The operation cash flow remains negative.

It is learned from Gelonghui that the Shanghai Stock Exchange terminated the review of the initial public offering of shares and listing on the main board of Changzhou Baojia Niandai Film Technology Co., Ltd. (hereinafter referred to as "Baojia Niandai") because it withdrew its application for public issuance and listing recently.

Baojia Niandai is a high-tech enterprise specializing in the development, production and sales of functional films. Since its establishment in 2007, the company has been focusing on the functional film industry, and its products are widely used in industries such as photovoltaic components, consumer electronics and home decoration.

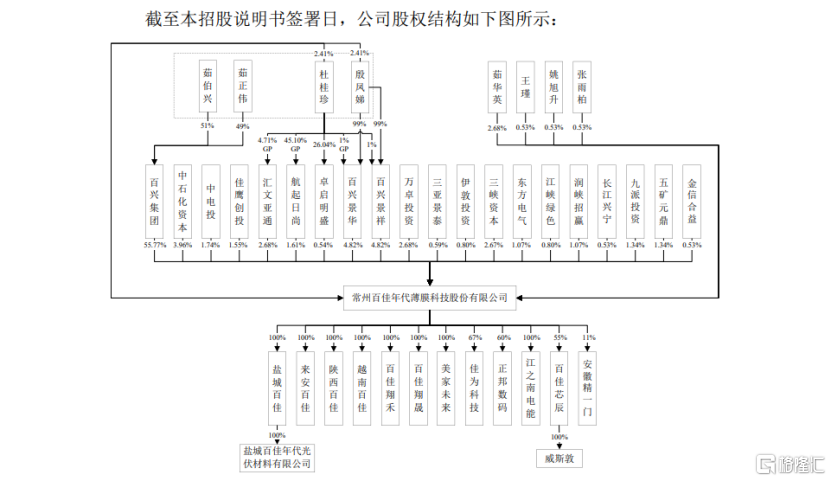

As of the sign date of the prospectus, Ru Boxing, Ru Zhengwei, Yin Fengdi and Du Guizhen together controlled 74.5132% of the issuer's shares and were the joint actual controllers of the issuer. Among them, Ru Boxing and Ru Zhengwei are father and son, Ru Boxing and Yin Fengdi are husband and wife, and Ru Zhengwei and Du Guizhen are husband and wife.

Ru Boxing, born in 1947, has a college degree and is a senior economist; Ru Zhengwei, born in 1975, has a doctorate; Yin Fengdi, born in 1952, has a junior high school education; Du Guizhen, born in 1975, has a master's degree.

According to the prospectus, Baojia Niandai originally planned to raise approximately RMB 1.597 billion for the annual production of 260 million square meters of photovoltaic film projects, the annual production of 88 million square meters of photovoltaic film projects, the renovation of the R&D center project, and the supplementary working capital.

The operating cash flow has been negative.

According to the prospectus, the main business income of Baojia Niandai is mainly composed of photovoltaic film, PVC film, BOPET film, PC film, and adhesives and coating materials.

According to the prospectus, the competition pattern of the photovoltaic film industry is basically stable. As an industry leader, Foster's market share is maintained at around 50%. Baojia Niandai's market share was 4.78%, 6.25%, and 8.89% in 2019, 2020, and 2021, respectively, showing a year-on-year upward trend, forming the second echelon with Swick and Haiyouxin.

In 2019, 2020, 2021, and the first half of 2022, with the rapid development of downstream photovoltaic component industry, the scale and proportion of Baojia Niandai's photovoltaic film business revenue continued to rise, accounting for 38.72%, 54.56%, 71.36%, and 81.49% respectively, and became an important source of the company's revenue.

The composition of the company’s main business income comes from the prospectus.

In terms of performance, Baojia Niandai's operating income in 2019, 2020, 2021, and the first half of 2022 was approximately RMB1.026 billion, RMB1.347 billion, RMB2.542 billion, and RMB1.987 billion, respectively. The corresponding net profit attributable to the parent company was approximately RMB45.7598 million, RMB121 million, RMB127 million, and RMB188 million, respectively.

The company's main financial indicators come from the prospectus.

It is worth noting that although the company's net profit attributable to the parent company has continued to increase, the company's operating cash flow has been negative.

