Source: Wall Street News Author: Du Yu Fang Jia Yao

Before the noon break, US stock indexes collectively fell, while Apple, Microsoft, Nvidia, Taiwan Semiconductor, Qualcomm, Broadcom, Micron Technology, etc. continued to reach new highs, driving the S&P, Nasdaq, and chip stocks to break records again. However, the Dow Jones fell for three consecutive days and fell 300 points at the beginning of the day. CrowdStrike and Oracle dropped out of the highs. Tesla rose 7.8% and closed up 2.9%. Broadcom rose more than 12% due to the positive earnings report, and Adobe rose about 17% after hours. The China concept index opened more than 1% higher and closed slightly higher, Bilibili rose more than 13% and closed up 7.7%, NIO opened 3.6% higher and turned lower. Expectations of a rate cut pushed US bond yields to a ten-week low, and safe-haven demand widened the yield spread between French and German government bonds to a seven-year high. Crude oil futures rose for four consecutive days before accelerating downward after the close, still up this week and hovering near a two-week high. After the PPI, the US dollar fell for a while and then rose to nearly a four-week high of 105. The euro was trading at a six-week low before the central bank decision, and the yen turned lower and lingered around 157. After the PPI, spot gold rose for a while and then fell 1% again, dropping below $2300 once again. LME nickel fell more than 2% to a ten-week low, and copper, zinc, and tin all fell by at least 1.1%.

The US May PPI data released before the US stock market opened was lower than Wall Street's expectations, adding to the bullish sentiment for interest rate cuts. US May PPI month-on-month was -0.2%, the largest drop in seven months, and the report also showed that May core PPI was lower than the expected growth of 0.3%, proving the easing of inflation pressure. In addition, first-time jobless claims rose to the highest level in nine months, further cooling the labor market and adding to signs of slow US economic growth.

Commentators have said that this month's data has strengthened confidence in interest rate cuts, but they still need to wait for some of the more sticky components to loosen before they can start cutting rates. UBS economists' expectation for the first interest rate cut by the Fed has been pushed back from September to December. While inflation cools, the Fed maintains a hawkish stance and continues to perform its duty of "stabilizing market volatility," possibly because of the November US election. After PPI data was released, the currency market now expects two 25 basis point rate cuts by the end of the year, up from the pre-release expectation of 44 basis points. The CME Federal Reserve observation tool shows that the probability of a 25 basis point rate cut in September is close to 70%.

In terms of the market's reaction, large tech stocks and bonds benefit the most. The S&P 500 and the tech-heavy Nasdaq index set closing records again, and US treasuries quickly gained strength after the data was released, with yields diving and 30-year treasury auctions performing well. The US dollar initially fell but rose again in the latter part of the trading day. The bullish interest rate cut expectation did not support rising precious metal prices, with gold and silver prices falling and basic metals in London falling across the board. Oil prices rose slightly and held steady at the end of the session.

On the Japanese side, the market generally expects that the Bank of Japan will keep its current policy interest rate unchanged and that the short-term interest rate target is expected to continue to be maintained at the level of 0.0% to 0.1% at the end of the two-day monetary policy meeting to be held this coming Friday. The currency market forecasts show that the probability of maintaining the interest rate unchanged is as high as 91%, while the possibility of a 10 basis point increase is only 9%. In addition, market focus will turn to the government's bond buying plan, as media reports indicate that as the Bank of Japan gradually achieves policy normalization, it may assess whether it needs to reduce its monthly purchase of about 6 trillion yen in government bonds.

In addition, French President Macron said that he will continue to serve as President until 2027.

The S&P 500 and Nasdaq set new highs, with Apple's market cap overtaking Microsoft's and Broadcom rising more than 12% leading chip stocks.

On Thursday, June 13th, the unexpected decline in US May PPI supported expectations of interest rate cuts, with the main US stock indexes only falling at the opening of the Dow but then turning briefly positive before falling again in the afternoon; the S&P 500, which opened high, was dominated by large-cap and tech stocks, the Nasdaq rose further, and the Russell small-cap stock index remained in decline all day, dropping more than 1.5%, while the Nasdaq had the relatively largest gain among the major indexes.

