Key Insights

- DoorDash's Annual General Meeting to take place on 20th of June

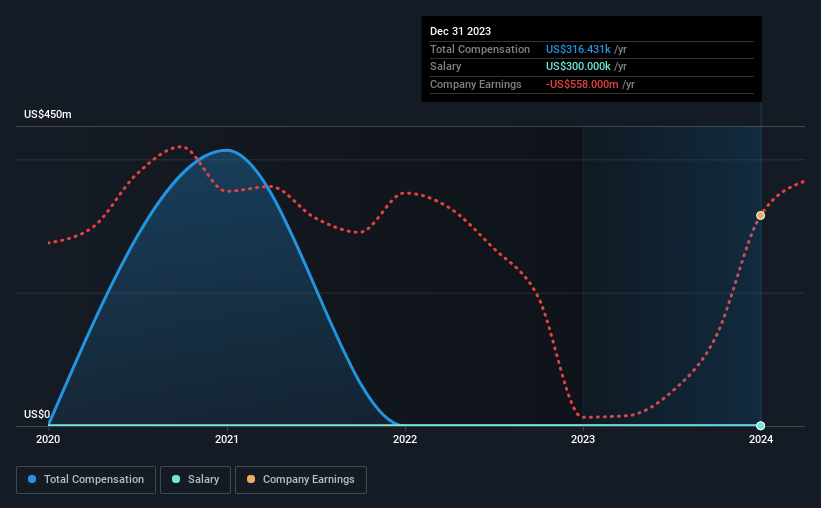

- CEO Tony Xu's total compensation includes salary of US$300.0k

- Total compensation is 98% below industry average

- Over the past three years, DoorDash's EPS grew by 6.4% and over the past three years, the total loss to shareholders 33%

Shareholders may be wondering what CEO Tony Xu plans to do to improve the less than great performance at DoorDash, Inc. (NASDAQ:DASH) recently. At the next AGM coming up on 20th of June, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We think CEO compensation looks appropriate given the data we have put together.

Comparing DoorDash, Inc.'s CEO Compensation With The Industry

According to our data, DoorDash, Inc. has a market capitalization of US$47b, and paid its CEO total annual compensation worth US$316k over the year to December 2023. That's just a smallish increase of 5.4% on last year. Notably, the salary which is US$300.0k, represents most of the total compensation being paid.

For comparison, other companies in the American Hospitality industry with market capitalizations above US$8.0b, reported a median total CEO compensation of US$17m. That is to say, Tony Xu is paid under the industry median. Moreover, Tony Xu also holds US$1.1b worth of DoorDash stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$300k | US$300k | 95% |

| Other | US$16k | US$221 | 5% |

| Total Compensation | US$316k | US$300k | 100% |

On an industry level, roughly 18% of total compensation represents salary and 82% is other remuneration. According to our research, DoorDash has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at DoorDash, Inc.'s Growth Numbers

Over the past three years, DoorDash, Inc. has seen its earnings per share (EPS) grow by 6.4% per year. In the last year, its revenue is up 27%.

We like the look of the strong year-on-year improvement in revenue. Combined with modest EPS growth, we get a good impression of the company. So while we'd stop short of saying growth is absolutely outstanding, there are definitely some clear positives! Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has DoorDash, Inc. Been A Good Investment?

Few DoorDash, Inc. shareholders would feel satisfied with the return of -33% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

The loss to shareholders over the past three years is certainly concerning. The lacklustre earnings growth perhaps may have something to do with the downward trend in the share price. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board's judgement and decision-making is aligned with their expectations.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 2 warning signs for DoorDash that investors should think about before committing capital to this stock.

Important note: DoorDash is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com