Source: Wall Street See

Author: Du Yu, Fang Jiayao

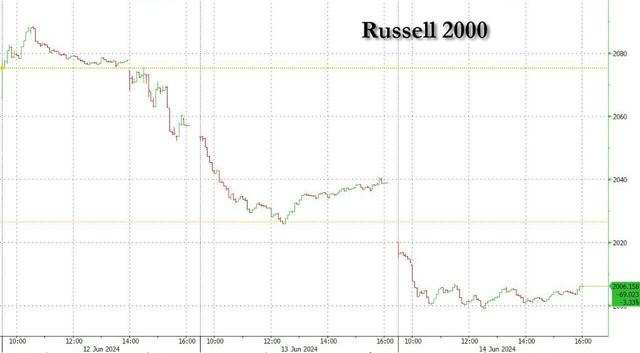

US consumer confidence unexpectedly fell to a seven-month low, inflation expectations rebounded, S&P 500 fell from its historical high, Dow Jones fell for four consecutive days, Russell 2000 small cap stocks fell to a six-week low, and some analysts believe that concerns about the economy have emerged. Throughout the week, S&P and Nasdaq rose 1.6% and 3.2% respectively, both of which rose in the seventh week within eight weeks, and Dow Jones fell 0.5% and small cap stocks fell 1%.

Apple is no longer at a new high and its market cap once again loses to Microsoft, while Microsoft, Nvidia, and Broadcom are at new highs. Adobe rose 14.5%, and Broadcom increased 23% in a single week, the largest increase in history. The Chinese concept index hit a new low of nearly eight weeks, falling 2.7% throughout the week. New energy vehicles fell across the line on Friday, and Li Auto Inc. fell more than 3%.

European stocks fell more than 2% throughout the week, the worst in eight months. French stocks fell more than 6% throughout the week, the largest decline in more than two years, with French stocks falling 3% at one point on Friday. Expectations of a rate cut in the autumn reignited as the 10-year US Treasury yield fell more than 21 basis points throughout the week. Political risk aversion led to the largest increase in the yield spread between French and German government bonds in a single week in history.

Oil futures have stopped rising for four consecutive days but have remained at a two-week high. US oil saw its first weekly gain in four weeks.

The Bank of Japan's dovish decision caused the yen to fall below 158 on Friday to a more than one-month low. After hawkish remarks from the governor, the yen briefly rebounded. The US dollar index rose to a six-week high and rose 0.6% throughout the week, while the euro fell nearly 1% throughout the week, its deepest decline in two months.

Gold has seen its first weekly gain in four weeks, rising more than $30 or 1.4% on Friday. London aluminum, lead, and nickel fell more than 2% throughout the week.

US import and export prices fell together in May. Import prices fell unexpectedly for the first time in five months, providing more evidence of cooling inflation. Futures traders still believe there is a 70% chance that the Fed will cut interest rates in September and that it will cut interest rates twice this year, which is more accommodative than the central bank's outlook.

However, the preliminary value of the University of Michigan consumer confidence index for June unexpectedly fell to 65.6, a seven-month low, far below the expected increase to 72, mainly because the one- and five-year inflation expectations rose to 3.3% and 3.1%, respectively, the highest since November last year.

As for the Federal Reserve, two officials made dovish remarks. Fed voter Bullard stated that if the May inflation scenario continues for several months, the Fed may consider cutting interest rates. If inflation performs as it did in the first quarter of this year, the Fed will find it difficult to cut interest rates. Outgoing Fed voter Mester said that it is important not to wait too long to cut interest rates. This week's inflation data is good news. Before cutting interest rates, she hopes to see several months of good inflation data.

The Bank of Japan kept interest rates unchanged as expected, and the governor said that interest rates may be raised in July and the magnitude of bond purchases will be significantly reduced, but the reduction in bond purchases will be postponed until the July meeting to give details, which is interpreted by the market as a cautious dovish move. The yen fell to a one-month low at one point, but the governor's hawkish remarks still pushed the yen slightly higher at one point.

Worries about political turmoil in France have intensified, with European stocks falling across the board, French stocks and bonds falling, and bank stocks plunging. The yield spread between French and German 10-year government bonds increased the most in a single week in history. French Finance Minister warns that if the far-right party wins in parliamentary elections, the EU's second-largest economy will face the risk of an economic crisis and may withdraw from the EU.