As of the close, the S&P, Nasdaq and Nasdaq 100 set new highs, while the Dow fell for the third consecutive day:

The S&P 500 index rose 12.71 points, up 0.23%, to 5,433.74. The Dow Jones Industrial Average fell 65.11 points, or 0.17%, to 38,647.10. The Nasdaq Composite Index rose 59.12 points, or 0.34%, to 17,667.56.

The Nasdaq 100 rose 0.57% to a new high, and the Nasdaq Technology Market Cap Weighted Index, which measures the performance of Nasdaq 100 tech component stocks, rose 1.09% to a new high. The Russell 2000 small-cap stock index fell 0.88%, and the "panic index" VIX fell 0.83%, closing below the 12 level for the first time since May 24th.

Looking at the industry indexes, the Nasdaq technology index rose by about 1.1%. The Nasdaq Biotechnology Index fell 0.15%. The Philadelphia Semiconductor Index rose 1.48%. The benchmark KBW Bank Index on the Philadelphia Stock Exchange fell 0.53%. The Dow Jones Regional Bank Index fell 1.56%.

Growth tech stocks fluctuated, with Apple climbing to the top of global market caps. Apple rose 0.55%, continuing to set a new record high for closing prices, with a market cap of about $3.285 trillion, surpassing Microsoft once again, while Nvidia rose more than 3.5% to catch up with the two. In the past three trading days, Apple has risen by 10.94% in total, its best performance in the same period since 2020. Microsoft rose 0.12% to a market cap of $3.281 trillion at the close, while Tesla rose 2.92%; Meta fell 0.93%, Google fell 1.48%, and Amazon fell 1.64%.

Nvidia led a group of chips to set new highs again. The PHLX Semiconductor Index rose 1.5%, setting a new high for the fourth consecutive day, and the industry ETF SOXX also rose 1% to a new high. Nvidia rose 3.5% to a new high, with a market cap of $3.19 trillion, ranking third in the US stock market. Nvidia's double long ETF rose 6.8% to a new high, AMD fell 1.8%, and then fell 0.2%, hovering at a low for a month; Taiwan Semiconductor's US stocks rose 0.2%, Qualcomm rose more than 1%, Broadcom rose more than 12%, and Micron Technology rose 1.7%, all setting new historical highs. However, Intel fell about 1%, and Applied Materials fell away from its new high.

AI concept stocks were generally down. CrowdStrike fell more than 1%, Oracle fell 0.4%, both fell out of their historical highs, SoundHound.ai fell 0.7%, BigBear.ai fell more than 2%, C3.ai fell more than 3%, Snowflake fell more than 3%, refreshing its lowest level in 17 months, Palantir fell more than 2%, but Dell rose more than 2%, and Super Micro Computer rose more than 12% to its highest level in more than two weeks.

In terms of news, Broadcom rose 16% at midday to its largest increase in four years, with second-quarter performance exceeding expectations and full-year guidance raised, announcing a 1-to-10 split plan. Nvidia's share of the global discrete graphics card market rose to 88% in the first quarter. Musk said Tesla shareholders will approve his $56 billion compensation plan. According to reports, in the past six months, OpenAI's annualized revenue has doubled to $3.4 billion from the end of last year. Microsoft draws a commission from OpenAI's AI model sales, and Apple will pay OpenAI by helping distribute rather than cash payment.

Chinese concept stocks narrowed their gains after midday. KWEB ETF rose 0.7%, CQQQ rose 0.5%, and the Nasdaq Golden Dragon China Index (HXC) opened 1.3% higher before closing up 0.3%, still hovering at a seven-week low, briefly rising above 6,200 points at the opening.

In popular stocks, JD.com fell 0.5%, Baidu rose more than 2% before turning down 0.4%, and Pinduoduo almost wiped out its gains of 1%. Alibaba fell nearly 1%, Tencent ADR rose 1.4%, Bilibili, which tested the game "Three Kingdoms: Determining the World," rose more than 13% before closing up 7.7%, new energy vehicles gapped higher, NIO rose 3.6% before turning down 0.9%, Li Auto rose 4.7% before closing up 2.5%, and Xpeng rose 2% before turning down 1.5%.

