Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that J.B. Hunt Transport Services, Inc. (NASDAQ:JBHT) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

What Is J.B. Hunt Transport Services's Debt?

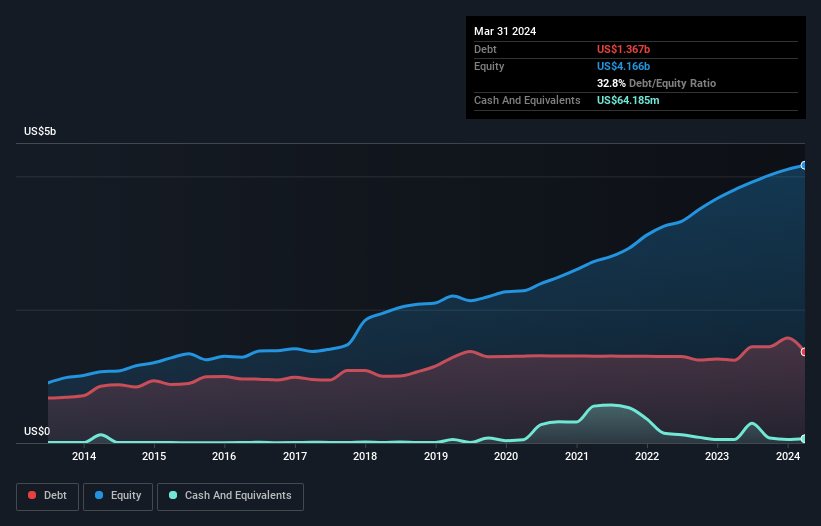

The image below, which you can click on for greater detail, shows that at March 2024 J.B. Hunt Transport Services had debt of US$1.37b, up from US$1.24b in one year. However, because it has a cash reserve of US$64.2m, its net debt is less, at about US$1.30b.

How Strong Is J.B. Hunt Transport Services' Balance Sheet?

The latest balance sheet data shows that J.B. Hunt Transport Services had liabilities of US$1.54b due within a year, and liabilities of US$2.72b falling due after that. Offsetting this, it had US$64.2m in cash and US$1.27b in receivables that were due within 12 months. So its liabilities total US$2.93b more than the combination of its cash and short-term receivables.

Of course, J.B. Hunt Transport Services has a titanic market capitalization of US$16.2b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

J.B. Hunt Transport Services has a low net debt to EBITDA ratio of only 0.79. And its EBIT covers its interest expense a whopping 15.4 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. In fact J.B. Hunt Transport Services's saving grace is its low debt levels, because its EBIT has tanked 29% in the last twelve months. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if J.B. Hunt Transport Services can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, J.B. Hunt Transport Services created free cash flow amounting to 12% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Neither J.B. Hunt Transport Services's ability to grow its EBIT nor its conversion of EBIT to free cash flow gave us confidence in its ability to take on more debt. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. We think that J.B. Hunt Transport Services's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Given our hesitation about the stock, it would be good to know if J.B. Hunt Transport Services insiders have sold any shares recently. You click here to find out if insiders have sold recently.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com