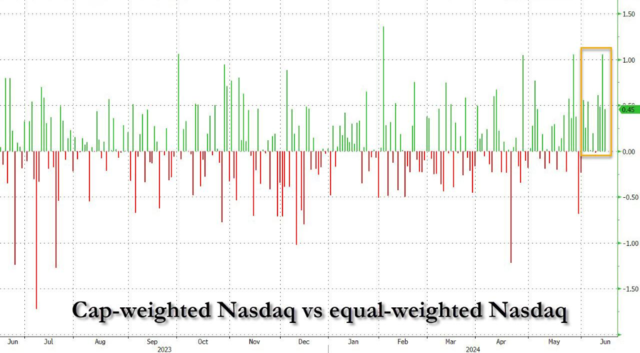

Nasdaq has set a new high for five consecutive days, while Dow Jones and S&P both fell. Most chip stocks, Chinese concept stocks, and retail investors' favorite stocks fell.

On Friday, June 14, the overall trend of US stocks was weak, with the three major indexes opening lower. In early trading, Dow Jones and the S&P 500 failed to turn higher, with Dow Jones falling nearly 341 points or nearly 0.9%, and the S&P 500 falling nearly 30 points or 0.55%. The Nasdaq fell the most by 74 points or 0.42% and turned higher several times in the short term, and the Nasdaq rose at the end of the day, refreshing its daily high and up 0.15%.

As of the close, the performance of Nasdaq has set a new high again. The tech-focused Nasdaq rose slightly by 0.12%, and the blue-chip Dow Jones and the S&P 500 were almost flat, falling by 0.15% and 0.04% respectively. The Russell 2000, consisting of small cap stocks, continued to fall on Friday, falling another 1.6%. Nasdaq 100 hit a historical high, NDXTMC, which measures the performance of Nasdaq's 100 technology components, rose about 0.76% to a new high. "Panic Index" VIX rose 6.03% and rose above $12.

Due to the continued cooling of US inflation data, the expectation of a rate cut by the Federal Reserve in the autumn has been boosted. S&P 500 index and Nasdaq rose by 1.6% and 3.2% respectively throughout the week, both up in the seventh week in eight weeks. However, Dow Jones fell 0.5% throughout the week, and Russell small cap stocks fell 1%.

In terms of sectors, only the technology and communication sectors were relatively stable on Friday. The technology sector rose 0.4% and rose about 6.3% this week. The industrial sector fell by more than 1.1% due to the pessimistic profit warning issued by the MSC industrial direct sales company and the impact of Boeing's delay in 737 production plan. The financial and energy sectors have fallen by at least 2% this week.

Some analysis pointed out that although major central banks in Europe and the United States are easing monetary policy, this process is not enough to offset the pressure on corporate profits brought by the slowdown in economic growth. Concerns about the escalation of economic recession risks are rising, such as the week-long decline of blue-chip stocks and the frequent lead of the Russell small-cap index on major stock indexes. Industrial, banking, and airlines sectors in the S&P market center fell on Friday, and perhaps the market has expected to cut interest rates by the Fed more times this year, betting on the possibility of an economic recession in the second half of the year.

The growth tech stocks were mixed. Tesla performed the worst and fell 2.44%, rising only 0.30% this week. Apple fell 0.82%, with a market value of US$3.26 trillion at the close, and rose 7.92% this week. Amazon fell 0.09% and fell 0.35% this week. Meta rose 0.11% and rose 2.38% this week, while Google A rose 0.93% and rose 1.45% this week. Microsoft rose 0.22%, with a market value of US$3.29 trillion at the close, and rose 4.42% this week. The market value of Apple, Microsoft, and Nvidia exceeded US$3.2 trillion.

Most chip stocks fell. Nvidia rose 1.75%, with a market value of US$3.24 trillion at the close, and rose 9.11% this week. In addition, Taiwan Semiconductor fell 0.23% and rose 5.27% this week, while AMD fell 0.17%. Broadcom rose 3.3% and rose 23% this week, making it the largest single-week increase in history.

Nvidia and Broadcom hit new highs again, although the Philadelphia semiconductor index was close to wiping out the 0.9% decline but it is off its new high. The index hit a new high for four consecutive days and rose 5.9% this week, while the industry ETF SOXX fell 0.4% off its record high. Nvidia rose 1.8% and hit a new high for three consecutive days, with a market value of US$3.24 trillion ranking third. The long ETF for Nvidia rose more than 1% to a new high, while Broadcom rose more than 3% to set another new high, rose 23% this week, setting a new record for the largest single-week increase in history; AMD fell 0.2%, and US stocks of Taiwan Semiconductor, Qualcomm, and Micron Technology have released historical highs. Intel is close to wiping out the drop of 0.8%, and Arm rose 6% before turning down 0.1%.