Gamestop, the leader of retail investors' stock holdings, has fluctuated significantly in the past week, with a drop of nearly 40% last Friday, a further drop of 12% on Monday, a rise of nearly 23% on Tuesday, a fall of more than 16% on Wednesday, and a rise of more than 14% on Thursday, up slightly this week. On Wednesday, the trading volume of the call options held by "Big Brother Roaring Little Cat" was more than nine times the usual volume, causing the price of these options contracts to fall by 40%, driving down the GME stock price.

In addition, space tourism company Virgin Galactic fell more than 14% to a historic low, down more than 16% at one point during the day, with the stock trading below $1 per share since June and the board approving a 1-to-20 reverse stock split plan.

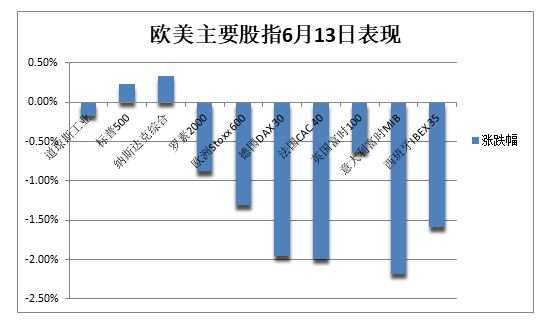

European stocks returned to a downward trend. The pan-European Stoxx 600 index fell 1.31%, hitting a two-week low since May 29, with auto stocks falling more than 2%, leading all sectors and falling to their lowest level in four months. The euro zone's STOXX 50 blue chip index and the national stock indexes of Germany, France, and Italy all fell by about 2%, with the French stock market falling to a four-month low and the German stock market falling below the key technical level of the 50-day moving average.

Expectations of a rate cut have raised the yield on US Treasuries to a ten-week low, with the spread between French and German benchmark bond yields at a seven-year high.

Unexpected cooling of inflation expectations has prompted expectations of a rate cut, causing US Treasury yields to fall for two consecutive days. The bid rate for the 30-year US bond auction was lower than the pre-issuance trading level, stimulating further price increases for US bonds and lower yields.

The two-year US bond yield, which is more sensitive to monetary policy, fell the most by more than 8 basis points to 4.66%, continuing to fall below the key level of 4.70% at the close, hitting a ten-week low since April 5. The 10-year basic bond yield fell the most by 7 basis points to less than 4.22%, refreshing a near two-and-a-half-month low since April 1.

The yield on the 10-year German government bond benchmark in Europe fell 6 basis points to 2.47% at the end of the day, with a cumulative decline of 20 basis points in the past three trading days. The yield on 10-year government bonds in France continued to rise by 2.5 basis points, causing the yield spread between French and German bonds to close at 70 basis points, the widest in seven years since 2017, highlighting panic sentiment. The poor performance of German bond yields is related to MSCIs exclusion of EU bonds from the government bond index.

The US dollar rebounded to approach a four-week high of 105, while the euro traded at a six-week low. Bitcoin fell more than 2% and lost the $67,000 mark.

The US Dollar Index, which measures against six major currencies, fell to a daily low after the PPI data was released. However, regular trading hours of US stocks rebounded, rising by a maximum of 0.6% and approaching the 105 level again, erasing most of the decline from yesterday and reaching a four-week high. The primary reason for the rise of the US dollar is that the Fed is expected to cut interest rates only once this year. However, lower-than-expected US inflation data has restrained the momentum of the US dollar. Yesterday's CPI data caused the US dollar to fall 1%, with a narrow decline at the end of trading, still the largest decline in two weeks.

Analysis shows that the rise of the US dollar is mainly due to the Fed's expectation of cutting interest rates only once this year, but lower-than-expected US inflation data has restrained part of the momentum of the US dollar. Yesterday's CPI data caused the US dollar to fall 1%, with a narrow decline at the end of trading, still the largest decline in two weeks.

The euro fell more than 0.6% against the US dollar and fell below 1.08, trading at a nearly six-week low, having achieved the largest single-day increase this year. The pound fell 0.3% against the US dollar and fell below 1.28, causing part of the tension before the UK general election on July 4th.

