or as a source of any specific investment advice. Investors should consult their financial and tax advisors concerning the suitability of this brief for their individual circumstances.

This material does not constitute an invitation or solicitation to anyone in any jurisdiction in which such invitation or solicitation is not authorized. Persons in possession of this document must inform themselves of any such restrictions and comply with them.

This document is confidential. It may not be copied, distributed or transmitted by any person without the express written consent of PRETB. All rights reserved.