AI concept stocks narrowed their declines at the end of the day. CrowdStrike rose 0.7%, close to the high, while Oracle fell more than 1%, SoundHound.ai fell more than 4%, BigBear.ai fell 1.5%, C3.ai fell nearly 5%, Snowflake turned into a rise of 1% off a 17-month low, Palantir rose more than 1%, Dell rose 0.5%, Super Micro Computer fell 3%, and Adobe rose sharply by 14.5% to a three-month high.

As requested by the Irish privacy authority, Meta will not be launching Meta AI in Europe for the time being. Tesla shareholders have re-approved Elon Musk's $56 billion sky-high compensation plan, and Tesla's registered location has officially moved from Delaware to Texas. Shanghai Nanhui New City is promoting the landing of Tesla FSD pilot projects. Arm will be included in the Nasdaq 100 Index on June 24th. Software giant Adobe posted record Q2 revenue and updated its full-year guidance, driven by demand for AI and creative software. SPDR Technology Select Sector ETF (XLK) will adjust stock weights based on market capitalization on June 14th, which may bring in a bid demand of over $10 billion for NVIDIA.

Chinese concept stocks fell following the decline of US stock market. KWEB ETF dropped 1.4%, CQQQ ETF dropped 0.5%, NASDAQ Golden Dragon China Index (HXC) fell 1.5%, losing 6100 points to hit the lowest level in nearly eight weeks, down 2.7% for the whole week.

Among popular stocks, JD.com and Baidu both fell more than 2%, while Pinduoduo fell more than 1%. Alibaba fell 3%, Tencent ADR reversed to fall 0.3%, Bilibili fell 5%, new energy vehicles were down across the board, and NIO and Xpeng Autos both fell about 2%, while Li Auto Inc fell more than 3%.

Headed by small retail investors, the stock price of gaming company GameStop has fluctuated greatly over the past week, falling nearly 40% last Friday, dropping another 12% on Monday, rising nearly 23% on Tuesday, falling more than 16% on Wednesday, rising more than 14% on Thursday, opening higher on Friday by more than 5%, and then turning down nearly 6% before finally closing down 1.4% for the whole week, up 1.7% for the whole week.

The 'roaring kitty' with a more than 5 million GameStop shareholding has reportedly built his investment portfolio to a worth of more than $268 million, surpassing the value of $210 million he held in stocks alone as of June 2. It is unclear yet whether he sold or exercised GME call options to acquire more shares.

European stocks continued to fall for two consecutive days, with the pan-European Stoxx 600 index falling about 1% to near six-week lows, led by automotive and industrial shares, down more than 2% for the week, the worst since October 2020. The French stock index fell 3% at the end of Friday, down more than 6% for the week, the largest weekly decline in more than two years, evaporating $210 billion in market value and turning down year-to-date. The largest French banks such as BNP Paribas and Société Générale both fell more than 10% for the week.

The 10-year US Treasury bond yield fell more than 21 basis points for the week, while the spread between French and German bond yields surged to a historical weekly record high.

The unexpected cooling of inflation has sparked expectations of interest rate cuts, pushing down US bond yields for three consecutive days. However, short-term bond yields rebounded at the end of the day, and US bond yields fell by double digits for the entire week. The risk aversion related to the French situation and the US CPI data further boosted US bond prices.

The two-year US Treasury bond yield, which is more sensitive to monetary policy, fell by more than 3 basis points to less than 4.66%, hitting a ten-week low since April 5, and rebounded at the end of the day. The 10-year benchmark bond yield fell the deepest, declining more than 5 basis points to 4.19%, falling below 4.20% at one point, hitting the lowest level in nearly two and a half months since April 1, and falling more than 21 basis points for the week.

The risk aversion in Europe continued to heat up. The yield on the 10-year bund in the Eurozone fell 11 basis points to 2.36% at the end of Friday, with a total cumulative decline of 26 basis points for the week, and the yield on the 2-year bond also fell by about 11 basis points, with a total cumulative decline of 32 basis points for the week. In addition, the 10-year yield on UK bonds fell by about 7 basis points on Friday, falling for four consecutive days and falling more than 26 basis points cumulatively.