The Japanese yen against the US dollar slightly fell and hesitated around the 157 level, trading at a one-week low, with an overnight low against the British pound falling to the lowest level in 16 years. The market is waiting for the Bank of Japan to reduce bond purchases on Friday. Offshore Renminbi against the US dollar hit 7.26 yuan, and then fell slightly during US stock trading, approaching the low of the month again.

Major cryptocurrencies fell across the board. The largest market cap leader Bitcoin fell 2% and lost the $67,000 mark, returning to the lowest level in three weeks. The second largest Ethereum also fell more than 2% and lost the $3,500 mark, touching a three-week low since mid to late May.

US inflation cools down, Russia promises to cut oil production, OPEC comments boost oil demand expectations, and oil prices rise slightly by more than 0.1%

WTI July crude oil futures rose by $0.12 and increased by more than 0.15%, reaching $78.62 per barrel. Brent August crude oil futures rose by $0.15 and increased by 0.18%, reaching $82.75 per barrel.

During the regular US stock trading hours, WTI crude oil rose by a maximum of $0.54 or 0.71%, breaking through the integer level of $79 at one point. International Brent crude oil rose by a maximum of $0.45 or 0.54%, reclaiming the $83 level at one point, but oil prices accelerated their decline after the close.

Analysis shows that the unexpected decline in US PPI further proves that inflationary pressures are easing, paving the way for the Fed to cut interest rates, stimulate the economy, and oil consumption.

Secondly, on Thursday, OPEC Secretary-General refuted the pessimistic monthly report by the International Energy Agency (IEA). The IEA report was bearish on the oil market, believing that global oil demand will reach its peak around 2029. Immediately afterward on Thursday, the OPEC Secretary-General criticized the IEA's views, saying that they would mislead consumers and cause oil market fluctuations to soar. He emphasized that there are still billions of people worldwide who do not have access to energy, and oil demand will continue to increase.

In addition, the Russian Ministry of Energy announced on Thursday that after slightly exceeding its production target under the OPEC+ framework in May, Russia expects to achieve its oil production quota in June. The department pointed out that the issue of excess production in May will be resolved through production adjustments in June to ensure that the established goals are achieved. According to a decree published on the Russian government's legal database, Russian President Putin will not sell crude oil and petroleum products to foreign buyers who comply with international pricing ceilings. This ban has been extended to December 31, 2024.

US July natural gas futures fell more than 2.82%, closing at $2.9590 per million British thermal units. The US Energy Information Administration (EIA) released its weekly report on natural gas inventories, stating that US natural gas inventories increased by 74 billion cubic feet last week, an increase of 2.55% over the week (an increase of 3.51% the week before), reaching 29.7 trillion cubic feet.

Precious metals fell nearly 1.5%, with silver falling more than 4% and falling below $30. London copper fell 1.5%, nickel fell 2.3%, and zinc and tin fell by about 1.1%.

Favorable PPI data did not support the rise of metals. The COMEX August gold futures fell by about 1.49% to $2,319.7 per ounce. The COMEX July silver futures fell 4.04% to $29.045 per ounce, falling below the $30 level.

Spot gold fell nearly $27 or nearly 1.2%, falling below the $2300/oz mark. Spot silver fell more than 3.6% and fell below the $29 integer.

Despite the cooling of inflation in May, gold prices fell on Thursday. Tai Wong, an independent metal trader in New York, said that this week, despite positive data, gold has not been able to maintain its upward momentum, indicating a general situation of profit-taking. China's buying interest may recover at a lower price level, but it is unclear what specific price level they are interested in, as they have not made purchases above $2300.

London industrial metals fell across the board:

The economic bellwether 'Dr. Copper' fell by $150, down nearly 1.51%, to $9794 per ton. LME nickel fell more than 2.30% to $17645 per ton. LME tin fell 1.71% to $32794 per ton. LME zinc fell more than 1.17% to $2860 per ton. LME aluminum fell by $18 to $2557 per ton. LME lead fell by $7 to $2166 per ton.

In addition, during the night session, domestic black futures rose, with asphalt, rbob gasoline, caustic soda, and glass night trading up to 0.61% at most, while coking coal rose 0.68% and coke rose 2.1%. International copper fell 0.86% during the night session, and Shanghai nickel and Shanghai tin both fell 1.40% and 1.62%, respectively.

Editor/Lambor