In 2019, 2020, 2021, and the first half of 2022, the net cash flow from operating activities of Baojia Niandai was approximately -RMB46.5484 million, -RMB331 million, -RMB491 million, and -RMB1.056 billion, respectively.

The company stated that due to the downstream customers of the company's photovoltaic film products mainly being large component manufacturers, the payment cycle is long. The upstream suppliers of the company are mainly large-scale chemical raw material manufacturers and generally require advance payment for goods, which puts pressure on the company's turnover of operating funds.

In the future, with the continued growth of the company's business scale, if the operating cash flow continues to be negative, or there are other significant adverse factors affecting the company's short-term solvency and turnover of operating funds, and the company cannot raise funds through other financing channels in a timely manner, the company may face the risk that the fund size cannot support the rapid expansion of its operating scale.

In the first half of 2019, 2020, 2021, and 2022, the gross profit margins of the company's main business were 18.14%, 22.37%, 14.98%, and 19.84%, respectively. From 2019 to 2021, the gross profit margins of the company's main business were lower than the comparable average of the same industry during the same period, which were 20.96%, 26.30%, and 19.89%, respectively.

Comparison of the company's gross profit margin with comparable companies in the industry come from the prospectus.

Baojia Niandai stated in the prospectus that in the first half of 2019, 2020, 2021, and 2022, the overall gross profit margin of the main business was lower than that of Shanghai Tianyang New Materials, mainly because the proportion of Tianyang New Materials' hot melt powder and granule business is higher, and the corresponding business gross profit margin is higher; the overall gross profit margin of the company's main business is lower than that of Foster, mainly because Foster is the industry leader in the photovoltaic film industry, and its high gross profit margin matches its market position.

In terms of R&D expenses, BJND's R&D expenses were CNY 33,438,500, CNY 46,074,400, CNY 79,158,900, and CNY 47,447,000 in 2019, 2020, 2021, and the first half of 2022, respectively, with R&D expense ratios of 3.26%, 3.42%, 3.11%, and 2.39%, respectively. The company's R&D expense ratio was the same as the industry average in 2019; and it was slightly lower than the industry average in 2020, 2021, and the first half of 2022.

Comparable to the industry, the R&D expense ratio of the company's comparable companies comes from the prospectus.

Accounts receivable continue to increase.

Along with the recent development of the company, the company's accounts receivable continues to increase.

In 2019, 2020, 2021, and the first half of 2022, the book value of the company's accounts receivable was approximately CNY 241 million, CNY 355 million, CNY 634 million, and CNY 1.017 billion, respectively. The book value of bills receivable was approximately CNY 253 million, CNY 395 million, CNY 458 million, and CNY 636 million, respectively, accounting for 50.74%, 43.65%, 44.00%, and 40.27% of the total assets in each period-end consolidated financial statement.

BJND stated that with the rapid development of the company's business, the amount of accounts receivable and notes receivable may further increase. If the client credit management system fails to be effectively implemented, or downstream clients encounter difficulties in their operations due to macroeconomic, market demand, or poor product quality factors, there will be risks of accounts receivable and notes receivable becoming unrecoverable or unacceptably, which will have adverse effects on the company's revenue quality and cash flow.

In addition, the company's inventory has also been gradually increasing.

In 2019, 2020, 2021, and the first half of 2022, BJND's inventory accounted for 9.28%, 10.88%, 16.48%, and 21.00% of the total assets, respectively, with a year-by-year increase.

The company stated that it has made provision for inventory impairment losses in accordance with accounting standards and combined with the actual situation of inventory. The inventory impairment loss amounts for each reporting period are CNY 3,536,500, CNY 4,241,400, CNY 7,683,700, and CNY 7,944,800, respectively. At the end of 2022, affected by the sharp drop in the price of EVA resin, the company expects to make provision for inventory impairment losses of over CNY 90 million for EVA raw materials and related photovoltaic film products.

In the future, if the market environment changes, or there are other unforeseeable reasons, causing the inventory to be unable to be sold smoothly, or the inventory price to drop significantly, there may be a risk of further expanding the inventory impairment loss that the company faces.

Epilogue

BJND recently withdrew its IPO application, which has attracted market attention. In recent years, the company's revenue and net income attributable to its parent have grown significantly, but the company has also experienced a sustained negative operating cash flow, continuous increase in accounts receivable and inventory. The company needs to strengthen its financial management, optimize its cash flow, to ensure stable operation and sustainable development.