After a 7 basis point drop in the 10-year French bond yield, it narrowed slightly, up 3 basis points for the week, and the spread with the German benchmark bond yield reached its highest level since 2017, rising nearly 30 basis points for the week, setting a record high for the highest weekly increase. Some analysts said that potential adverse results from France's parliamentary elections increased people's concerns about the country's debt sustainability.

The oil futures price stopped rising for four consecutive days but hovered at a two-week high. WTI July crude oil futures fell $0.17, or more than 0.21%, to close at $78.45 per barrel on Friday, accumulating more than 3.86% for the whole week, ending a three-week decline. The August Brent futures fell $0.13 on Friday, down 0.16%, to close at $82.62 per barrel, up 2.78% for the whole week.

US oil WTI rose by $0.53 or 0.7% at its highest level during the day, breaking through the $79 per barrel mark, and international Brent rose by $0.64 or 0.8%, breaking through the $83 mark. Oil prices turned down when the US stock market closed.

The 10-year US Treasury bond yield hit a two-month high for the week.

Petroleum analysts generally expect the market to face significant supply shortages in the third quarter of this year, which will boost oil prices in the short term. In addition, the cooling off of inflation supporting the Fed's interest rate cuts this year will also be bullish for oil prices, but the supply will return to excess next year.

The European benchmark TTF Dutch natural gas futures fell 0.8% on Friday, up nearly 7% for the week, while ICE British futures fell more than 1% on Friday and rose more than 6% for the week. The U.S. natural gas July contract fell 3% on Friday, continuing to fall below the $3 mark and wiping out the week's gains, down 1.3% for the week and off its six-month high for three consecutive days, narrowing its cumulative gains this year to 16%.

The dollar rose to a six-week high, up 0.6% for the week, with the euro falling almost 1% for the week, its deepest drop in two months.

The DXY, which measures the dollar against six major currencies, rose 0.7% on Friday to 105.81, its highest level since May 1 and up about 0.6% for the week.

Some analysts believe that the rise of the dollar is mainly due to the expectation that the Fed will only cut interest rates once this year, but the lower-than-expected inflation data has suppressed the dollar's rise. At the same time, the weakness of the euro is the main factor driving the forex market this week.

The euro fell 0.6% against the dollar on Friday and briefly fell below 1.07, its lowest level since May 2, down nearly 1% for the week, its biggest drop in two months. The euro weakened across the board this week, falling to a three-month low against the Swiss franc and its biggest weekly drop against the pound in seven months.

The pound fell more than 100 points or 0.8% against the dollar on Friday, dropping to its lowest level since May 17, as anxiety over the July 4 UK election mounted. The yen fell 0.8% against the dollar, falling below 158 after the Bank of Japan's dovish decision, hitting its lowest level since the end of April and returning to the 157 level with significant losses in the US market. The offshore yuan was slightly weaker against the dollar and remained below 7.27 yuan.

Mainstream cryptocurrencies fell in general for two days. Bitcoin, the largest by market cap, fell another 2% and fell below $66,000, while the second largest Ethereum fell about 2% again and approached the $3,400 integer mark, both hitting four-week lows since mid-May.

Gold rose for the first time in four weeks on a weekly basis, up more than $30 or 1.4% on Friday. London aluminum, lead and nickel fell more than 2% for the week.

Gold rose for the first time in four weeks on a weekly basis. COMEX August gold futures rose 1.3% to $2,348.80 per ounce at the end of the session, while COMEX July silver futures rose 1.6% to $29.52 per ounce.

Spot gold rose more than $30 or 1.4% on Friday, rising back above $2,330 and up about 1.8% for the week. Spot silver rose 1.9% intraday, returning to above $29 and off a one-month low, up about 1% for the week.

The prices of London industrial metals fell for two consecutive days on the strength of the dollar:

The economic barometer 'Doctor Copper' closed down $53 or 0.5% on Friday, holding below $9,800 for seven weeks and down 0.2% for the week. London aluminum fell 1.6% on Friday, approaching a two-month low of $2,500, down 2.3% for the week. London zinc fell 3.2% on Friday, falling below $2,800 for a seven-week low and closing roughly flat for the week. London lead fell 1.2%, down 2.7% for the week. London nickel fell to a 10-week low, down 2.5% for the week. London tin fell 1.5%, but was up 2.8% for the week.

Editor/Jeffy